U.S. Personal Income and Spending, GDP, Durable Goods Orders, and Initial Claims - Mostly firm but consumer spending revised lower

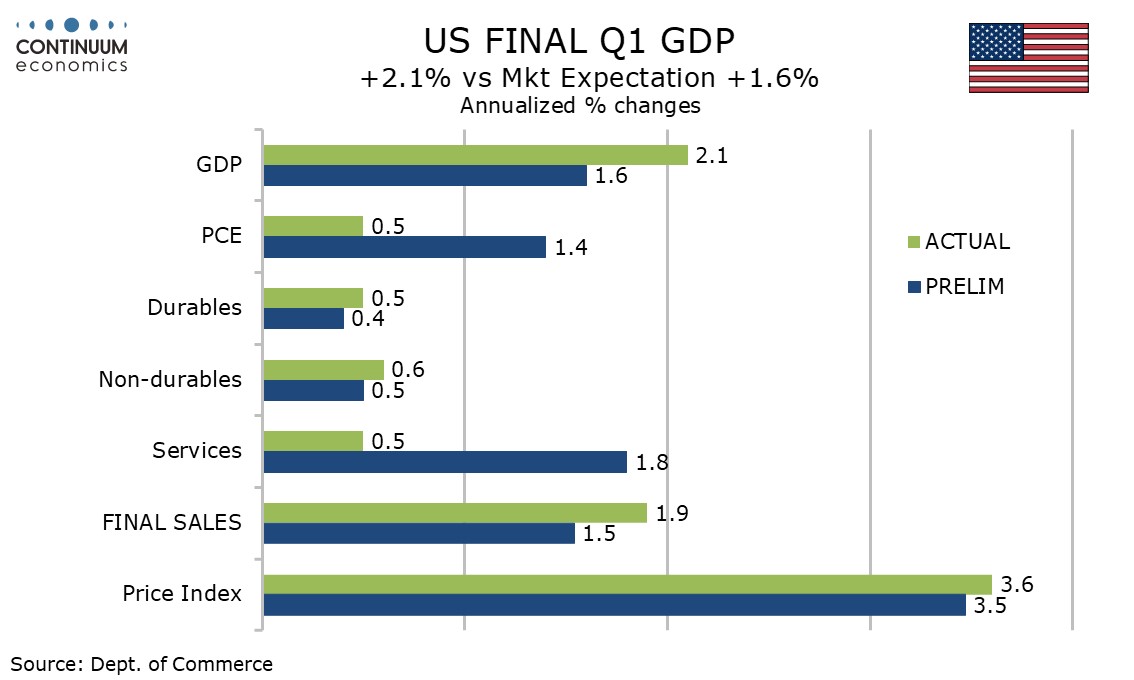

The latest US data is mostly strong, with an upward revision to Q1 GDP, stronger than expected May personal income and spending, still firm core PCE prices, lower initial claims and strength in May durable goods orders outside a fall in transport. However the Q1 GDP revision was mixed, with a significant downward revision to consumer spending. The upward revision was led by net exports.

Q1 GDP was revised up to 2.1% from 1.6%, but consumer spending was revised down to 0.5% from 1.4%. The revision was fully due to services, now at 0.5% from 1.8%. Retail was revised slightly higher, durables to 0.5% from 0.4% and nondurables to 0.6% from 0.5%, but both remain subdued.

