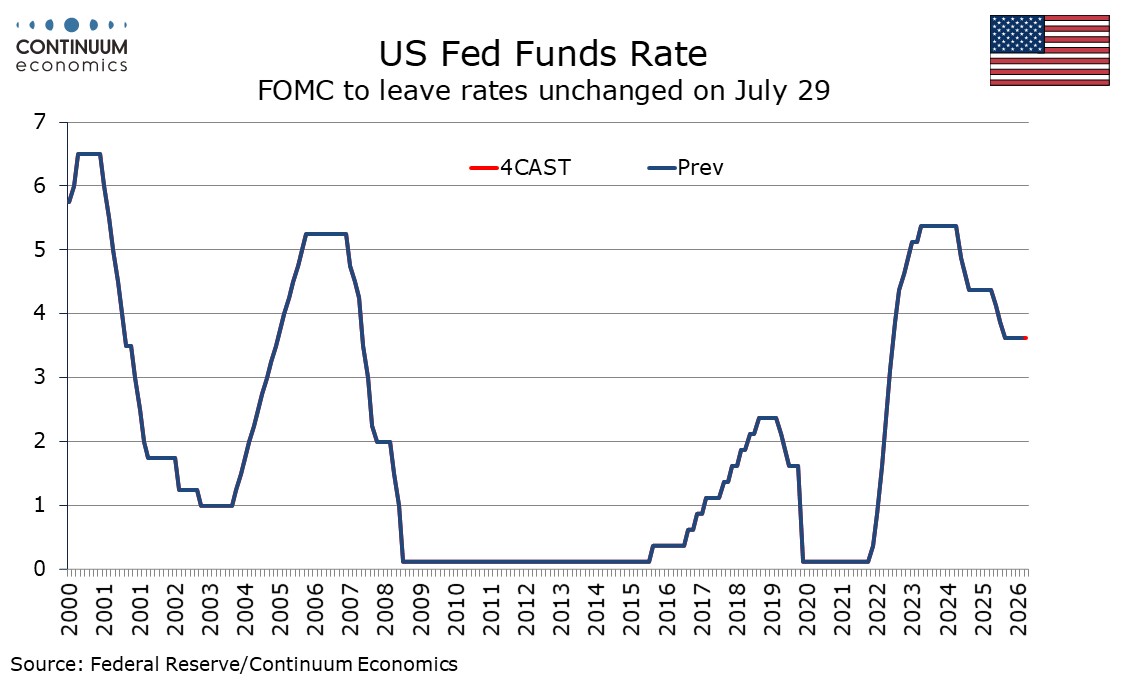

FOMC Preview for July 29: Unchanged policy with an unspoken tightening bias

The FOMC meets on July 29 in a meeting that will see no update to the dots or economic forecasts. With forward guidance now becoming limited all meetings should be seen as live, but after softer than expected June non-farm payroll and more importantly CPI data, a change in policy looks unlikely at this meeting. The case for tightening will be debated, but no more than two hawkish dissents are likely.

