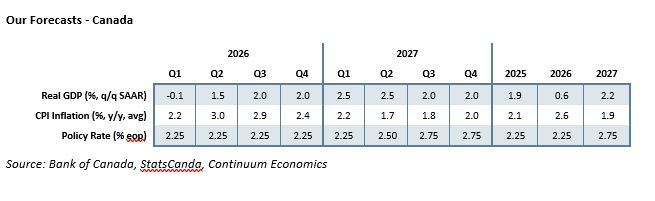

Bank of Canada - On hold with balanced tone

While recognizing that oil is around $10 per barrel higher than was assumed in its April Monetary Policy Report, the Bank of Canada left rates unchanged at 2.25% with a balanced tone to the statement. As long as core inflation does not start showing feed through from energy the BoC looks likely to avoid tightening until excess supply in the economy is reduced. We do not expect tightening until 2027.

After April’s meeting Governor Tiff Macklem stated that if the economy evolved in line with expectations policy close to current settings would be appropriate, but noted that policy might have to be nimble, noting the risk of consecutive tightenings on persistent inflation and easing if the US imposed significant new tariffs. While energy prices are now stronger than anticipated in April, Q1 GDP was weaker than expected at -0.1% annualized, which the BoC attributed to an unexpected decline in government spending, while April CPI at 2.8% was on the soft side of an April projection of about 3.0%. On inflation the BoC added that there has been little evidence of a broad based pass through of energy prices, with core CPI falling to around the 2% target and the share of components above 3.0% close to the historical average. CPI is now expected to hover around 3% in the near term before easing gradually to around the 2% target. On GDP the BoC expects growth to resume in Q2 but excess supply to persist. A strong May employment report was downplayed, with employment volatile and little changed since the start of the year. Senior Deputy Governor Carolyn Rogers stated that risks to the economy were about the same as where they were in April.

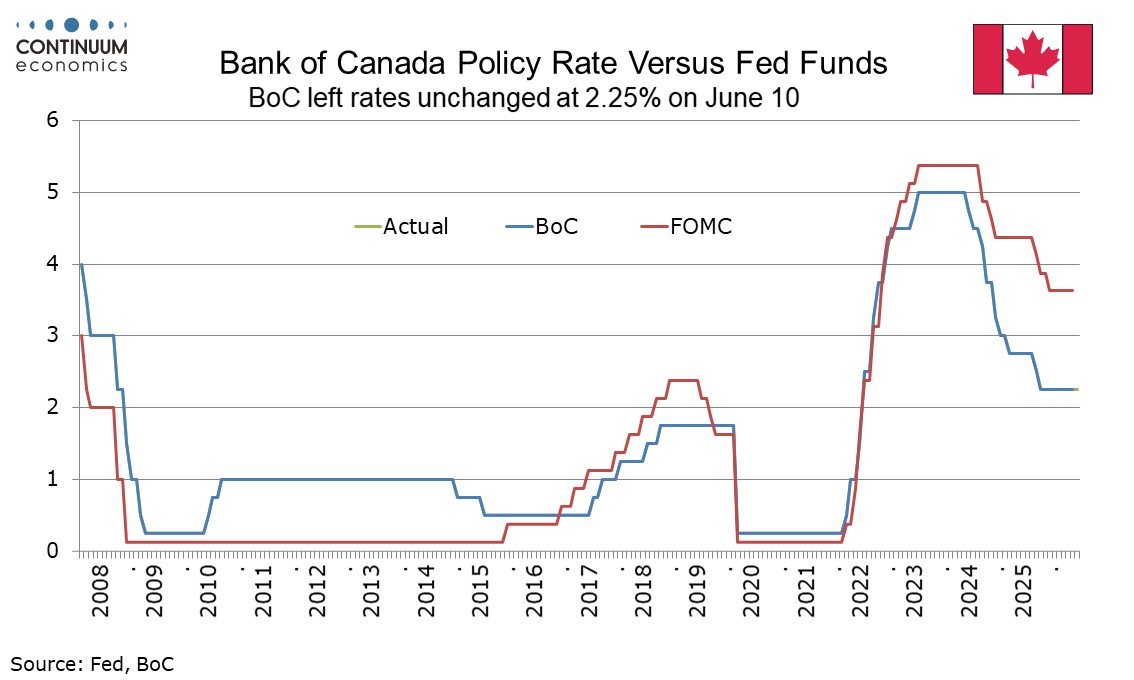

Macklem now sees leaving rates unchanged as balancing the risks of slowing the economy by tightening and lifting inflation by easing, though the possibility of consecutive tightenings on energy feed through or easing on fresh tariffs was reiterated. The latter risk could materialize quite quickly with USMCA negotiations due in July though Macklem's base case is that they continue for a number of months. The statement noted that the US administration continues to propose fresh tariffs. The BoC appears some way off tightening in response to energy risks, with Macklem’s conditions for that being the if conflict in the Middle East continues and higher energy prices start leading to ongoing generalized inflation. Our central assumption is for the Strait of Hormuz to reopen in the summer, and while there is significant uncertainty on that, excess slack is likely to keep underlying inflationary pressures subdued. We do not except the BoC to change rates until Q2 2027, by when the economy is likely to be growing above potential with core inflation remaining near target and the overall pace below target on an energy unwind. Thus policy is likely to be determined by activity rather than inflation as long as core inflation remains contained. We are assuming the BoC will not have fresh US tariffs to respond to, but uncertainty is high there too. 50bps of tightening in 2027 would return rates to the midpoint of the BoC’s neutral range of 2.25%-3.25%.

Macklem now sees leaving rates unchanged as balancing the risks of slowing the economy by tightening and lifting inflation by easing, though the possibility of consecutive tightenings on energy feed through or easing on fresh tariffs was reiterated. The latter risk could materialize quite quickly with USMCA negotiations due in July though Macklem's base case is that they continue for a number of months. The statement noted that the US administration continues to propose fresh tariffs. The BoC appears some way off tightening in response to energy risks, with Macklem’s conditions for that being the if conflict in the Middle East continues and higher energy prices start leading to ongoing generalized inflation. Our central assumption is for the Strait of Hormuz to reopen in the summer, and while there is significant uncertainty on that, excess slack is likely to keep underlying inflationary pressures subdued. We do not except the BoC to change rates until Q2 2027, by when the economy is likely to be growing above potential with core inflation remaining near target and the overall pace below target on an energy unwind. Thus policy is likely to be determined by activity rather than inflation as long as core inflation remains contained. We are assuming the BoC will not have fresh US tariffs to respond to, but uncertainty is high there too. 50bps of tightening in 2027 would return rates to the midpoint of the BoC’s neutral range of 2.25%-3.25%.