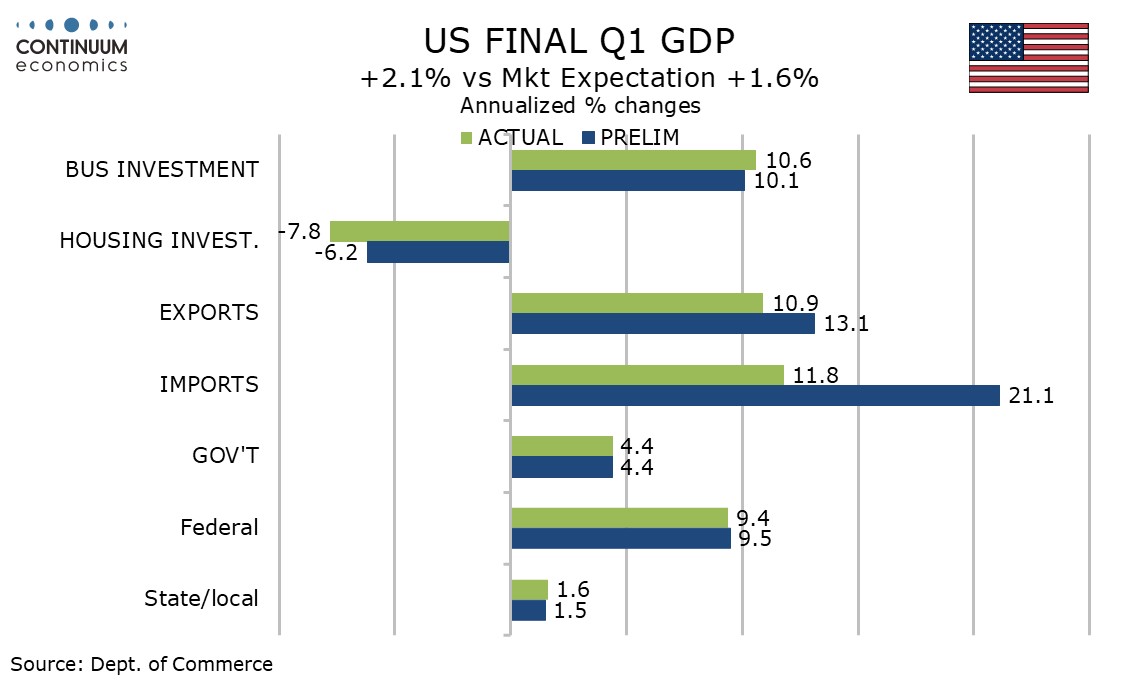

The downward revision to consumer spending was however more than outweighed by an upward revision to net exports. Exports were revised down to 10.9% from 13.1%, the negative revision almost entirely on services, but imports were revised down sharply to a still firm 11.8% from 21.1%, here both goods and services were revised sharply lower.

Final sales (GDP less inventories) saw a similar upward revision to GDP, to 1.9% from 1.5%, but final sales to domestic buyers (GDP less inventories and recent exports) were revised down to 2.2% from 2.7%. Other revisions were modest. Business investment was revised slightly even higher led by intellectual property but housing is increasingly negative. Revisions to government were minimal.

