China: Housing Not Bottomed Yet

• We do not feel that China residential property market has bottomed, as it faces two cyclical and two structural headwinds. Cyclically outstanding inventory of complete houses remains high, while households are also suffering from low income and employment growth. Structurally population aging is already hurt long-term demand for housing, while China authorities remain reluctant to accelerate the clean up of the property sector. We see residential investment remaining adverse to GDP in 2026 around 0.75% of GDP and is one of the key reasons behind our 4.4% 2026 GDP forecast.

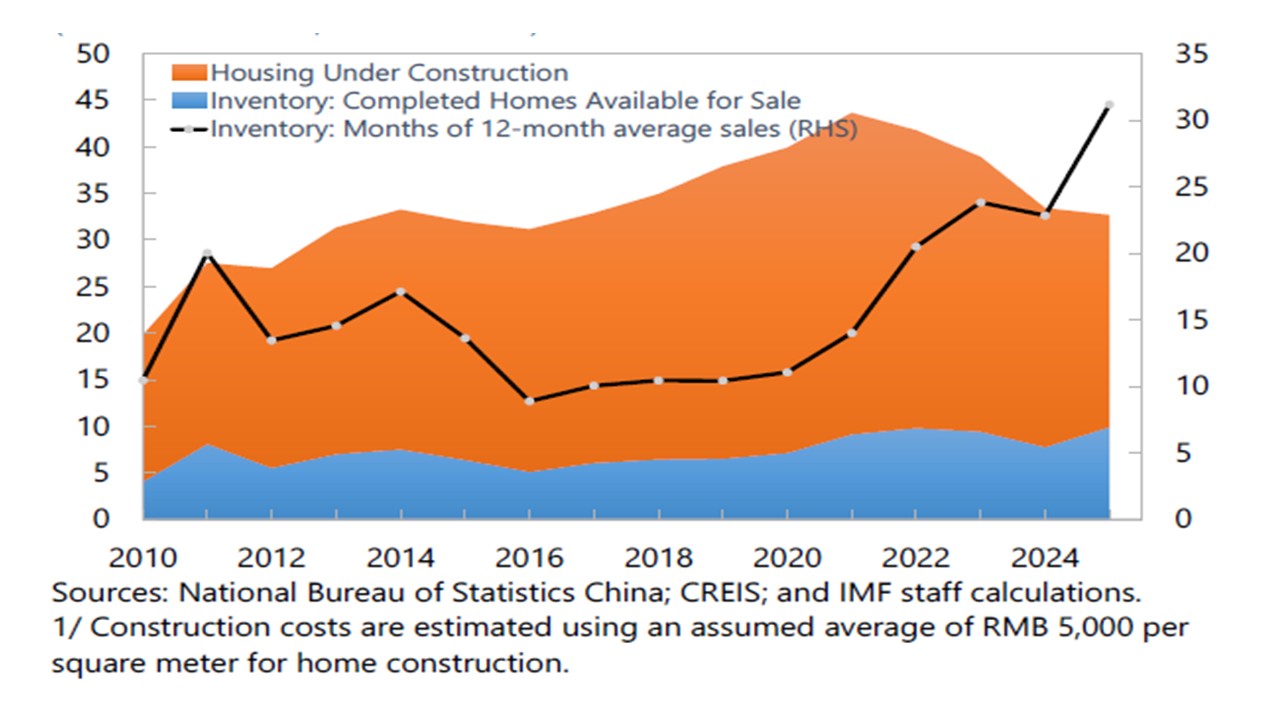

Figure 1: Housing Supply (LHS RMB Trlns end of period; RHS Months of Supply)

Source: IMF Article IV Feb 26

Source: IMF Article IV Feb 26

China authorities are of the view that the residential property market is bottoming and will become less of a headwind to the economy. Key points to note.

