China Yuan to 6.65 Then 6.50?

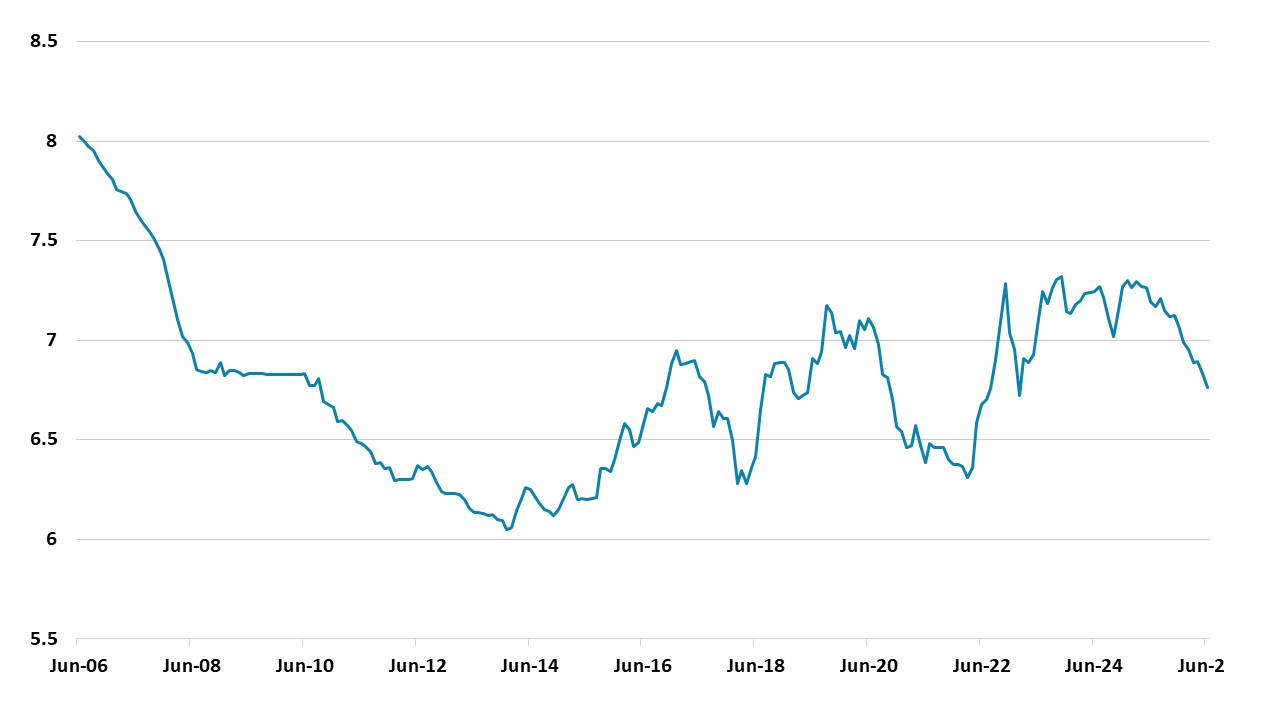

· We feel that the authorities will pause appreciation at times via FX intervention, but then allow appreciation to restart. We now see further Yuan appreciation to 6.65 by end 2026, though the authorities will be reluctant to see much more. For end 2027 we forecast USDCNY at 6.50. China authorities did allow Yuan appreciation in 2014, 18 and 22 (Figure 2), but became sensitive below 6.25. Stepwise this probably translate into a restraint around 6.50 in 2027.

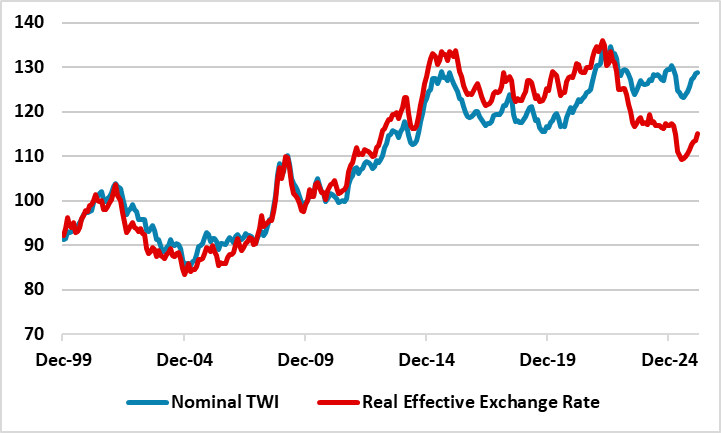

Figure 1: Yuan Nominal Trade Weight Exchange Rate and Real Effective Exchange Rate (Index)

Source: Datastream/Continuum Economics

China authorities are allowing a slow controlled appreciation of the Yuan. The Iran war has so far not hurt China’s economy, with coal/renewables playing a bigger part in electricity production. Additionally, monthly trade data suggests that trade momentum remains into 2026, as China diverts exports away from the U.S. to other countries and also through 3rd countries to the U.S. China’s exports are also being helped by leadership in certain sectors e.g., solar and wind, which are growing sectors globally as renewables help produce cost-effective domestic energy against the backdrop of high geopolitical uncertainty for fossil fuels. Thirdly, the trade truce with the U.S. has been extended after the May summit between presidents Trump and Xi. Trump also seems to place less of a priority on getting a comprehensive trade deal and is happy with commitments that China needs to do anyway, e.g., an order for 200 Boeing planes, which is just above the annual pace prior to Trump 1.0. Though China’s effective tariffs to the U.S. are higher than other countries due to the 2018-19 tariffs, China is competitive. The disinflation in China compared to other countries has meant that the real exchange rate has fallen noticeably in recent years (Figure 1). Overall, a positive contribution should be seen in 2026 from net exports, but lower than in 2025. The U.S. will continue to tighten China exports through 3rd countries, while the EU and major EM countries want to avoid any cheap dumping by China manufactures. Export orders also show a softening with the Iran war.

Figure 2: USD/CNY Exchange Rate

Source: Datastream/Continuum Economics

We feel that the authorities will pause appreciation at times via FX intervention, but then allow appreciation to restart. The reopening of the Straits of Hormuz would make the authorities more willing to accept appreciation. This willingness to allow slow appreciation also appears to be linked by official desire to increase long-term usage of the Yuan. President Xi Jinping's 2024 speech also noted that the yuan should be widely used in global trade, investment, FX markets, and more importantly, have the status of a global reserve currency. We now see further Yuan appreciation to 6.65 by end 2026, though the authorities will be reluctant to see much more. Additionally, the 2yr spread between the U.S. and China also argues for slow further appreciation.

For end 2027 we forecast USDCNY at 6.50. China authorities did allow Yuan appreciation in 2014, 18 and 22 (Figure 2), but became sensitive below 6.25. Stepwise this probably translate into a restraint around 6.50 in 2027. Additionally, China prospective returns for bonds and equities are unattractive for active global investors, even if global benchmarks require passive funds to increase weighting in China. FDI data also shows that inflows have slowed, as the private sector business environment is less positive than the go-go years from 1990-2019. FDI inflows will likely be narrowly focused on AI and Green energy. However, the current account surplus will remain large and this will keep the Yuan firm. We see 6.50 by end 2027.