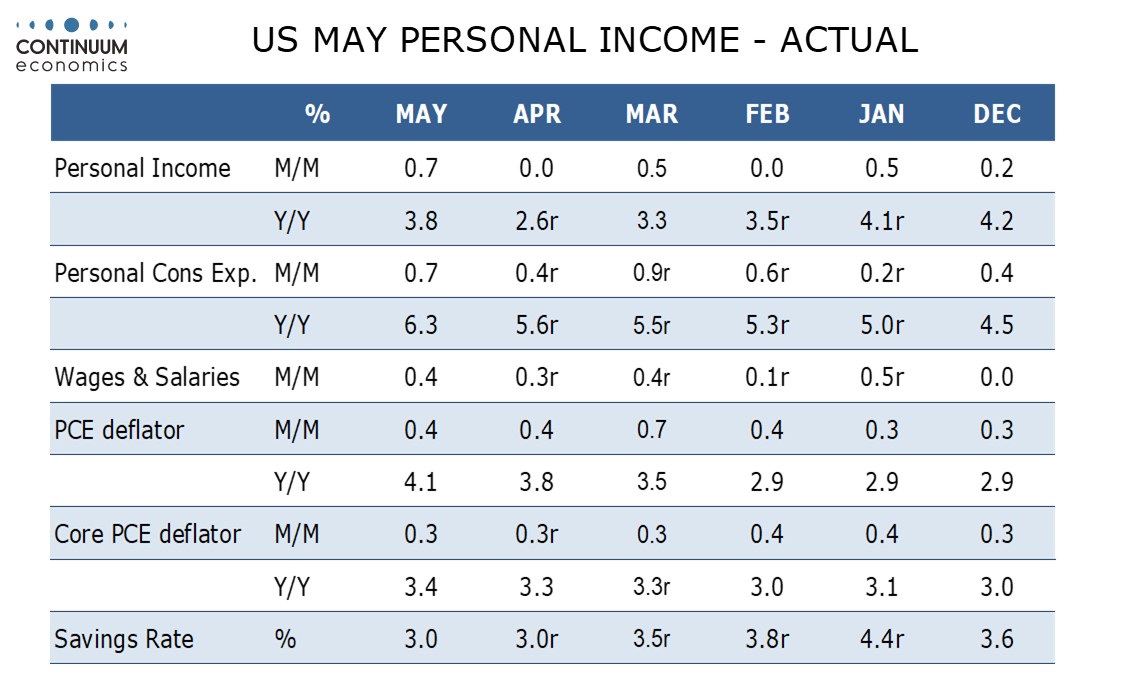

The consumer spending revisions are reflected in the personal income and spending data for May, with personal income revisions being minimal. April personal spending was also revised down, to 0.4% from 0.5%, offsetting a modest upward surprise in May personal spending, which rose by 0.7% in nominal and 0.3% in real terms. May services rose by 0.6% in nominal and 0.2% in real terms.

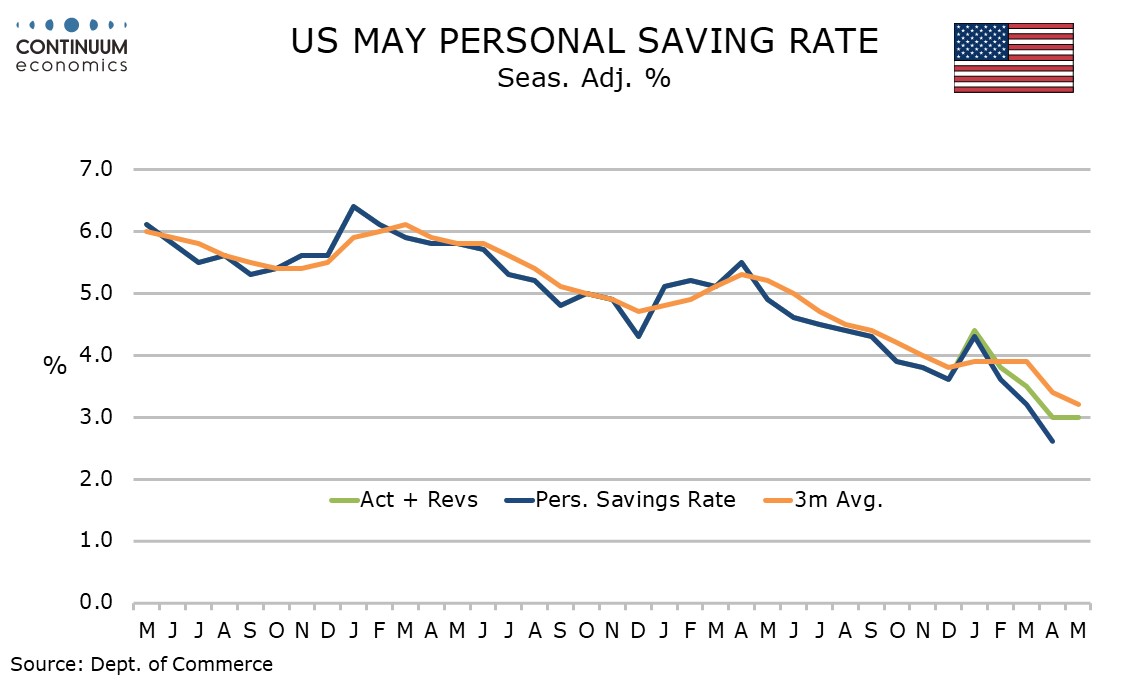

May personal income also rose by 0.7%, this significantly above expectations. Wages and salaries rose by only 0.4% with overall personal income lifted by a sharp rise in farm incomes on a second round of supplemental disaster relief (the first round came in March). The savings rate now stands at 3.0%, unchanged from April which was revised up from 2.6%. The rate is still the lowest since the post-COVID low of 2.2% seen in April 2022, but less weak than previously appeared to be the case. On a yr/yr basis, real disposable income is unchanged, while real personal spending is up by 2.1%.

