China: Divided Economy

· Overall, growth remains unbalanced. Momentum in AI/automation leads economic growth, with support from net exports still. However, consumption is not consistent with a 5% growth pace, as adverse wealth effects and a soft labor market mean only modest consumption. While the stimulus announced in March is helpful, it is the same size as 2025. Overall, the underlying momentum for 2026 leaves us forecasting 4.4%. For 2027, we see a further trend slowing to 4.2%, as the structural headwinds to consumption get larger and a soft labor market ingrains cautious among consumer.

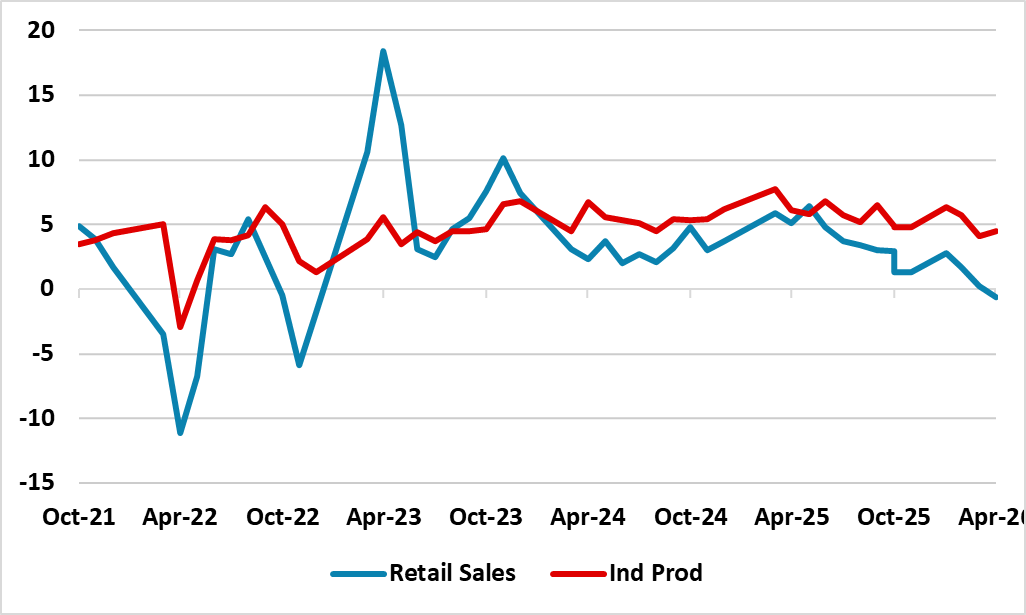

Figure 1: Industrial production and Retail Sales (Yr/Yr %) Source: Datastream/Continuum Economics

Source: Datastream/Continuum Economics

The May China data shows a divided economy between production/exports and domestic demand. Key points to note.

• Negative retail sales Yr/Yr. The -0.6% decline versus May 25 is awful. It was depressed by weakness in goods that had previously benefitted from trade in programs. Even so, auto sales maintain the weak trend, as in recent months. Tourism and catering were also soft during the month, which included a 5 day holiday period. China’s consumer are still suffering from the adverse wealth effect from the cumulative large house price decline, given that household wealth remains dominated by housing. Additionally, households are also concerned about current and future income prospects, with private sector employment growth weak. NBS did provide a headline for a new goods and services consumption measure, which showed that services held up better in the first five months of 2026. Even so, the retail sales trend (Figure 1) is worrying.

• Residential construction worse. Residential investment fell -16.2% Yr/Yr YTD versus -13.7% in April, with poor property sales figure and further falls in house prices. This all suggests that the authorities hopes of a bottom in the housing market are premature. Though the early spring has seen some improvement in house purchases in tier 1 cities like Shanghai and Shenzhen, the wider picture including tier 3 cities remains weak. Firstly, a large inventory of complete and uncomplete property continues to curtail the interest in starting new residential construction. Secondly, households' property optimism has been significantly dented by the bust of the last few years.

• Industrial production and exports good. A 4.5% rise in May industrial production Yr/Yr was better than expected and led by a 15.1% surge in high tech manufacturing (AI/tech to green energy). The May export figures last week showed a nominal 19.4% Yr/Yr surge helped by exports of high tech goods, so the industrial production resilience is partially driven by exports. Even so, the EU is becoming concerned about the surge in China exports, which could temper future growth.

Overall, growth remains unbalanced. Momentum in AI/automation leads economic growth, with support from net exports still. However, consumption is not consistent with a 5% growth pace, as adverse wealth effects and a soft labor market mean only modest consumption. While the stimulus announced in March is helpful, it is the same size as 2025. Overall, the underlying momentum for 2026 leaves us forecasting 4.4%. For 2027, we see a further trend slowing to 4.2%, as the structural headwinds to consumption get larger and a soft labor market ingrains cautious among consumer. As always it could also be that the reported GDP numbers are higher (to hit the 4.5-5.0% target) than the actual reality, as this still remains the political bias for good news messaging.