FX Weekly Strategy: APAC, Jun 1st-5th

Focus on MoU, dollar to slip if deal signed, though long-term outlook less clear cut

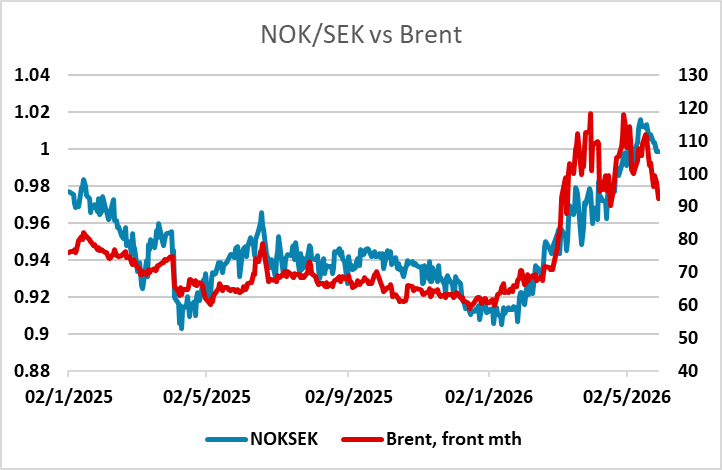

Oil crosses such as NOK/SEK also potential to key off sustained pullback

Payrolls and ISM the key data out of the US, to show ongoing resilience

Outside of Iran, a large list of political tail risk events across the rest of the year to consider

Stop me if you’ve heard this one before… The week ahead very much dominated by the subject of a Trump signature. Very little getting away from the fact that this will direct the price action for the next few weeks, even if it isn’t necessarily the end of the story.

A betting person would punt that the odds favour an MoU of sorts getting across the line, but that the nuclear issue might not be entirely nailed down and the opening of the Strait might not go entirely gracefully either. That reflects the realities of Trump needing to be able to at least spin the outcome to conservatives (and to himself).

On the subject of punts, for what its worth, Polymarket as of writing had the next extension/deal announcement at 42% for June 3, 60% for 7th and 78% for 30th. It also had a permanent deal as 56% by July 31, and 78% by Dec 31. Probably as reasonable as anything else.

Such a scenario would be a clear huge relief in the immediate term, but still leave open the risk of skirmish scares on the re-opening and, more importantly, remaining baggage on the nuclear material details that could still need a lot of work to clear for a final agreement.

What the FX reaction to that is maybe not as trivial a question as it might seem. Initial fading of the ‘haven dollar’ factor and some central bank pricing adjustment (assuming less pressure on the Fed to move into line, while the ECB might show more inertia in still hiking?) seems a reasonable story. If EUR/USD closed about 1.1650/60 then it could well run for the range upside (1.17-18). Likewise, USD/JPY can see some relief on the upside pressure as far as the MoF are concerned and next support is 159.00 and then the 158.60~ weekly low of 20 May.

Further out, the economic divergence story though doesn’t entirely go away though, nor does the potential for other ambiguous political risks, so this leaves a more nuanced story for the dollar in coming quarters than might be hoped.

On the subject of that relative resilience, we do expect that to be broadly on show again this week with a not-unhealthy 90k for payrolls and strong ISM data (more details below). The dollar might not smile as of old but there’s still the possibility of a bit of a smirk or is it a sneer.

We recently discussed the cross trades that might see the most corrections too. AUD/NZD has already pulled back in some style with the RBNZ trigger and after the noted spec cross positioning extreme, getting back to circa 1.2. 1.1927~ weekly lows would be the next line back on further kiwi recovery.

NOK/SEK hasn’t been as lively but as another clean oil trade and a good run this year, albeit from cheap levels, it might also see further correction in the event of a deal announcement (pullback low of 0.991~ so far, around 23% back, with 0.98 and 38% back if it too can extend).

