Sweden Riksbank Preview: Mild Tightening Bias Persist but We Don’t See it Exercised?

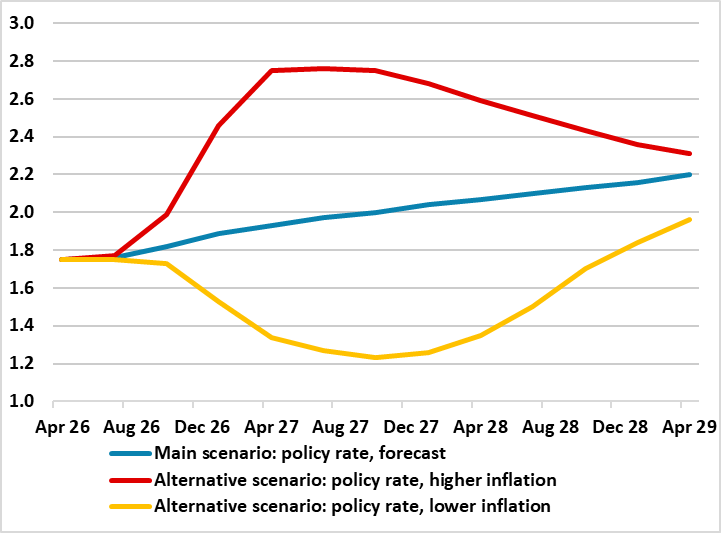

Not only at the meeting this, we still see stable policy though to end-2027 rather than the small hikes markets and the Board are now pricing for late 2026. A similar profile has been offered by the Riksbank since last autumn (Figure 1) and it did bring forward its first hike hint a touch when it presented its updated Monetary policy report alongside this stable verdict. Indeed, in March, it tweaked its forward guidance by suggesting that, even amid Middle East conflict making the outlook very uncertain, it was in a good initial position to adjust monetary policy if required to safeguard the inflation target and no longer pointed to no change for some time to come. Somewhat better data in the last on both the GDP and CPI fronts may even harden this guidance, but underlying inflation is still well below Riksbank thinking while its own survey data and the labour market (Figure 2) provide a timely reminder of on-going economic fragility.

Figure 1: Riksbank Policy Rate Outlook Scenarios

Source; June 2026 Riksbank Monetary Policy Report

Regardless, the Board analysis is party out if date, not encompassing the recent Iran ceasefire deal and the ensuing marked drop in energy prices. Even so, the update suggests that CPI inflation in Sweden is still low, largely due to the dampening effects of fiscal policy measures. Economic activity is somewhat weaker than normal and growth was lower than expected in the first quarter. Moreover, the recovery in the labour market is tentative. However, the supply disruptions caused by the war in the Middle East are dampening economic developments somewhat, but, in the forecast, growth is expected to be higher this year than last year and economic activity will strengthen.

The Executive Board therefore decided to leave the policy rate unchanged at 1.75 per cent. Underlying inflation is low and economic activity is somewhat weaker than normal, but at the same time the supply disruptions have led to a rise in inflationary pressures and increased the risks of inflation being too high – not sure about this! Against this backdrop, the Executive Board has raised the policy-rate forecast somewhat, but assesses that it is well-balanced to leave the policy rate unchanged at present. The forecast means that the probability of the rate being raised later this year has increased compared to the assessment in March.

But there is considerable uncertainty and the developments call for vigilance. In addition to the war in the Middle East, there are also other risks that could affect the outlook for inflation and economic activity. There is also a possibility that the effects of the war will interact with other more underlying vulnerabilities in the global economy, such as high equity valuations and unsustainably high public indebtedness. The range of potential outcomes for what can happen going forward is wide and the Riksbank is highly prepared to adjust monetary policy, presumably this implies a move in either direction ultimately. But a clear but modest hiking bias remains even on a more benign inflation, albeit as for the later any such hikes would follow clear further easing.