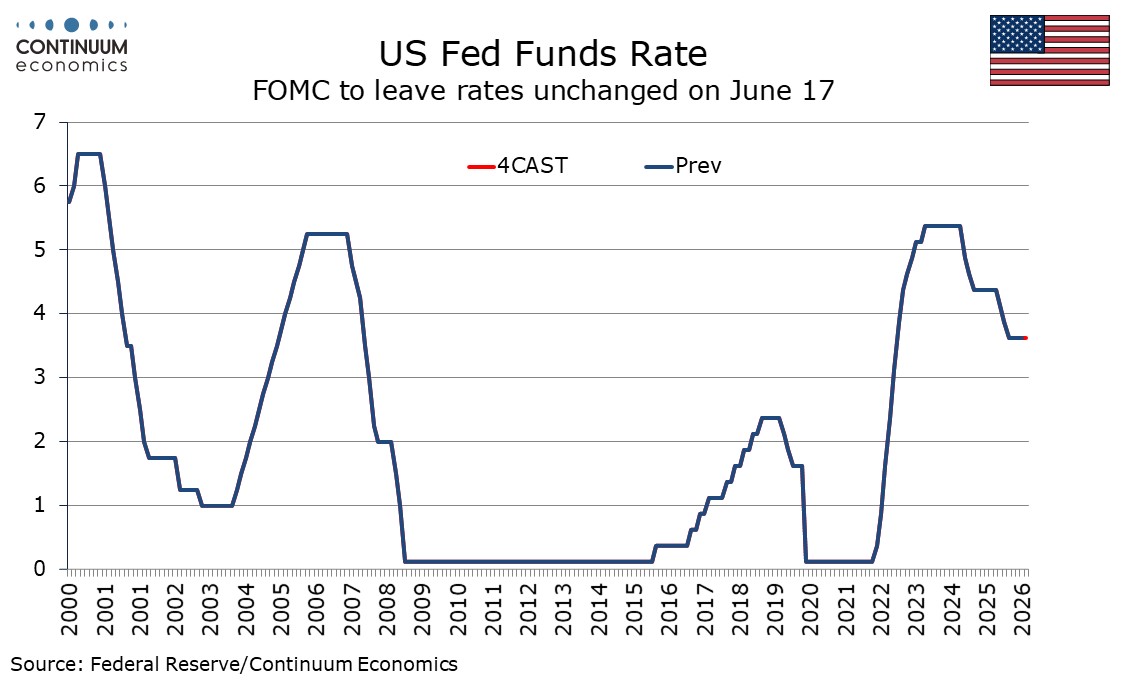

FOMC Preview for June 17: Dropping the easing bias

The FOMC meets on June 17 and while a change in the Fed Funds target range from the current 3.5-3.75% is unlikely, the statement is likely to drop the easing bias. The median dots are likely to get a little more hawkish with a hawkish skew in the detail, with inflation forecasts, even ex food and energy, likely to see a significant near term upward revision. The post-meeting press conference will be of particular intertest, being the first from incoming Chair Kevin Warsh. He is likely to be less hawkish than some will feel upgraded inflation forecasts would justify.

The Statement

The last meeting on April 17 saw three hawkish dissents, from Cleveland Fed’s Beth Hammack, Minneapolis Fed’s Neel Kashkari, and Dallas Fed’s Lorie Logan, who wanted to drop an easing bias. Governor Stephen Miran dissented for an easing but he has now left the FOMC. Then Chair Jerome Powell hinted at the press conference that others were inclined to drop the easing bias, and minutes from the meeting stated that many were. This is likely to happen at this meeting, though given high levels of uncertainty the statement is more likely to be open to moving rates in either direction rather than giving an explicit tightening bias.

It is possible the arrival of a new Chair will see the format of the statement altered, though we are not assuming that. The assessment of the economy warrants a hawkish adjustment, with three straight healthy payroll gains suggesting job gains should no longer be described as remaining low, though the unemployment rate remains little changed in recent months as was started in April. April saw inflation described as elevated. It may be described as increasingly so in June, even with May’s core CPI providing some relief. That economic activity has been expanding at a solid pace still looks valid given positive early forecasts for Q2. We expect the statement to be approved unanimously with none explicitly calling for a hike. Governor Michele Bowman is a possible dovish dissent having stated that it was right to maintain the easing bias in April, though Governor Christopher Waller, who like Bowman turned dovish in 2025, has stated it should be removed. Warsh may have a lean to maintain an easing bias, but is unlikely to give a dissent against the majority view in his first meeting as Chair.