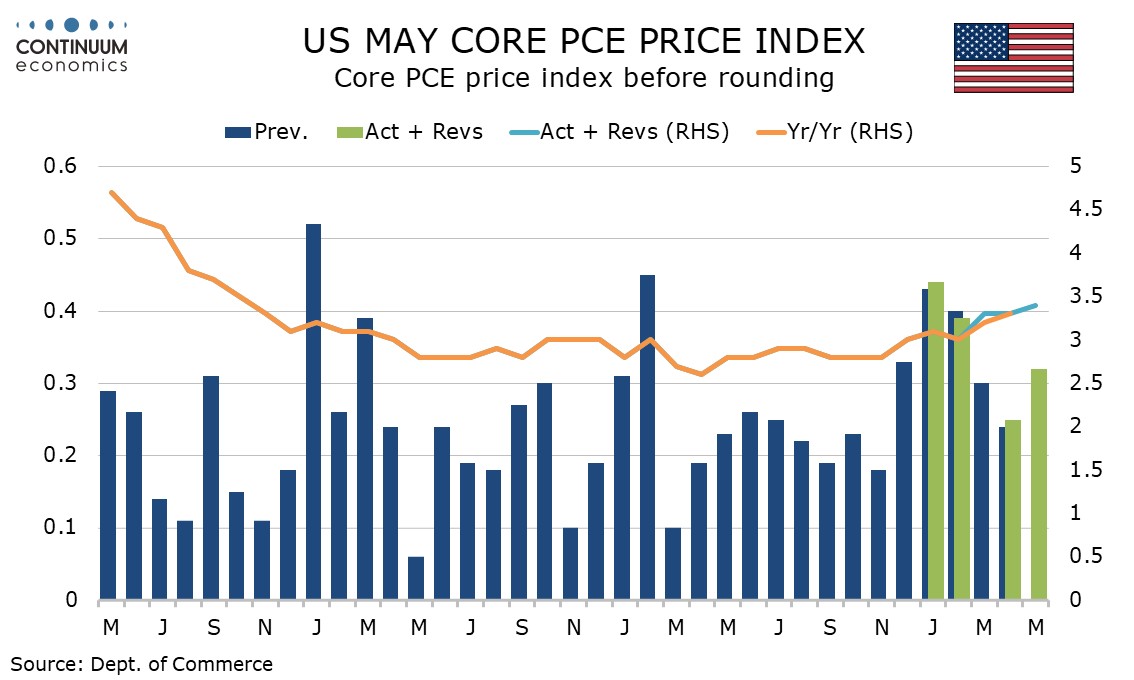

May’s PCE price gains of 0.4% overall and 0.3% in the core rate ex food and energy were in line with expectations, though the core rate was on the firm side at 0.32% before rounding. April’s core rate was revised to 0.3% from 0.2% but remains close to 0.25% before rounding. Q1 core PCE prices were unrevised at a still firm 4.4% but overall PCE prices were revised up to 4.6% from 4.5%. May’s yr/yr data shows core PCE prices at 3.4% from 3.3%, the highest since October 2023, and overall PCE prices at 4.1% from 3.8%, the highest since April 2023.

