FOMC Minutes - Fork in the road: scenario-dependent policy

The June Minutes show a Committee that had skewed slightly more hawkish, in pockets, but had mainly moved toward greater uncertainty and dispersion.

The spine of the policy debate now revolves around a fork in the road: two plausible inflation trajectories, with policy calibration in either direction. Inflation risks had broadened, labor market downside had eased, but the outlook was explicitly cast around competing scenarios.

Policy is now scenario-dependent, if you will.

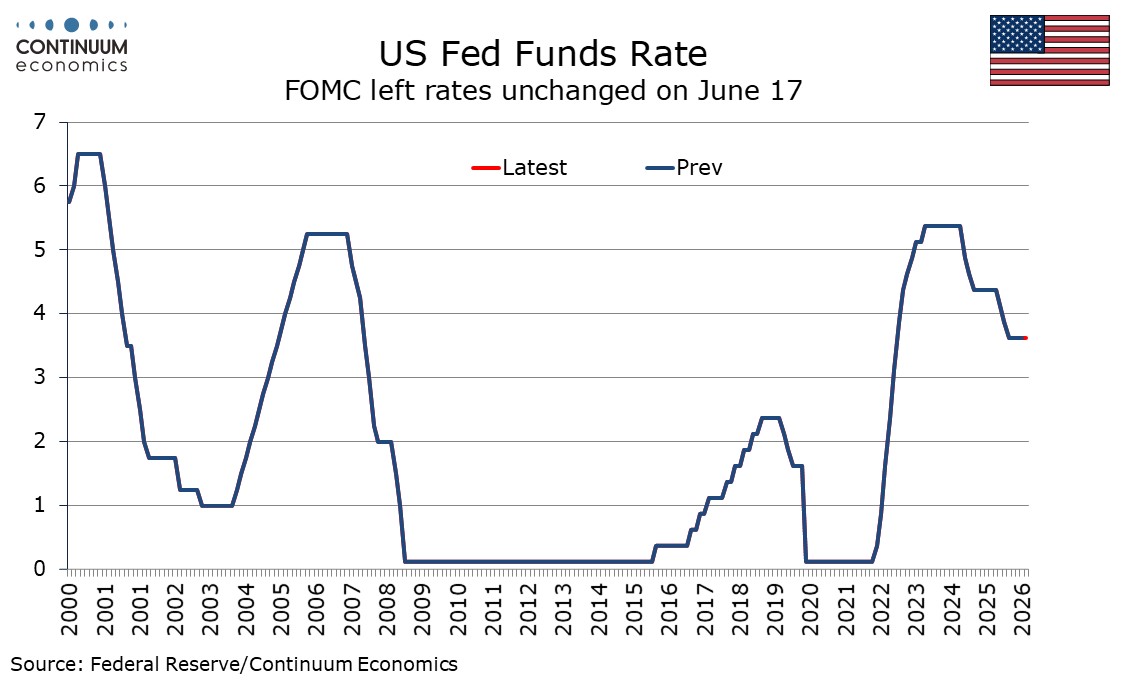

The vote to hold the funds range steady was unanimous, while confirming that most backed dropping the easing bias language, with the majority also seeing advantages in shortening the statement – that might as much reflect the lack of clear direction, as the known broader philosophical stance.

Some hawkish skew was visible in the policy discussion. Participants judged that upside risks to price stability remained elevated, while downside risks to employment had 'moderated a bit.' A few participants saw a case for raising rates, though they supported holding at this meeting. That is perhaps the strongest line that implied a minority tightening bias, if lightly stated.

Several participants did not see the current stance as restrictive, while only a few saw it as slightly restrictive, maybe implying that a minority see neutral real rates as having moved somewhat higher, although it is not put in those terms.

The inflation discussion had more texture. Participants said inflation had “increased further and remained well above” 2%, with pressure linked to tariffs, the Strait of Hormuz disruption, energy and input costs, and AI-related demand. AI received notably explicit treatment as a near-term demand and cost channel: many participants said strong AI infrastructure demand would likely sustain upward pressure on technology products and electricity prices, while most saw AI-driven activity above potential as a possible source of more persistent inflation. Several saw price pressures becoming more broad-based, including transportation, airfares, petrochemical products and agricultural inputs. Several also noted that services inflation excluding housing had declined little and remained high.

There were offsets. The majority saw medium- and longer-term inflation expectations as consistent with the 2% objective, which is fundamental and perhaps the most important constraint on the hawkish read. Several noted caution among firms in raising prices. Housing services were still expected to contribute disinflation. The text also nods to the assumed Warsh view that productivity gains could eventually lift supply and reduce costs, though participants noted that this would likely take time and that the scale and timing of productivity gains remain uncertain.

