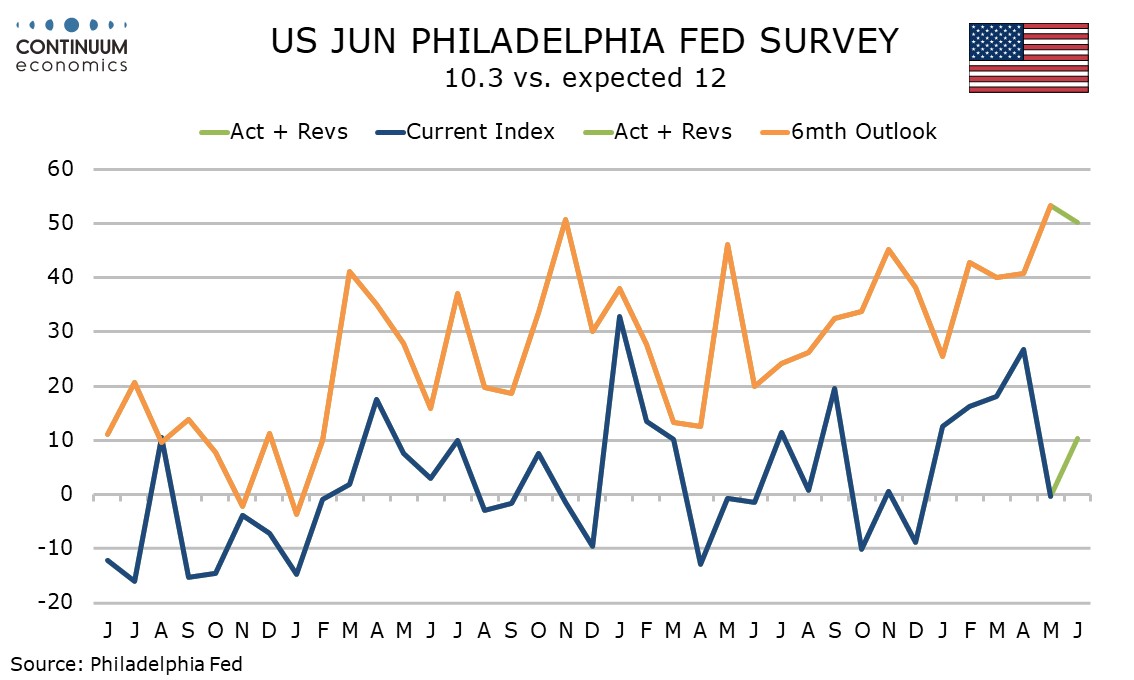

U.S. Initial Claims, June Philly Fed - Slightly improved but some signs of fading momentum