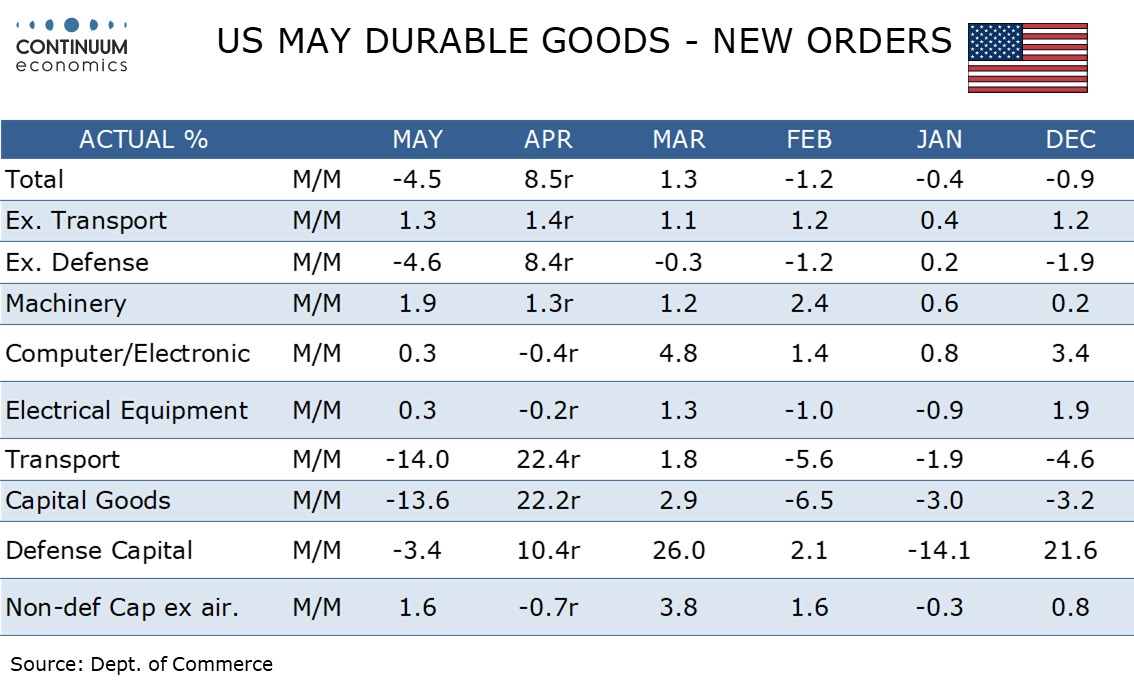

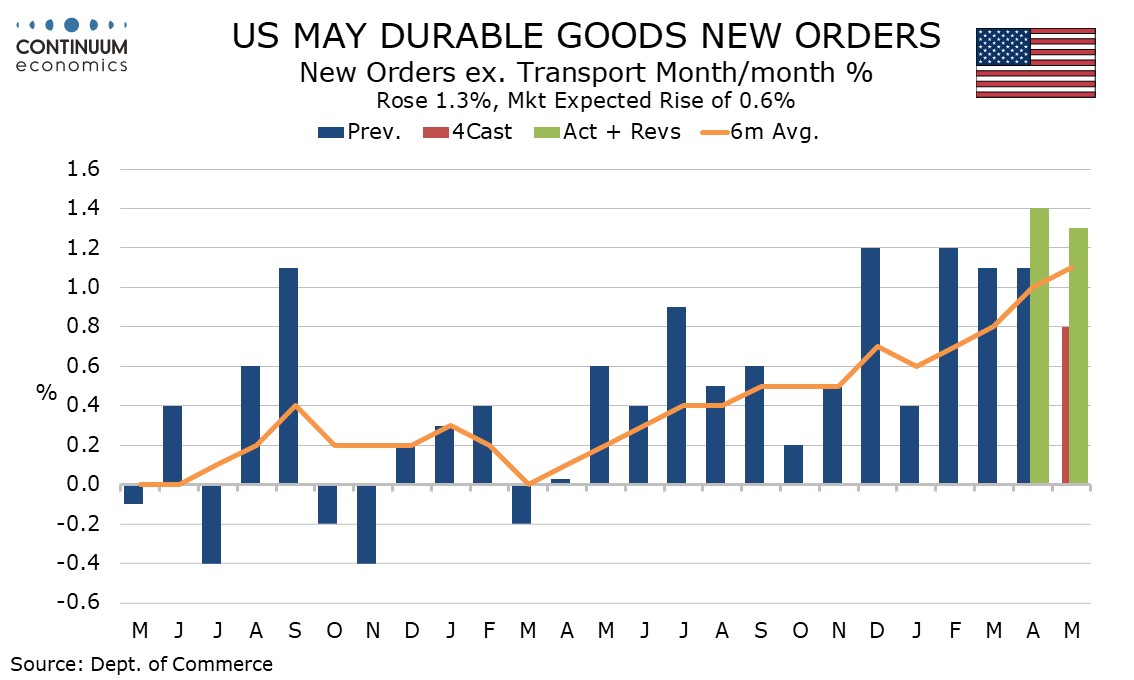

May durable goods orders fell by an as expected 4.5% as aircraft returned to normal after a very strong April when overall durable goods orders surged by 8.5% (revised from 8.0%). However ex transport orders exceeded expectations with a rise of 1.3% after a 1.4% April gain (revised from 1.1%). This means four straight gains in excess of 1.0% and five in six