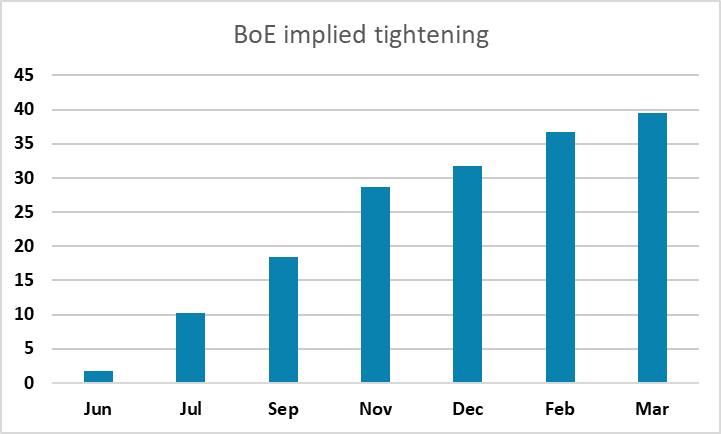

Comments from the BoE Bailey last week continue to present the BoE as the anti-ECB meanwhile, seeing risk-reward skewed to leaving policy on hold despite short-term inflation overshoot so long as not seeing second round effects. The MPC is split on this, but Bailey’s view is prevailing. Market pricing has moved this way, but we could see odds of a hike further diluted from July and maybe even out to Sep if the data keeps coming in sluggish and the Iran shock shows signs of thawing. In terms of FX though, there’s little sign that the market has shifted out of its well-established swing pattern within a range and EUR/GBP looks likely to continue to play a range and reverse strategy until and unless a breakout it seen. Politics is on the backburner until nearer the Makerfield byelection, and the retreat in yields has also stemmed the pressure.

Given how dominated the week ahead is by a binary event, it might be worth stepping back from the immediate, and taking stock of global political risks that sit the other side of summer and that stand outside of the critical Iran war and blockade sphere.

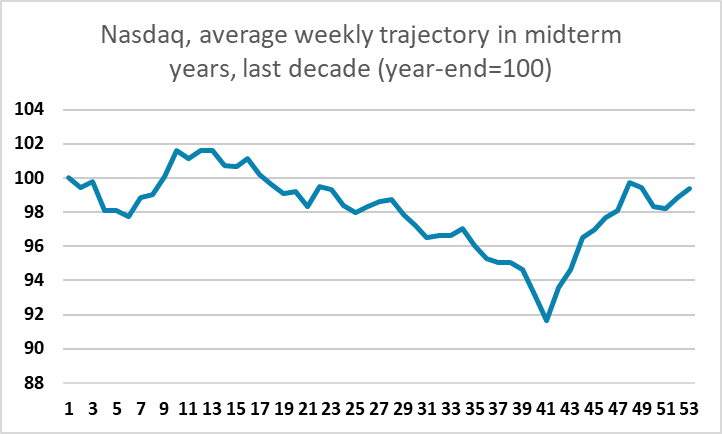

We discussed elsewhere how US midterms present a very high risk of incident, in terms of either interference or contestation of the results. The historic tendency anyway to see notable peak-to-trough equity drawdowns at some point during midterm years is well-documented and a useful contextual backdrop to the unique dangers on show this time around, even if the current equity market is far from normal. For the dollar, the question would be how any effects on risk markets, if seen, and dollar-trust-status net out if this scenario unfolds later in the year. One plays to renewed haven, the other to the structural dollar bear call (the ‘ignore politics and buy AI again’ to neither).

In Canada, the Alberta referendum question on Oct 19 is its tail risk. Current voting intentions are 60% against and 67% against in any eventual binding referendum. But Brexit showed that it’s risky to be asking questions you don’t want the wrong answer to.

Finally, Switzerland has a slightly less dramatic but still possibly problematic vote more imminently on June 14 to cap the population at 10mn, with associated trigger mechanisms of exiting its EU free movement trade agreement, as well as labour access implications. Polls have been narrowly divided only marginally against so a surprise yes is well within statistical error margins even now and could cause CHF volatility.