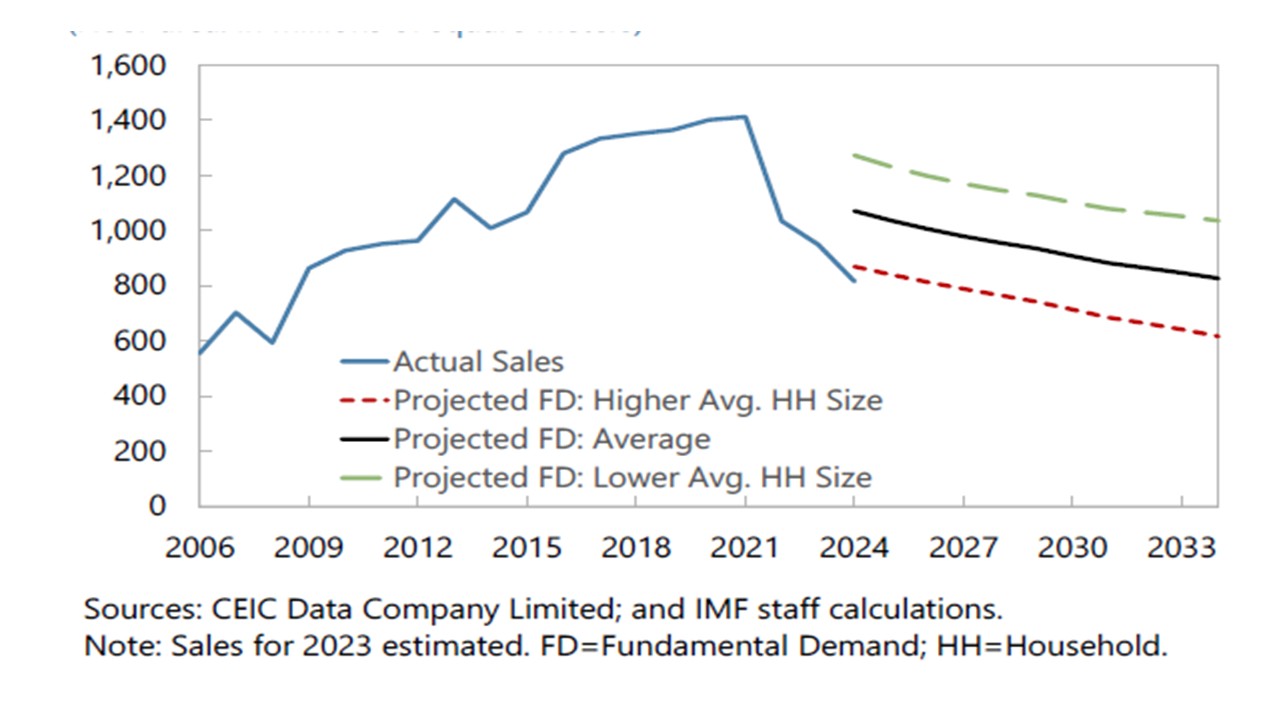

• Stabilising home sales, but inventory overhang. Home sales declines have slowed down, while property prices are falling at a slower pace than 2024. This prompted China authorities to argue that the housing market is bottoming in the latest IMF Article IV official comments. Certainly signs of stabilization in home sales are helpful, but we do not feel a bottom has yet been reached. Inventory levels of completed homes remain excessive (Figure 1), as government spending to absorb some homes for social housing has been more than counterbalanced by new homes being completed. This is the 1st cyclical problem. Additionally, China is moving to structurally lower residential property needs, as population aging already means that the proportion of 25-45yr forming households is smaller than previous generations and this is slowing long-term demand (Figure 2). Combined with inventory overhang, this suggests that downward pressure on residential property prices has not reached bottom. The combination of still lower house prices, plus the inventory overhang, means that the market is not yet reached bottom and home sales can remain fragile and not show a meaningful rebound in 2026. Indeed, our baseline remains for residential property investment to knock around 0.75% off 2026 GDP growth, though this would be less adverse than 2024 or 2025.

Figure 2: Residential Real Estate Sales and Projected Fundamental Demand (Floor area Mlns SQM)

Source: IMF Article IV Feb 26

Source: IMF Article IV Feb 26

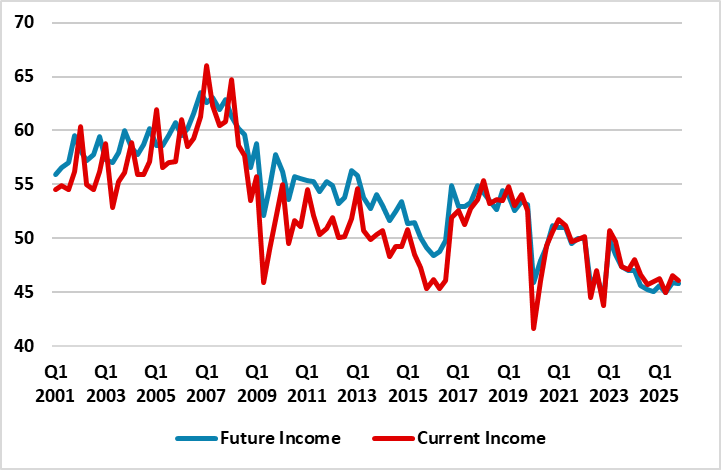

• 2nd cyclical problem: Weak Consumer. China consumption growth is modest, as household confidence surveys shows constraints from wage and employment growth (Figure 3). Private sector wages that averaged 8% per annum pre COVID have slowed dramatically to around 3%, which means that households are less willing to buy at high house price to income ratios as wage growth will no longer quickly relieve being overextended initially. Additionally, private sector employment growth has slowed, both alongside the economy and given the less pro-business stance post COVID under President XI. Some households have been repaying debt, which has meant that net household lending is now close to zero, which only occurs in recession or balance sheet constrained economies.

Figure 3: China Current and Future Income Expectations (Index) Source: Datastream/Continuum Economics

Source: Datastream/Continuum Economics

• Authorities reluctant to accelerate property reset. China authorities have been providing fiscal expenditure to help reduce the overhang of complete housing, but also to finish incomplete houses that is adding to inventories. Lower deposit requirement, monetary easing and encouragement for banks to lend are also elements of the support package for the sector. Even so, China authorities are reluctant to have a more aggressive clean up that would produce a bottom to the property market, with the official view disagreeing with IMF recommendation that 0.9% of GDP should be spent in 2026 on a property clean up. Part of this reflects a bias against old economy areas such as residential property investment, but also official restraint on fiscal policy given the general government debt/GDP ratio – the IMF forecast this will rise from 102% in 2026 to 116% in 2030.