The labor side no longer gave the Committee much reason to lean dovish. Unemployment was stable, payroll gains had strengthened, and job openings, claims and layoffs pointed to balance. Some participants said earlier concerns about deterioration had eased, and several saw recent payroll strength as possible renewed momentum – though maybe the latest report and revisions might have tempered this view, you could argue. Many still saw wage growth as consistent with inflation returning to 2% moreover.

The broader demand picture was seen firmer, though uneven. Business investment remained strong, heavily concentrated in AI-related spending. Consumer spending looked resilient, helped by stock-market gains and earlier tax refunds, particularly for higher-income households. But the household picture was mixed: lower-income consumers were increasingly relying on credit to sustain spending and remained under pressure from elevated gasoline and grocery prices, something we have emphasised with the declining savings ratio. Very much a K-shaped story reflected in the Committee overview then.

The key policy passage was the scenario framing and split. On one side, the minutes said that 'most participants remarked on scenarios in which inflationary pressures would dissipate and inflation would soon begin to return to 2%.' In those scenarios, 'almost all' thought it would likely be appropriate to maintain or eventually lower rates. On the other side, 'most participants, however, also pointed to scenarios' in which inflation would remain elevated because of AI demand, the Middle East conflict, or tariffs. In those scenarios, 'almost all' thought some policy firming would likely be warranted.

That casts the outlook as a very clear conditional case between tightening on inflation persistence or pause and resume the end of the easing cycle in due course if not. This tends to emphasis that inflation prints will be the critical release in coming months while also that any fresh supply constraints on the back of recent Iran escalations would be material.

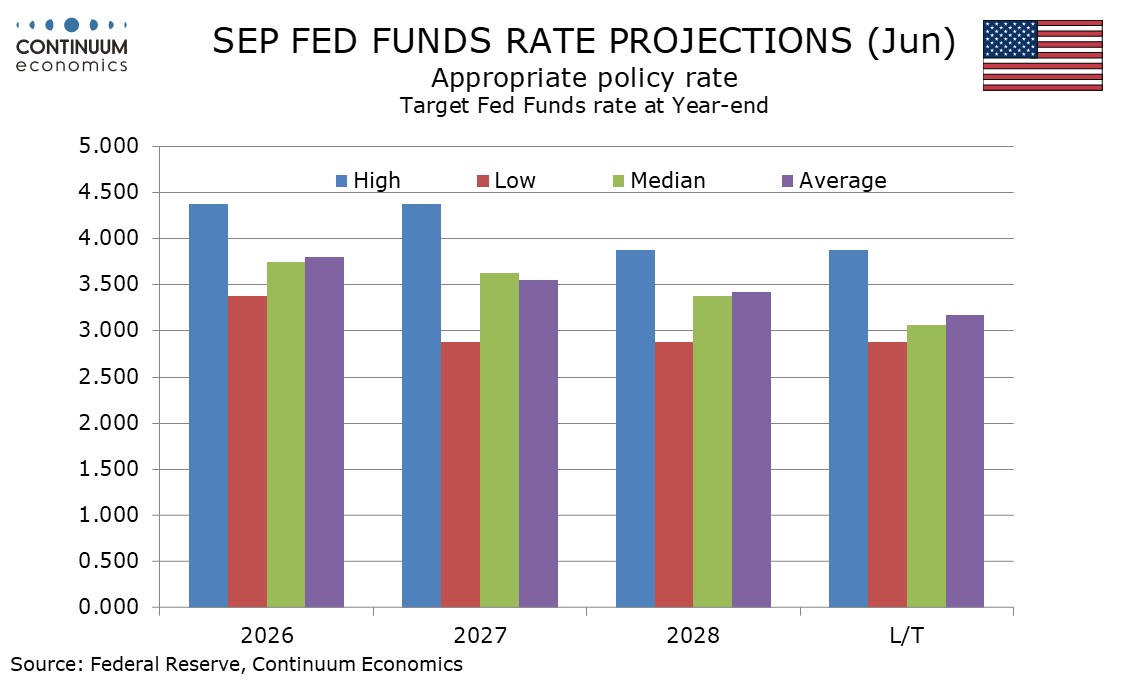

Separately, participants' own most-likely rate paths were meaningfully split. Many saw the appropriate funds rate within or slightly below the current range at year-end, while many other participants saw it above the current range. Both reliant on incoming information.

One last footnote in passing - the taskforces were not given any fresh colour at this point, with just the shortest of passing references to the 'Chairman describing plans to establish them'. These may well prove highly influential in due course but for now can only be speculated on in terms of their direction and motivation.

The clean read is perhaps that the Fed has moved beyond just repeating the cliché non-guidance language of data dependence and into a more explicitly scenario-dependent framing. That backdrop makes forward guidance not only less favoured at the top, but also less useful when the central policy stance is defined by state dependency and genuine uncertainty over the near-term balance of supply and demand, and global developments.