Data and events for the week ahead

USA

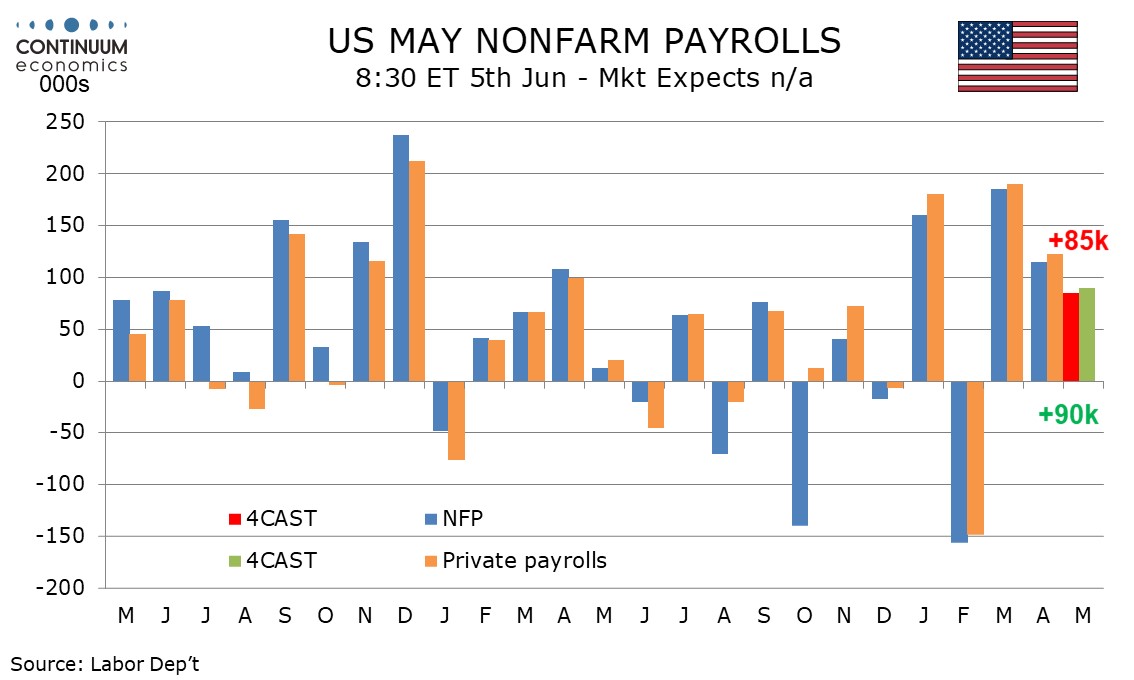

The data highlight from the US will be Friday’s non-farm payroll for May. We expect a rise of 85k, 90k in the private sector, slower than in March and April but still healthy, leaving unemployment unchanged at 4.3%. We expect a 0.3% increase in average hourly earnings after two straight subdued gains of 0.2%.

Other labor market signals come from Tuesday’s JOLTS report on labor turnover, and Wednesday’s ADP report on private sector employment for May, where we expect a rise of 100k. Thursday sees weekly jobless claims and revised Q1 productivity and costs.

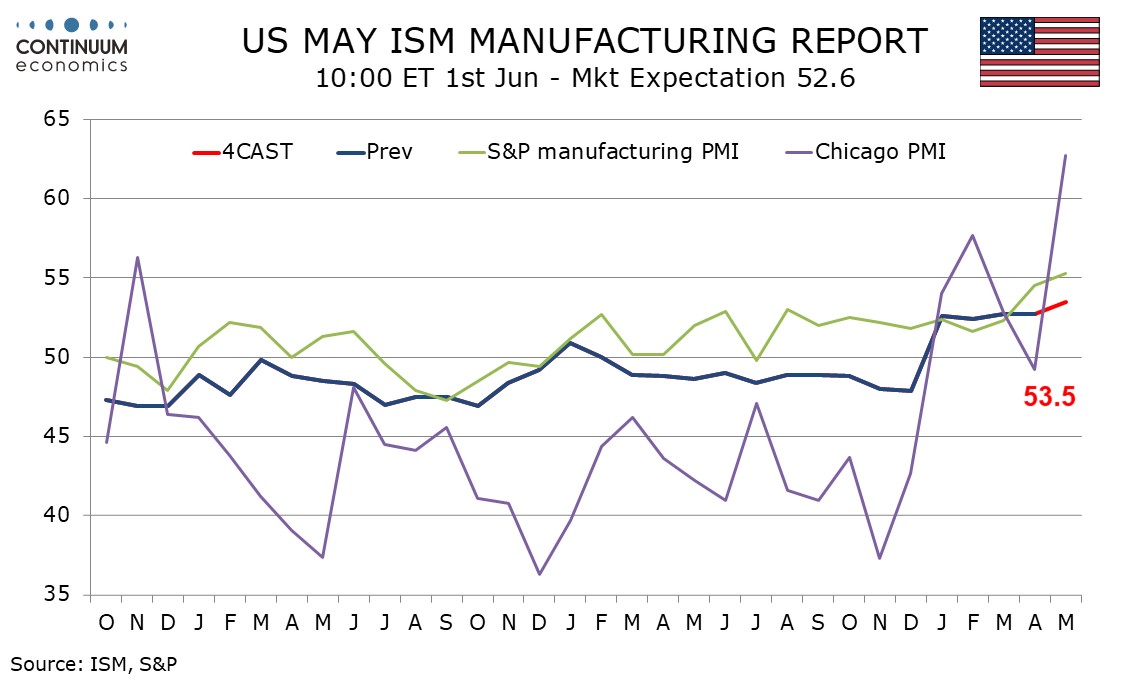

We expect stronger ISM indices for May, manufacturing on Monday at 53.5 from 52.7, and services on Wednesday at 54.5 from 53.6. The tail end of April data sees construction spending on Monday, factory orders on Wednesday and consumer credit on Friday. Fed speakers include Kashkari and Hammack on Tuesday, and Daly on Thursday.

