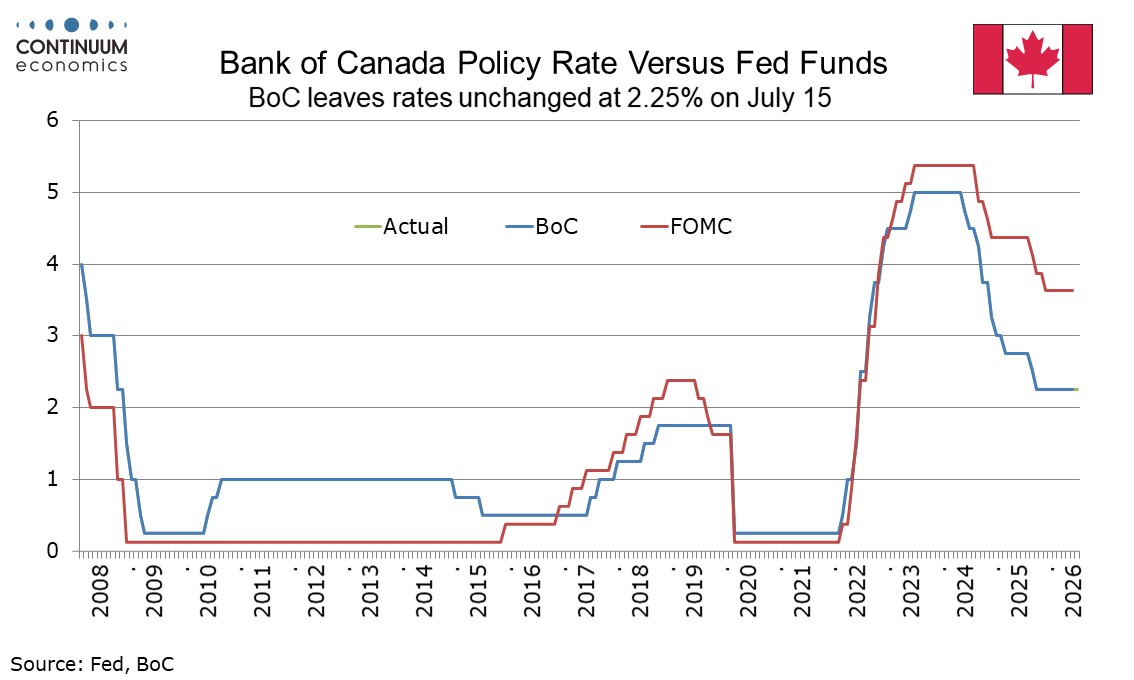

Bank of Canada - Near term policy change looks less likely

The Bank of Canada left rates unchanged at 2.25% as expected and while expressing increased optimism over the Canadian economy, does not appear in any hurry to change rates. The statement did state the BoC was prepared to adjust policy as needed but explicit mentions of the possibility of moves in either direction seen after recent meetings were not repeated. We continue to expect unchanged policy through 2026.

After the April and June meetings, Governor Tiff Macklem warned over the possibility of consecutive tightenings on persistent inflation or easing should the US impose fresh tariffs. While Macklem still sees the conflict in the Middle East and the relationship with the United States as the two biggest risks the possibility of policy responses to the alternative scenarios was not stated so clearly. Oil moving off its highs reduces the upside risk somewhat, and while Trump remains unpredictable on trade policy, downside risks from tariffs appear to have been offset by a more positive assessment of the Canadian economy.

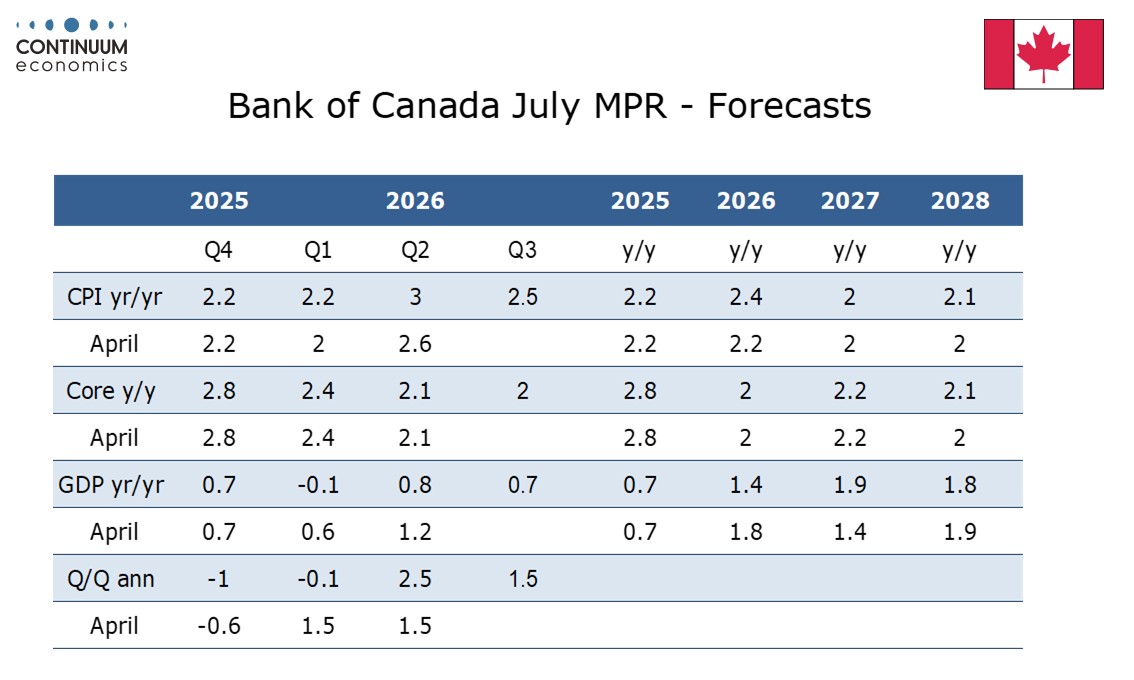

A 2.5% annualized forecast for Q2 GDP, up from 1.5% in April, was not a surprise to us, and 2026 has still been revised down given a weaker than expected Q1, though offset by an upward revision to 2027. Macklem stated that the growth outlook is similar to the April forecast overall but data received since April has increased confidence that the economy is working its way through this period of global upheaval. Macklem expressed some optimism on all the components of GDP, consumer spending, housing, exports, business investment and government.

The 2026 inflation forecast did get an upgrade from April though largely on strength in Q2, with 2027 and 2028 not much changed. Macklem did note that the oil futures curve had moved higher since the forecast was finalized on Friday and the forecast is dependent on oil prices stabilizing between $70 and $75 per barrel. Clearly there are upside risks here, and Macklem saw risk that inflation could get stuck above the 2% target. However this was immediately balanced by noting a risk that the Q2 pick-up in GDP is not sustained, leaving the BoC’s tone far from hawkish. In his press conference Macklem said he would not want to respond to a spike in inflation caused by rising oil prices that then came down, though he did say that the BoC would not allow higher oil prices to become persistent inflation.

While the situation is highly uncertain, we continue to expect the BoC to leave policy unchanged at 2.25% through 2026 before returning rates to 2.75%, the midpoint of the 2.25-3.25% range the BoC sees as neutral. In 2027. We expect 25bps moves to come in Q2 and Q3 of 2027.