Canada May Employment - Recent weakness largely erased, wages correct lower

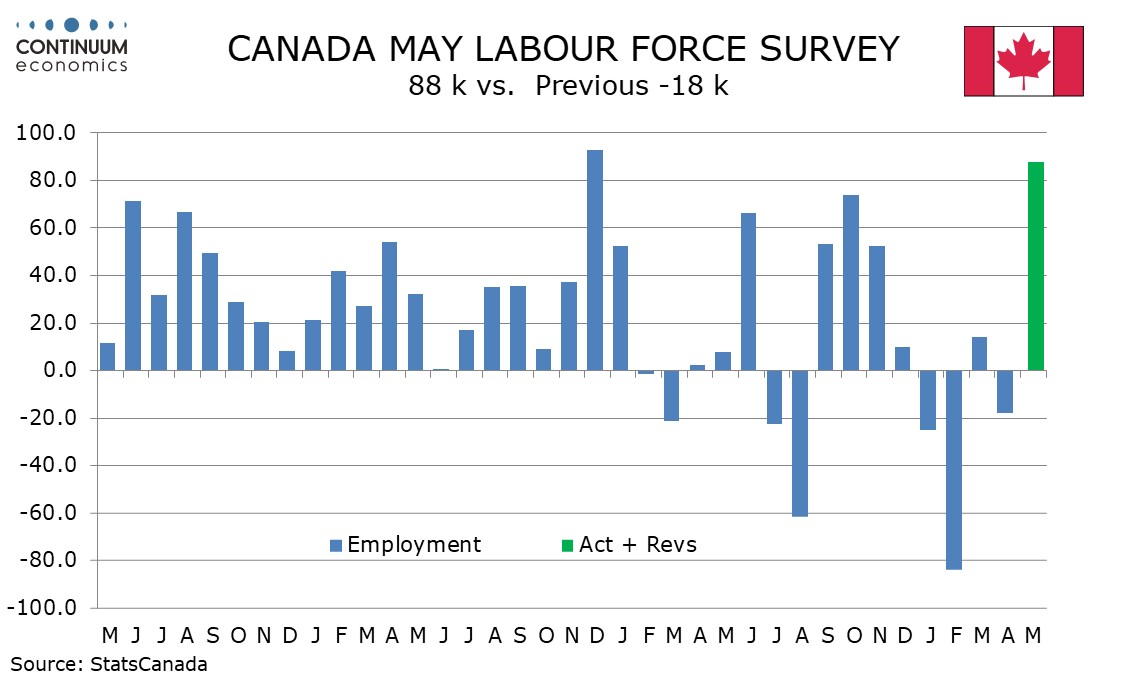

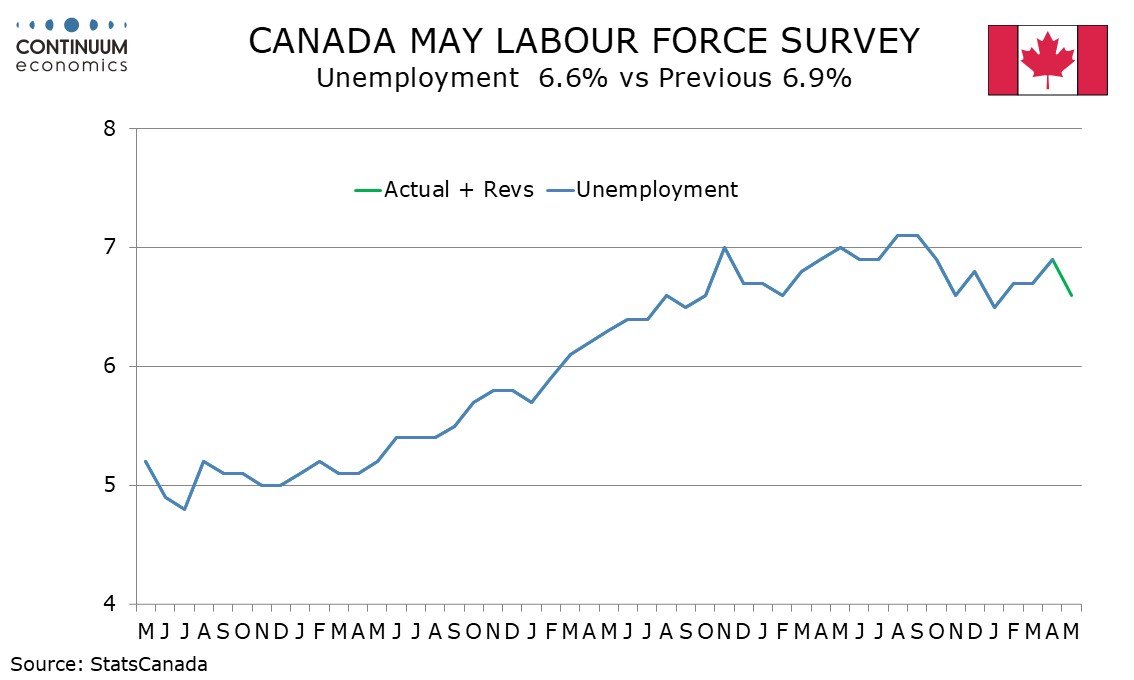

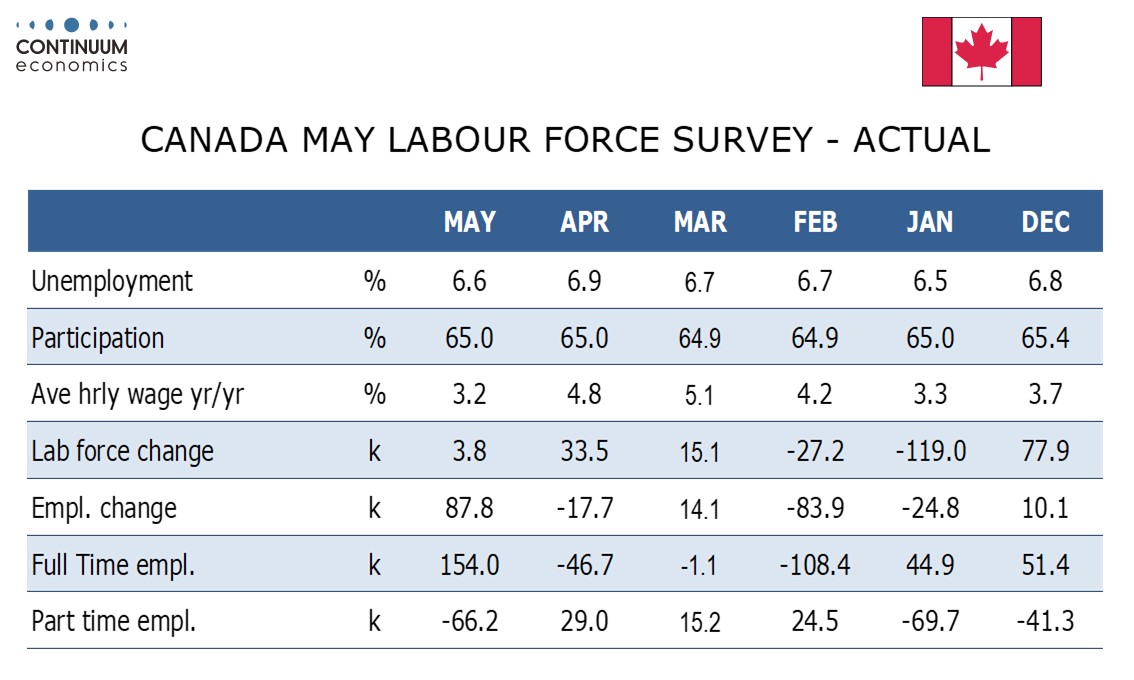

Canada’s May employment report keeps the series volatile, with a strong 87.8k bounce reducing unemployment to a four month low of 6.6%, from April’s 6-month high of 6.9%. This should ease any Bank of Canada worries over the weak Q1 GDP data which saw a second straight, if marginal, decline. The data supports expectations for a return to growth in Q2 as suggested by a positive preliminary estimate for April GDP.

Monthly Canadian employment data is volatile with the data following declines in three of the last four month with employment still below December’s level and almost unchanged from January. The six month average remains marginally negative at -2.4k suggesting trend is fairly close to flat, though over the last twelve months the high of the six month average of 26.9k seen in November is above the low of -8.3k seen in April, suggesting trend is slightly above rather than slightly below neutral.

The labor force significantly underperformed the employment gain, rising by only 3.8k, explaining the decline in unemployment, but the six month average of -2.6k is almost identical to that for employment. Trend in unemployment is fairly flat. Significant labor slack remains.

The details of May’s employment gains are mostly positive, particularly a 154k rise in full time employment after three straight declines totaling 156.2k. Part time employment fell by 66.2k after three straight gains totaling 68.7k. Private sector employment rose by 56.k, the public sector saw a rise of 20.4k while self-employment rose by 11.2k. Goods employment at 38.7k, with construction at 26.8k and manufacturing at 14.7k was more impressive than a 49.1k rise in services, though the latter was firm outside a 35.0k fall in wholesale and retail. Elsewhere gains were broadly based if moderate, with no component of services managing a ruse as high as 20k, but several getting close.

While the data will reduce Bank of Canada fears over downside risk to activity, the approaching review of the USMCA trade agreement, cited by the BoC as a downside risk in April, remains a concern. The BoC will also note that yr/yr hourly wage growth for permanent employees also slowed sharply to 3.2% from 4.8%, seeing a surprising acceleration seen in February and March now fully erased. This and recent core CPI data suggests the BoC’s inflationary worries should not extend much further than energy. The data reduces the risk of the BoC taking a significantly more dovish turn at next week’s meeting, but is not enough to suggest a hawkish turn either.