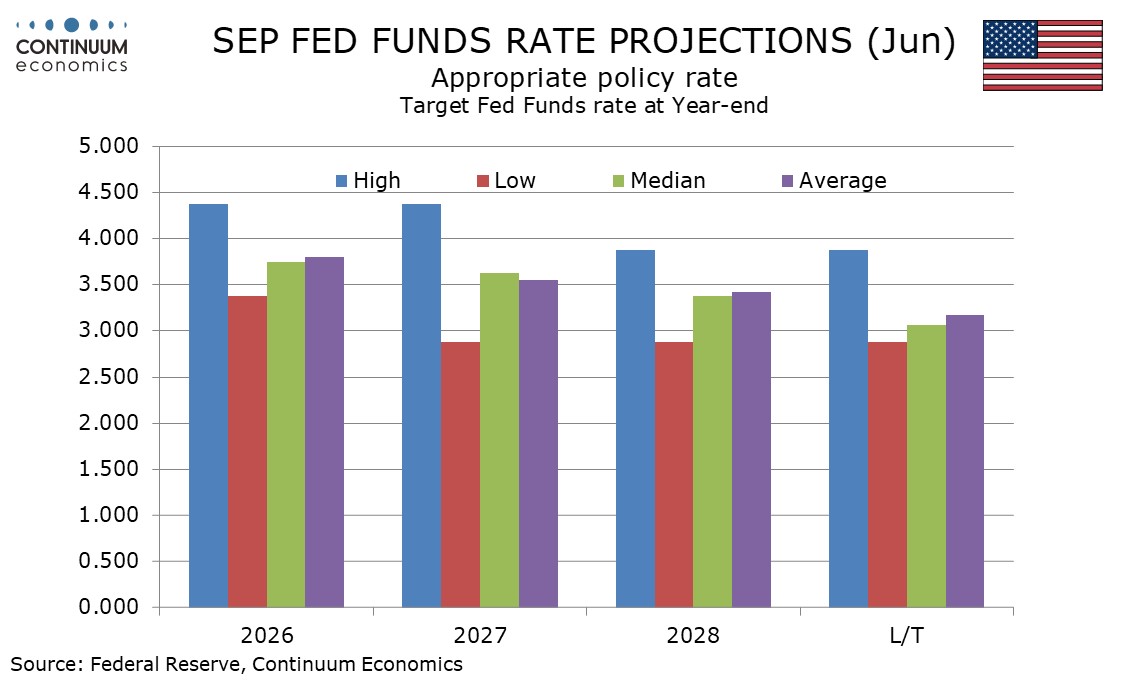

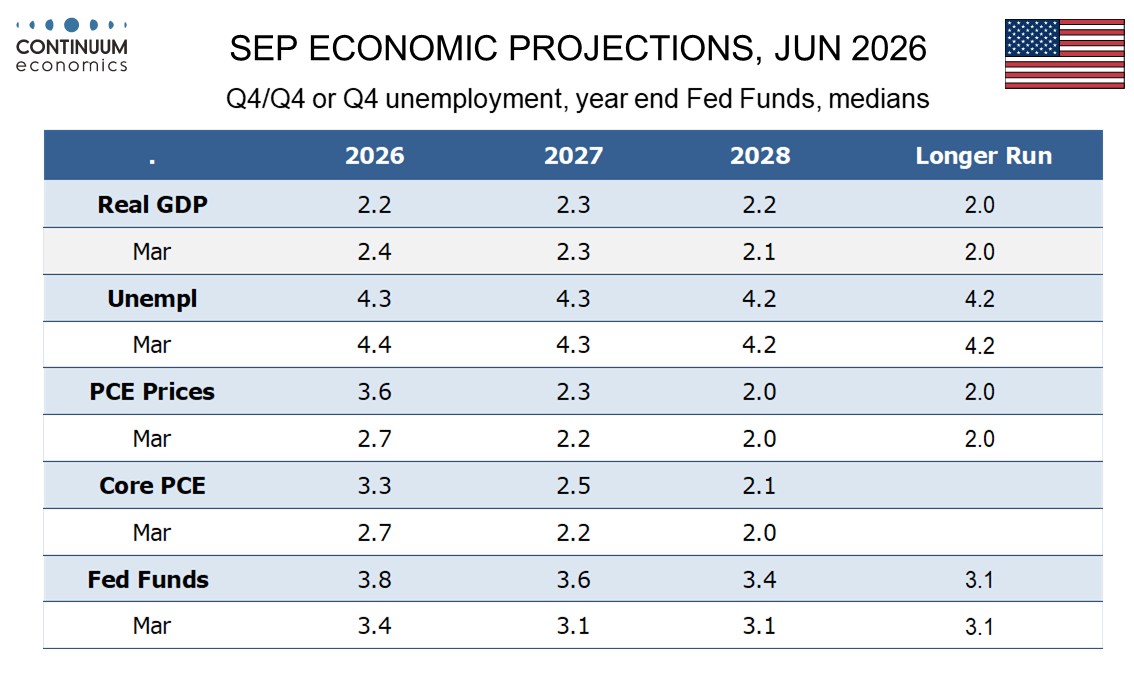

The last meeting on June 17, the first under incoming Chair Kevin Warsh, saw rates left unchanged at 3.5-3.75% with no dissenting votes, but the dots had a hawkish skew, with nine out of eighteen respondents seeing tightening this year, and only one seeing an ease and eight seeing steady policy. Minutes from the meeting showed two scenarios were discussed. The first saw inflationary pressures dissipating and inflation soon beginning to return to 2%, in which it would be appropriate to maintain or eventually lower the target range for rates. The second saw stable labor market conditions and persistent elevated inflation, under which some policy firming would be needed.

A slightly softer than expected June non-farm payroll still leaves labor conditions as stable, with the unemployment rate actually slipping on a fall in the labor force, but a significantly softer than expected unchanged June core CPI does provide hope that inflationary pressures are starting to cool. Governor Christopher Waller before the CPI release suggested that that release could be crucial in determining whether a rate hike was needed in June. We believe Waller’s views will be close to the median on the FOMC and that suggests the FOMC will not see a need to tighten at the coming meeting. We would be surprised if any of the permanent voters dissent from a decision to leave policy unchanged, though we suspect Governor Michael Barr has a hawkish lean. Potential dissents come from regional Fed presidents, Cleveland’s Beth Hammack, Dallas’ Lorie Logan, and less likely, Minneapolis’s Neel Kashkari. Philadelphia’s Anna Paulson is likely to go with the majority.

Under previous Chair Jerome Powell, a statement with a tightening bias would probably have been produced under current circumstances, suggesting that tightening may be necessary if inflation data delivers renewed disappointments after the soft June, while several months of soft inflation data are likely to be needed before easing is considered, as was conveyed by Waller’s recent speech. However this time the statement is likely to see little change from the last one, avoiding forward guidance.

Warsh’s press conference is likely to continue to avoid forward guidance but he is likely to provide a somewhat hawkish tone, seeing inflation as too high but the labor market close to where the Fed would like. Warsh is likely to be reluctant to tighten, being of a view that strong productivity will contain inflation in the long run, but is likely to recognize that his credibility would suffer if he does not respond should inflation prove persistent in the second half of the year. Many at the Fed believe that in the short run, strong business investment is generating demand that is lifting inflationary pressure and potentially the neutral rate. We continue to expect steady policy through 2026 and 50bps of easing in 2027, though that is dependent on core inflation slowing in the second half of 2026 and moving towards the 2.0% target by mid-2027.