FX Daily Strategy: N America, Jun 16th

Since Iran kicked off, gold holds on to the biggest remaining losses, SEK next

BoJ delivers the expected hike, later taper, and minor tweaked statement - little impact seen

RBA likewise largely on-message

Broader dollar tone still waiting on the new era Fed, market tread water prior

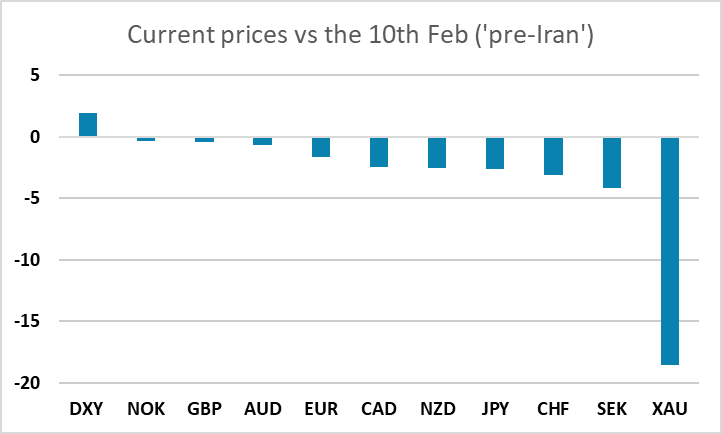

Before turning to the next round of key events, it is worth briefly taking stock of where current prices sit, relative to the pre-Iran levels, to give some basis of comparison if we assume the benign scenario plays out from here (see here for the latest risk scenario odds and implications).

Gold remains the biggest net changer, still down just under 20%, but it has been bouncing. It would need to be back above 4450, so another 100pts, to be regaining the broken 200dma. This is a market where mood had turned extremely bearish having previously been super bullish, so it is prone to contrary sentiment excesses.

Otherwise, it’s SEK as high beta counter that is still down the most on mid Feb, and this is where the most major FX reactiveness has been seen so far as a result, at least as long as broader risk trade is able to sustain its recover as well (i.e. the tech risk bounce holds rather than running into more distribution).

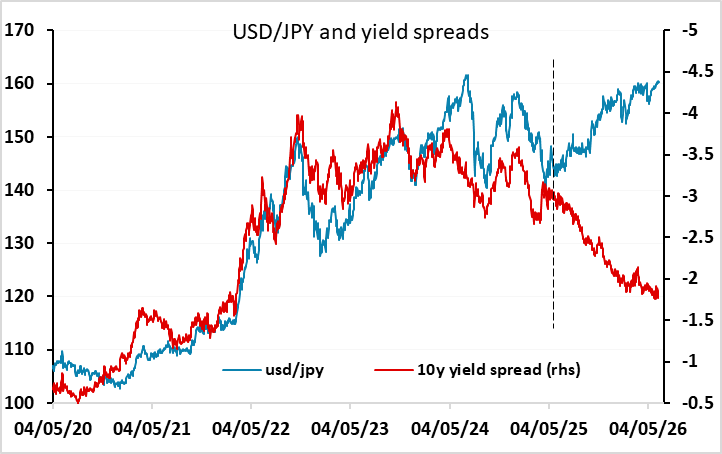

As to whether the yen also has a little room to reset and give up the 160 handle, one event risk has passed and the BoJ failed to provide any great triggers so far coming in as expected - with the 25bp hike, and continuing as is this fiscal year before ending tapering from April.

The statement also didn’t particularly surprise by dropping the reference to rates being ‘significantly low’ while retaining the tightening bias and guidance skew (‘will continue to raise rates and adjust the degree of monetary accommodation in response to developments in economic activity, prices and financial conditions’). It is worth nothing though that the wider statement does note ‘Real interest rates have been negative, mainly in the short- to medium-term zone. Firms' and other entities' demand for funds has increased’ so that still highlights the BoJ’s focus on the policy rate being relatively low, and may need further increases, as long as long end yields are controlled.