The dots and the SEP

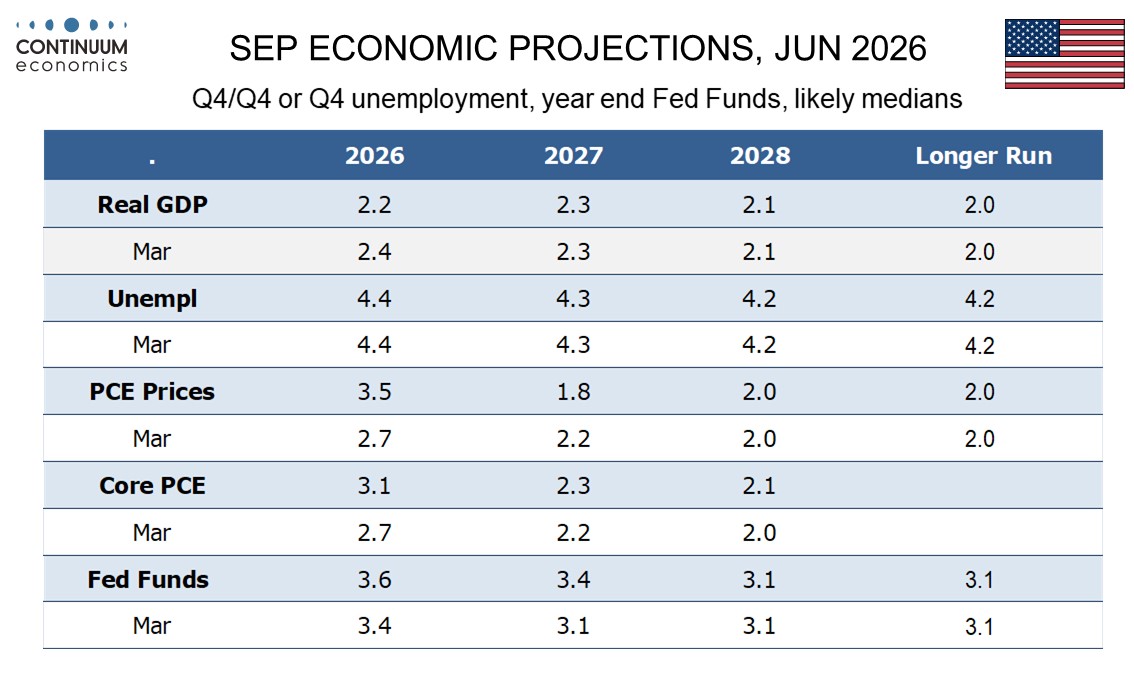

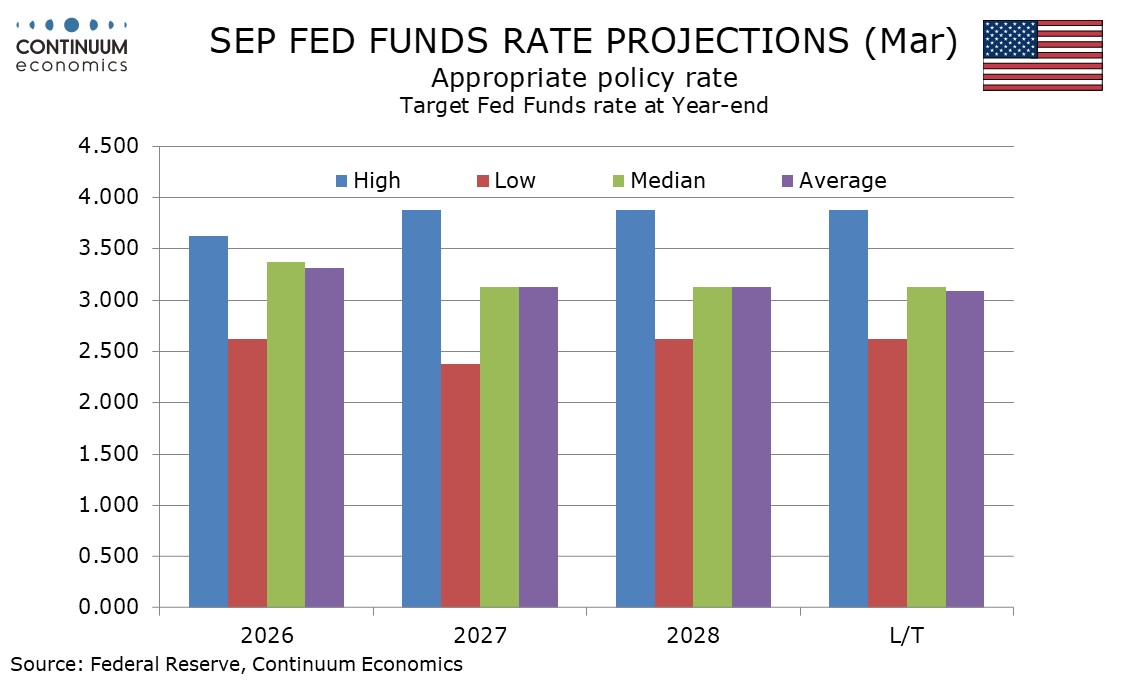

We expect the dots will show a median view of no change in policy this year, compared to one 25bps easing when the dots were last updated on March 18, while still seeing one 25bps easing in 2027, though this would leave the year end dot at 3.375% rather than 3.125%. We expect 2028 to see a drop to 3.125% which is where the it and the long run neutral rate was seen in March.

In March seven participants saw no change in rates in 2026 while seven were on the then median of one 25bps easing. Three of those need to shift to no change to nudge the median higher. We however expect most participants to shift their 2026 view in a hawkish direction, such that there will be a hawkish skew to the 2026 dots, with more seeing a tightening than an ease. Only two need to shift their 2027 dots higher to shift the median, so that looks likely. However, we expect a majority will see rates slightly lower at the end of 2027 than in 2026 with the energy spike likely to be at least party corrected by then and the impact of tariffs also likely to have faded. The dots for 2028 and the long run were reasonably balanced in March around medians of 3.125%, with a marginally hawkish skew for 2028 and a marginally dovish one for the long run view which in March was revised up from 3.0%.

There may be some debate around the long run at this meeting with Warsh feeling that productivity gains will reduce inflation and potentially the neutral rate over the longer term, but he will have trouble convincing the majority at the Fed on this. In March the longer run GDP view was revised up to 2.0% from 1.8% which is likely to reflect technological advances, and that is probably why the median long run interest rate was nudged higher, with strong expected investment demand lifting the neutral rate. Given that the long run view was revised in March a further update is unlikely this time.