months. Non-defense capital orders ex aircraft were also solid at 1.6%, implying continued strength in business investment.

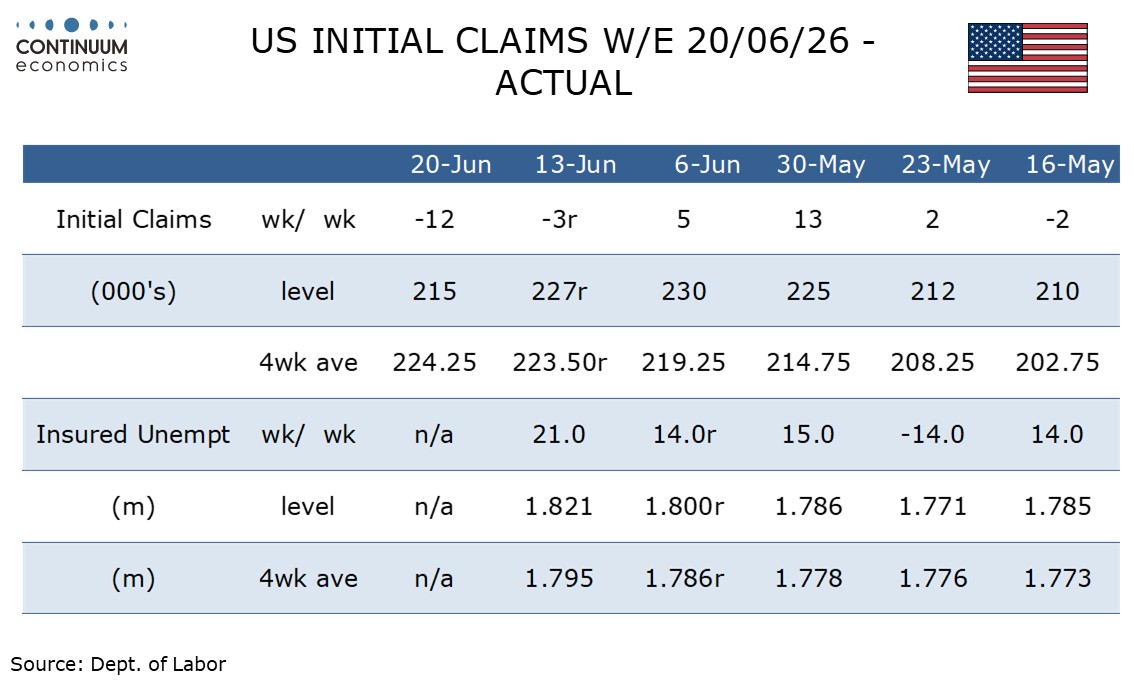

Initial claims at 215k from 226k are at a 4-week low, though the Juneteenth holiday may have played a part in this. The 4-week average of 224.25k is the highest since November. Continued claims, covering the week before initial claims, rose by 21k to 1.821m, the highest since March 28.