That currently leaves the pair for now needing to get impetus from either the FOMC side of the equation, risk tone, or MoF (they may be more in the picture on any fresh upside now the BoJ is out the way, and modest tightening still being delivered).

The RBA also came and went without any great shocks. The 'data dependent hold' was largely as expected, albeit with the tone overall keeping at face value a slightly hawkish skew on inflation risks and possibility of more action needed. It was clear however that they didn’t discuss hikes and were waiting on more data to see if there is substance to the recent softer prints. AUD/USD eased back to 0.7050~ support with a bit of backfilling, but remains in consolidation on the recent minor bounce.

Dollar direction overall though may remain lacking until Wednesday’s FOMC given the unusually large amount of uncertainty and information packed into this maiden Warsh meeting. EUR/USD is back to fairly neutral at the 1.16~ area prior to that, both in terms of levels and in terms of positioning. If Iran relief is sustained, and it further allows the Fed to avoid a stronger hawkish pivot, that could see a little stretch of the bounce (1.1650/70) but momentum isn’t strong.

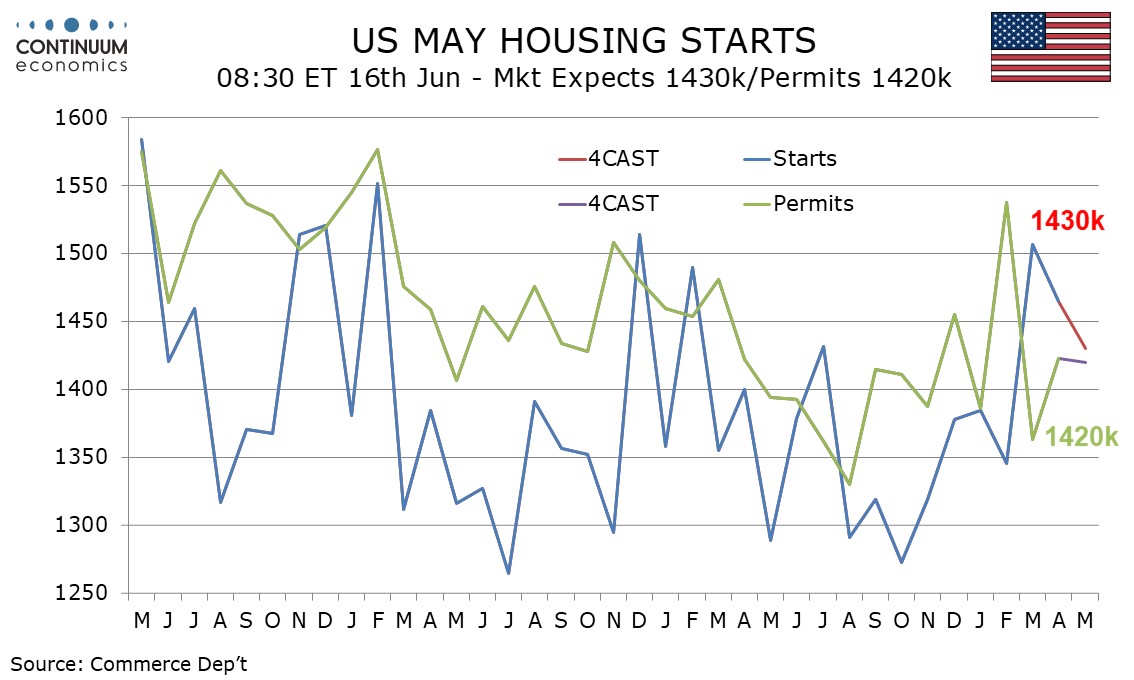

In the US, we expect May housing starts to fall by 2.4% to 1.43m, with permits falling by 0.2% to 1.42m. May import and export prices are also due. The market however is very much in definite on hold mode until the Fed.