UK CPI Preview (Jun 17): Inflation Peaking?

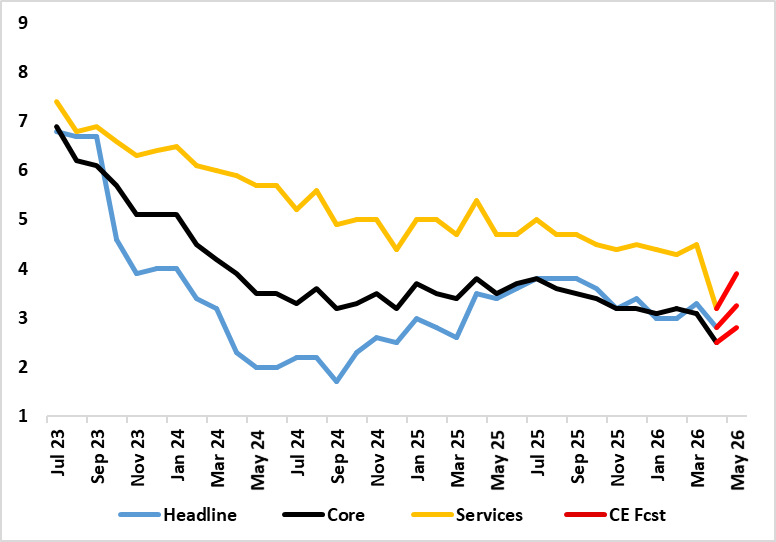

What have been energy induced price rises are now very evident, even more so in some aspects of the latest PPI data. Regardless, actual CPI have offered a more benign picture both in terms fo headline and underlying trends. Indeed, having seen headline CPI jump to 3.3% in March and where services rose to 4.5%, the headline was down to a lower-than-expected 2.8% (BoE saw 3.0%) despite a 15% m/m rise in fuel related energy, this offset by services dropping almost a full ppt, taking the core down to 2.5%, a four-year low. This will not last as even with Government-paid support measures, CPI inflation will rise afresh from this month – we see it back up to 3.2%-3.3% with calendar effects taking services up toward 4% and the core 0.3 ppt higher to 2.8%, all similar to BoE thinking. But the headline may then be at (or near) a peak, especially given the already visible drop in diesel prices.

Figure 1: Headline And Core To Bounce Back?

Source: ONS, Continuum Economics

It is noteworthy that without the rise in fuel prices in the last few months, headline UK inflation would actually be just over 2.1%, ie in line with most projections, (inc the BoE) ahead of the breakout of the Middle East conflict. Even so, the April reality of a headline at 2.8% is below BoE thinking and surely reduces the chance of near-term MPC hikes, not least the lack of second-round effects. As for the policy outlook, the IMF now says in its Concluding Statement of its latest insight into the UK, monetary policy should remain restrictive to ensure that higher energy prices do not spill over to core inflation and wage growth. It says that the rise in energy prices will lift headline inflation this year while also weighing on output, complicating policy calibration. Staff assesses that holding the policy rate unchanged for the remainder of the year would maintain a sufficiently restrictive monetary stance to limit second-round effects and keep long-term inflation expectations anchored. However, given exceptional uncertainty, the BoE should retain the flexibility to adjust the monetary stance in either direction (ie hikes or cuts), but be prepared to respond forcefully if second-round effects prove stronger than anticipated. More recently, the OECD went further, pointing a to renewed rate cuts late this year, noting that ‘further easing in monetary policy is expected, with the Bank of England looking through the energy shock in 2026 and moving to a neutral stance in 2027’

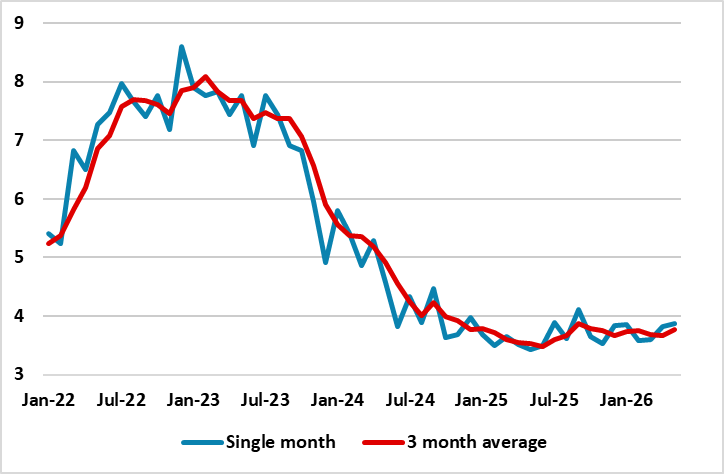

Figure 2: Companies CPI Expectations Stable Still

Source: Mean realised price growth from BoE Decision Makers Survey (May 2026), % chg y/y

Although no longer our central view, a possible very late-year fall back toward 3% may facilitate this OECD projection, all part of what we now see the headline staying around 3.2%-3.3% for the rest of the year and averaging that for 2026 overall, below consensus and BoE thinking and with a temporary dip in June before the OFGEM energy rise takes effect in July.

But the softer than expected April CPI data will not materially change MPC thinking with the data due the day before the next BoE verdict and where more hiking dissents then seem likely. Regardless, it is worth noting that base effects are not the full story as not only are adjusted, smoothed m/m data offering more subdued signs but also are more benign and still stable company expectations (Figure 2) and also actual recent wage pressures.

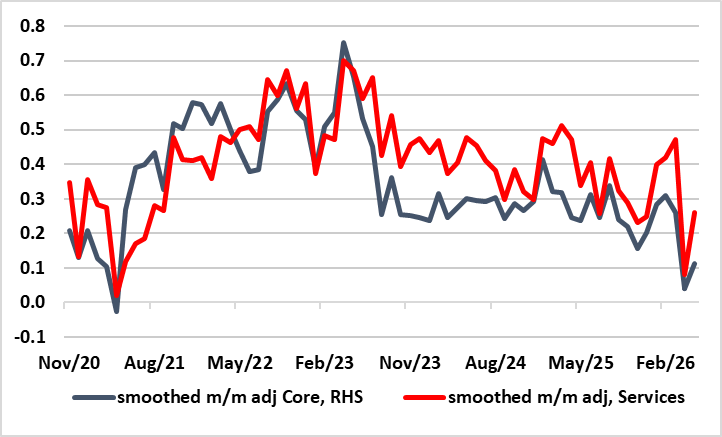

But obviously, the April CPI data showed little, if any’ signs of second-round effects, possibly the opposite especially looking at adjusted m/m numbers (Figure 3).

Figure 3: Clear Adjusted Core Inflation Drop Continues?

Source: ONS, Continuum Economics

This latter view very much reflects a position where we see little second round effects, with even the latest BoE MPR suggesting firms do not have much pricing power especially compared to four years ago with very little expectation of any pick-up in wage growth to come. An unwillingness to raise wages may also reflect company thinking that the medium-term inflation has not changed, this also evident in BoE survey data. Moreover, we would argue that households will not have much wage bargaining power either even if their inflation expectations have risen somewhat. This comes against a backdrop where wage inflation has already slowed continually and clearly.