CANADA

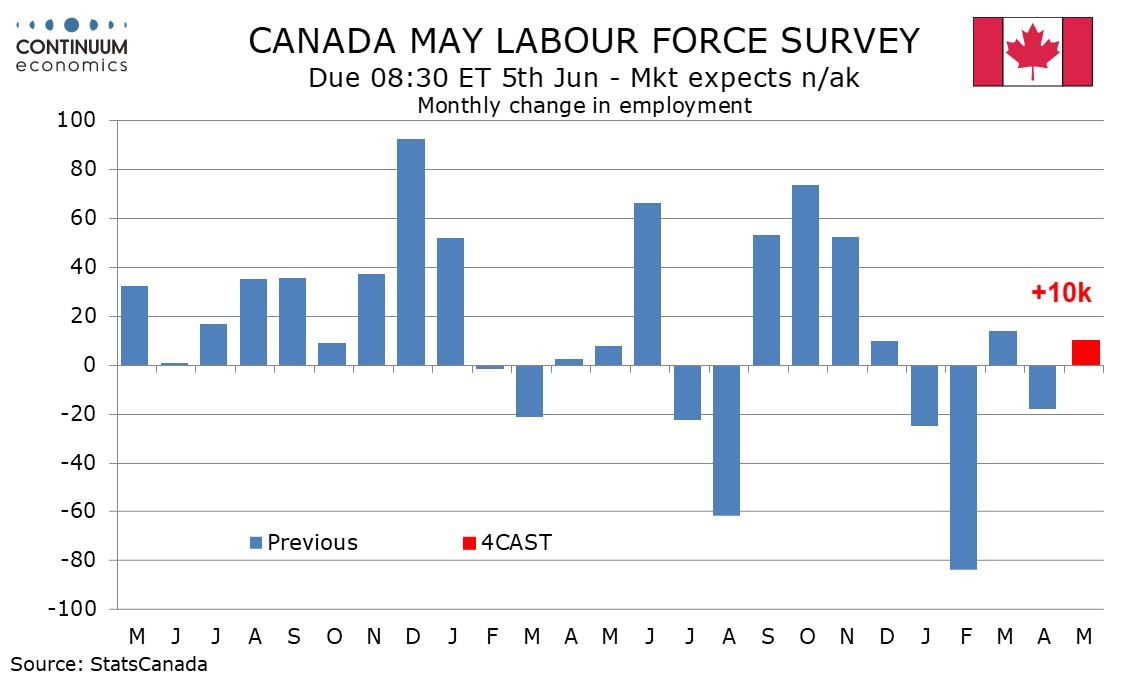

Canada’s most significant release will be May employment on Friday, where we expect a subdued 10k increase with unemployment unchanged at 6.9%. Q1 productivity is due on Wednesday. May PMI indices are seen from S and P for manufacturing on Monday and services on Wednesday, with the Ivey manufacturing PMI following on Friday.

UK

Coming before final PMI data (Mon & Wed), Thursday sees construction PMI data as well, this likely to be flashing clear warning signals. Otherwise, the BoE dominates the week with Tuesday’s money/credit data likely to show more signs of a softer housing market, thereby chiming with anecdotal evidence. Such signs may get short shrift from MPC hawk Greene who speaks (Tue) but may feature in updated BoE survey data (Thu) via the latest Decision Maker’s Panel.

Eurozone

Data wise, there are final manufacturing and services PMI numbers (Mon/Wed) and then the construction counterpart (Thu). Retail sales (Thu) and PPI data (Wed) will attract little attention. Otherwise, the week is dominated by Monday’s actual money and credit figures, where some credit weakness is emerging, these coming almost alongside labour market data which still suggest abundant workforce supply. But the main event will be the May HICP flash. While somewhat important, these data are unlikely to have a material impact on ECB thinking, irrespective of whichever way it may surprise. Most likely the data will show a further and still largely energy driven rise of 0.4 ppt, matching the April gain, but now to a 32-mth high of 3.4%. This could involve small rise in the core too, albeit mainly aberrant seasonals pulling up services, but where the resultant core of 2.4% (0.2 ppt up) would mean a double-whammy in that both it and the headline would be above existing (ie March) projections. Friday sees updated Q1 employment and GDP figures, and also services output for March

Rest of Western Europe

Sweden sees flash May CPI numbers due Wednesday which will make little difference to Board thinking even if CPIF which fell to a surprise low of 0.8% in April rise back above 1%. In Switzerland Monday’s Q1 GDP should echo the flash. The latter is estimated to have grown by 0.5 % last quarter of 2026.Both the industrial and services sectors contributed to this growth. Thursday should see the CPI y/y rate up to around 0.8%