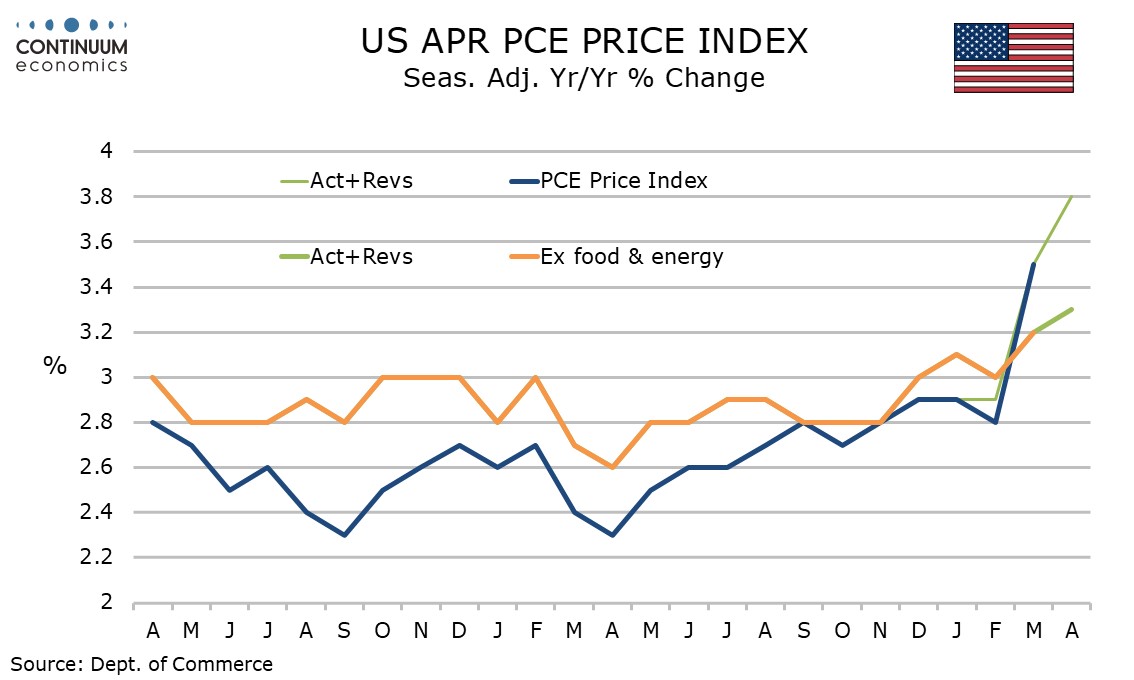

The hawkish shift in the 2026 dots will be largely on the near term inflation picture. March’s year end forecasts of 2.7% for both overall and PCE prices, respectively revised from 2.4% and 2.5% in December, now look significantly too low, with April’s respective outcomes being 3.8% and 3.3%. Some slowing of energy prices may be assumed in the second half of the year but only limited progress will be seen on core PCE prices, which we expect will be seen ending 2026 at 3.1%, with overall PCE prices higher still at 3.5%. On an annualized basis however, core PCE prices will be seen below 3.0% in the second half of the year, as the lift from tariffs as well as energy fade. This will leave scope for a significant slowing in 2027, though that year may be still be revised marginally higher from 2.2%, while even 2028 may be seen slightly above the on target 2.0% that was seen in March.

The lift to energy prices may see GDP in 2026 revised marginally down from March’s forecast of 2.4%, but we do not expect much change to the 2027 view of 2.3% and the 2028 view of 2.1%. We expect the 2026 year end unemployment forecast to remain at 4.4%, slightly above the current level of 4.3%, with the strong non-farm payroll growth seen in the three months to May difficult to sustain. Again, we expect little change to the 2027, 2028 and longer run views. These forecasts could argue for the Fed making it clear that risks to inflation outweigh those to growth, and signaling a tightening bias, but given elevated uncertainty the Fed is more likely to simply shift to a neutral from an easing bias.

The press conference and the outlook

Incoming Chairman Warsh will face a challenging press conference in which he may be torn between a desire to gain credibility with the markets by taking the upside risks to inflation seriously enough to imply that tightening is a significant risk, while also noting the clear desire of President Trump, who appointed him, for lower rates. Warsh’s views are likely to lean on the dovish side, and he can give valid arguments against a rush to tighten, noting high uncertainty, the temporary nature of some inflationary pressures and an optimistic but controversial view of the benefits of productivity gains. His desire to reduce forward guidance may also be convenient in justifying a lack of a bias, though stressing this too much could allow markets to see near term tightening risk even in the absence of a bias.