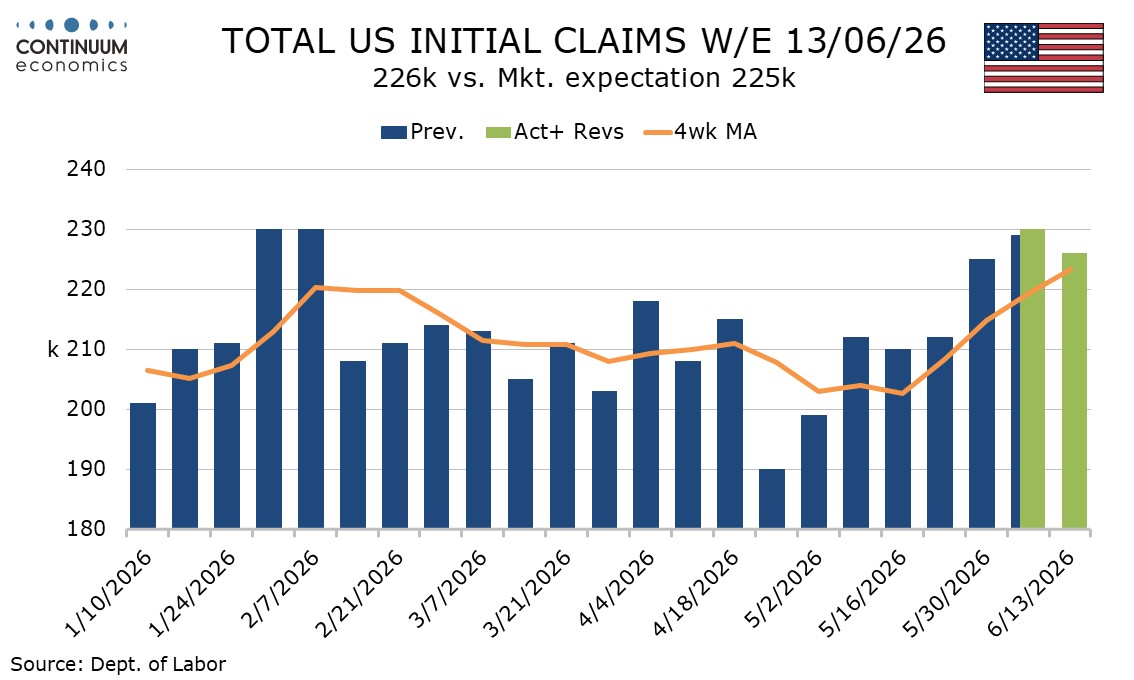

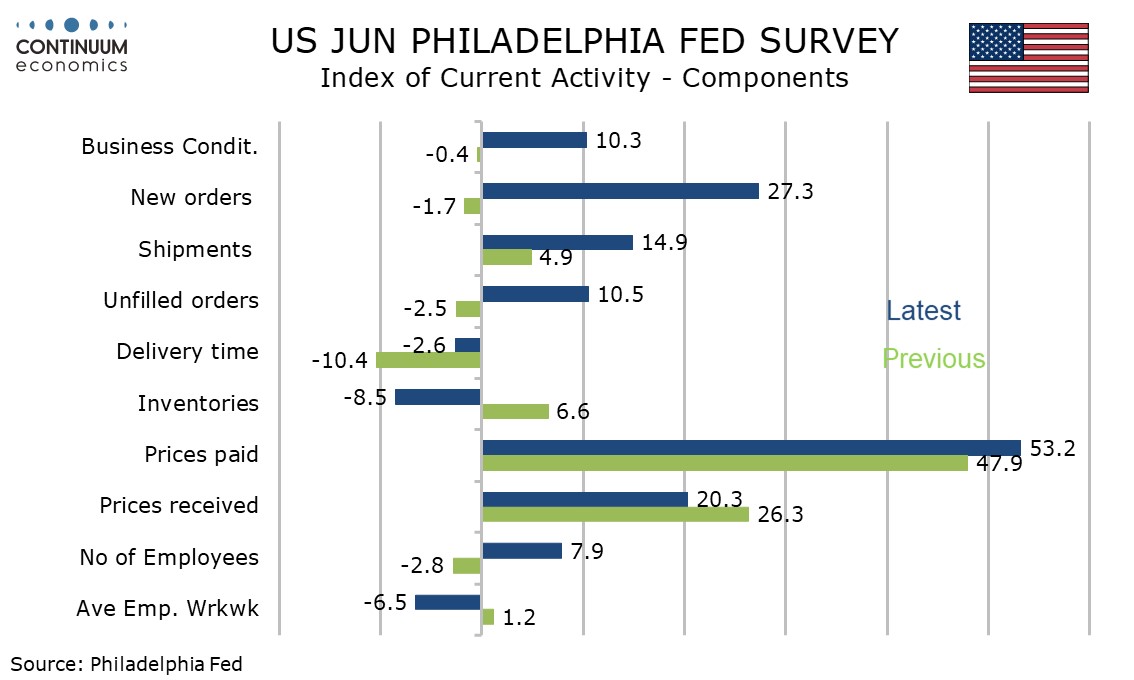

Initial claims slipped to 226k from 230k while June’s Philly Fed manufacturing survey increased to 10.3 from -0.4, both in line with expectations, improved but not as strong as some recent releases.

The initial claims data covers the survey week for June’s non-farm payroll and the 4-week average of 223.25k is the highest since December, and up from a recent low of 202.75k seen in May’s payroll survey week. This suggests June’s non-farm payroll will see some slowing from May strength.

