Norges Bank Preview (Jun 18): Forecast Update the Key

It may not have been a close call, but amid what were divided market expectations, the Norges Bank hiked afresh last month by 25 bp (to 4.25%), the first such move in two years. Admittedly, it had given a clear pointer in March of at least one rate hike probable in subsequent next couple of months (Figure 1), implying a good chance that a further such hike will occur is on the cards. Notably, rather than this month, markets are not pricing in such a move until around the November 5 Board verdict. By then, we assume some degree of clarity regarding the timing and size of any fall back in energy prices will be available and consistent with no need for further tightening. But in spite of what have actually been far from unfriendly CPI data and a slowing in growth that points to a clear undershooting of Board GDP expectations, the looming updated Monetary Policy Report may even be explicit in suggesting a hike late this summer. This is even if that means a nominal policy rate twice the Norges Bank’s estimate of neutral.

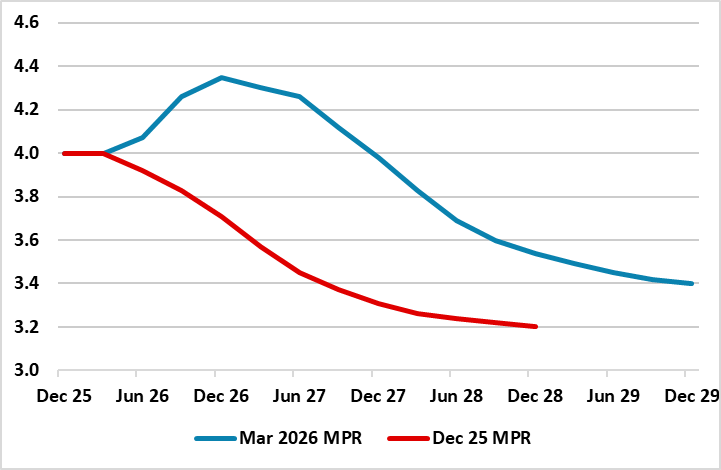

Figure 1: Norges Bank Policy Outlook Suggests Short-Lived Hikes

Source: Norges Bank Monetary Policy Report

We think that the inflation persistence arguments, that actually prevented faster easing before the Middle East conflict broke out, are overdone and that even with no hike at all, the current Norges Bank policy stance is very restrictive – even on its own assessment with the current policy rate is 1.5 ppt-plus above neutral despite (at worse) a mixed inflation backdrop.

While no change in policy is expected from the Norges Bank’s verdict this month, it is likely to repeat, if not harden, its hiking bias which currently asserts ‘the policy rate will likely be raised at one of the forthcoming meetings’. Its March forecast implied that this would entail one or two 25 bp hikes but that these will be short-lived with the policy rate coming down afresh from early next year (Figure 1). Given the lags in such policy moves taking effect, this questions the need for such a temporary measure other than to underscore hawkish reputation. As a result, we feel the Board is being excessively hawkish and not just on account of the stronger currency seen of late.

Moreover, as suggested above, we question the extent to which the inflation upgrades made by the Bank last March are realistic with the Board CPI-ATE now seen averaging 3.3% this year and 2.8% next, some 0.6 ppt and 0.4 ppt higher than envisaged three months ago. Some of the upgrade to this year is due to the apparent fact that CPI data have been higher than expected, but is this an indictment of the Board’s forecasting as despite its assertions to the contrary underlying inflation has been reasonably well behaved.

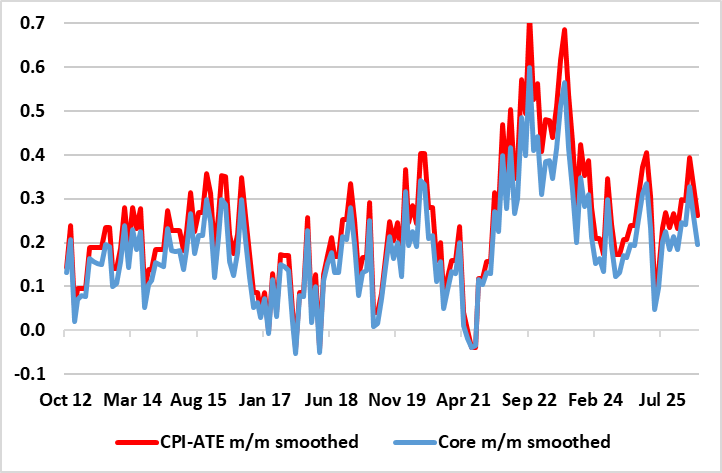

Figure 2: Underlying CPI Inflation Actually Well Behaved

Source: Stats Norway and CE – Core is ex food and energy, 3-mth % chg m/m, seas adj

Indeed, underlying inflation short-term dynamics are far from unfriendly (Figure 2) especially if food is excluded from the targeted CPI-ATE measure so as make a more familiar core measure.

Given Norges Bank caution, we remain far less confident about the extent of any eventual easing, this now having been deferred into 2027. More likely, we envisage some 100 bp of cuts through next year. At 3.25%-3.5%, that would still leave the policy rate still at the end if next year well above its own estimated nominal neutral rate of just over 2%. In other words, even on below market thinking policy outlook, the Norges Bank will be merely keeping its foot on the brake, rather than pressing on the accelerator as it only sees the rate reduction we are envisaging occurring into 2029!