He will need to be careful to reflect the views of the FOMC. The FOMC has at least one remaining dove amongst the Governors in Bowman, while New York Fed’s Williams, a permanent and influential voter is still sounding quite moderate, as does Governor Philip Jefferson. Of the remaining Governors Waller has become less dovish but is not yet hawkish, Lisa Cook is still moderate but seems to be getting more hawkish, while Michael Barr has a hawkish lean. Outgoing Chair Powell remains a governor, and moderate, and would be unlikely to lead opposition to his successor. Three of the four rotating voters, Hammack, Kashkari and Logan, signaled their hawkishness with April dissents. The fourth, Philadelphia Fed’s Anna Paulson, remains moderate.

There is still a moderate majority on the FOMC voters though several of the non-voting district presidents are hawkish. If inflation shows no sign of easing in the second half of the year and unemployment remains stable, tightening pressure will increase, though we feel that the path of least resistance will be to leave rates unchanged through 2026, particularly as we expect weakening real disposable income growth to see consumer spending lose momentum further. Policy will be described as moderately restrictive, thus putting downward pressure on inflation. We revised our view for two easings in 2026 to one (in December) after the April meeting and now believe that a December move is unlikely, even if, as our central scenario assumes, that the Strait of Hormuz reopens in the summer. Inflation moving closer to target in 2027 should allow easing to resume, though the Fed is likely to need confirmation that core PCE prices in early 2027 do not repeat early 2026 strength before moving. We expect a move in Q2 2027, followed by another in Q3. That would take the rate to neutral sooner than we expect the FOMC’s June dots to predict. Policy will be heavily guided by incoming data.

Warsh does want to trim the Fed’s balance sheet, and is likely to initiate some discussion on this at the meeting, but we doubt any decisions will be made. The issue is unlikely to be addressed in the statement, or significantly at the press conference, though there may be some useful insights when minutes of the meeting are released. Hawkish Kansas City Fed President Jeffrey Schmid has stated that the balance sheet could be used to create policy restriction, an option that could appeal to Warsh if he wants to fight inflation without fighting Trump, though he may have trouble getting majority support for this. Fed attempts to trim the balance sheet in 2019 led to tensions in money markets, ultimately contributing to Fed easing.