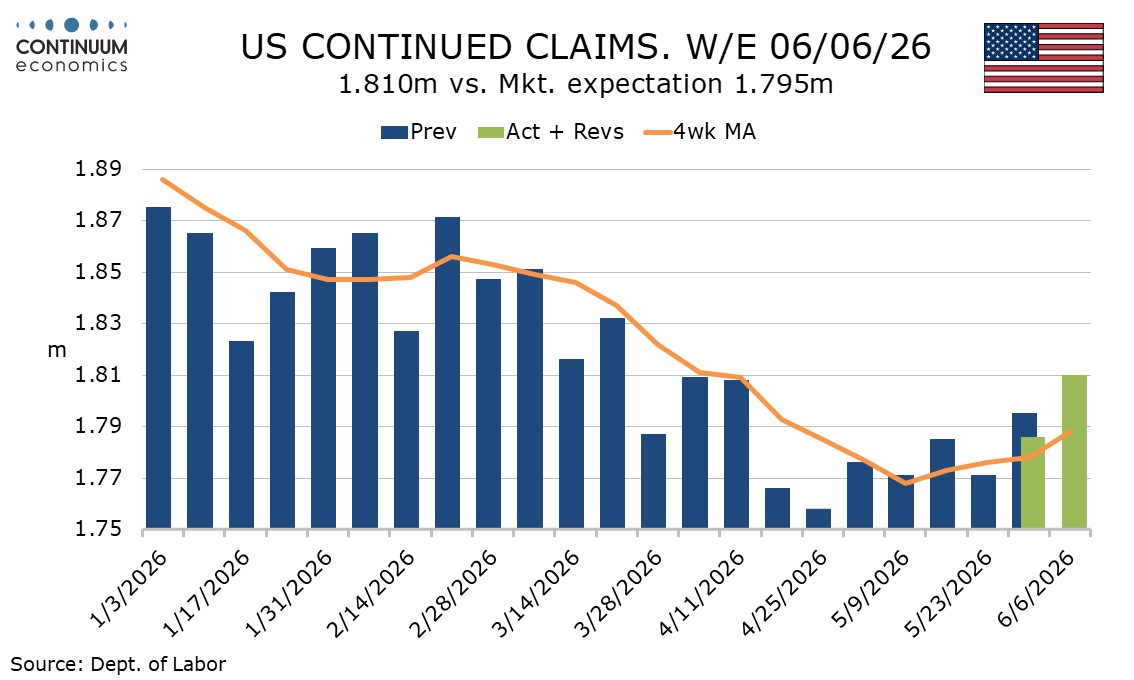

Continued claims cover the week before initial claims but have also started to move higher. On the week a rise of 24k to 1.81m was seen, to the highest level since March 28, while the 4-week average of 1.788m is at a 7-week high.

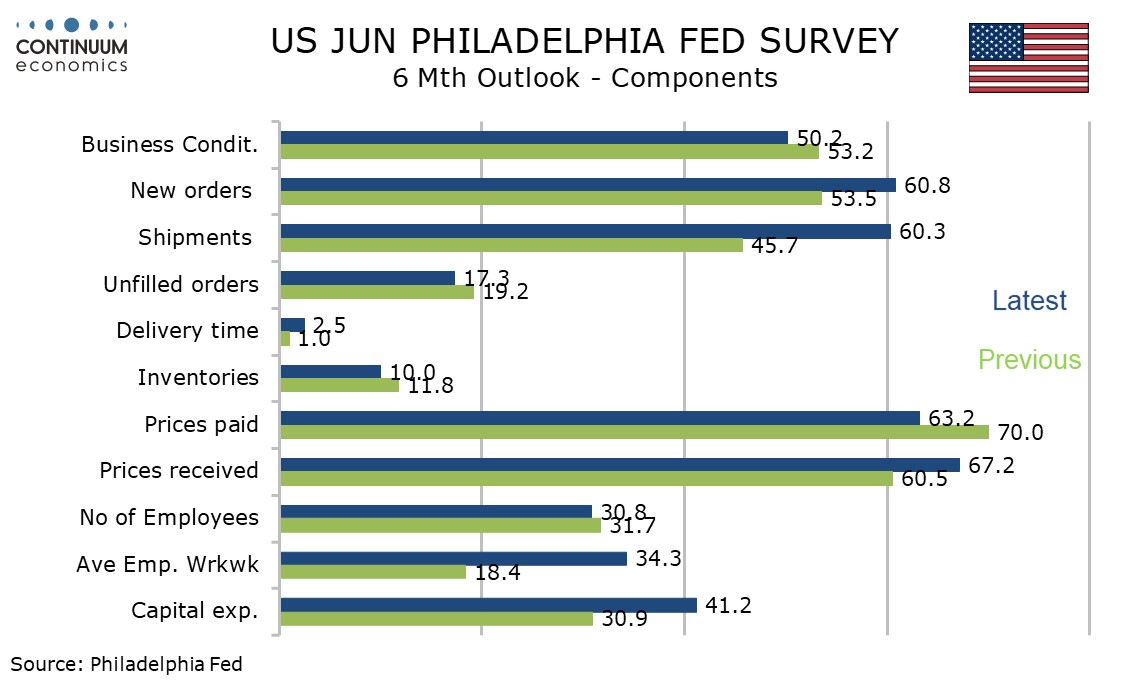

June’s Philly Fed index of 10.3 shows May’s -0.4 move below neutral was erratic, but is still down from the recent high of 26.7 seen in April, which also looks erratic. June’s index is slightly below those seen in each month of Q1.

Details are however mostly positive, with new orders at 27.3 the highest since January 2025 and 6-month expectations on activity, while down to 50.2 from 53.2, showing the first months above 50 since November 2024. Employment at 7.9 turned positive after two negatives but the workweek at -6.5 was the first negative in four months.

Price data was mixed but on balance remains firm. Current month data shows prices paid at 53.2 from 47.9, still below April’s 59.3, and prices received at a 4-month low of 20.3 from 26.3. Six month expectations show prices paid at 63.2, down from May’s 6-month high of 70.0 but prices received up to 67.2 from 60.5, reaching their highest level since August 2021, and that is worrying.