FX Daily Strategy: Asia, Jul 14

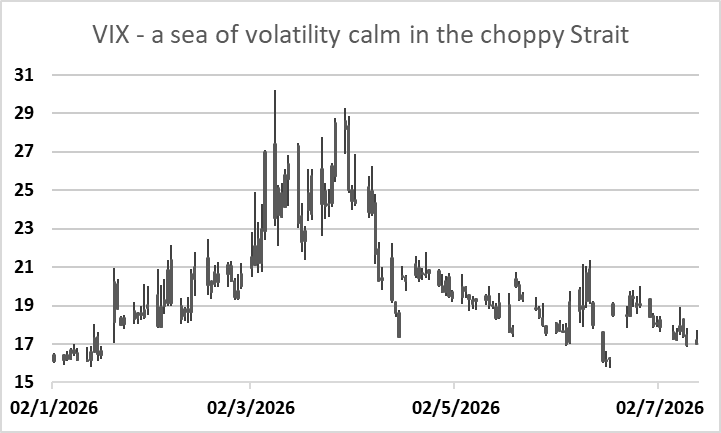

Market summer-lulled, too relaxed, or ice-cool worldly - time will tell; arm-wrestle can't go on forever without consequences

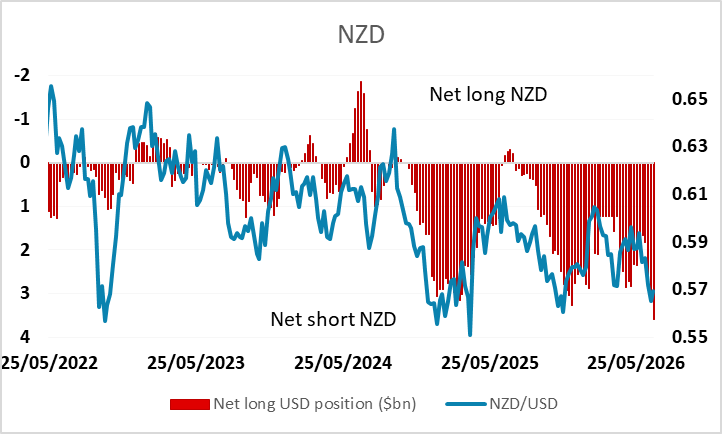

Short and caught kiwi still a bright spot

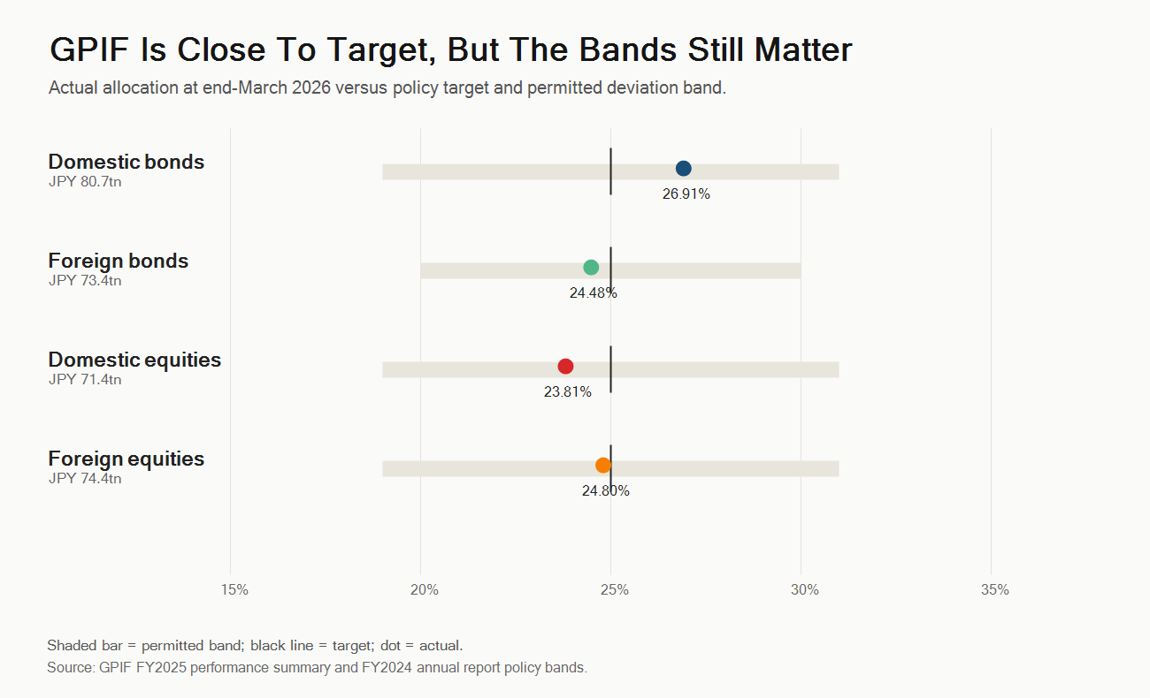

Japan GPIF story also slumbers but one to watch

Main focus for the week arrives with US CPI and Warsh testimony

Traction is proving hard to come by at present, as the summer heatwave (and World Cup) goes on. Whether that is prescience or drifting complacency in markets given the renewed chastening impact of military exchanges on Strait traffic flow (at much tighter remaining reserves in refined than crude) is to be seen. It’s still a controlled arm-wrestle but not without big consequence if it rolls on and on.

Outside of Iran, even the Japan GPIF story as failed to really spark the market much either, at least at present, USD/JPY back on the 162 handle yet again. The theme is not without its implications, direct and indirect (discussed here), but may prove to be a slow burner if it is to gain more market prominence.

Honouree mention does still go to the kiwi, where the spec data actually showed the market doubling down even more extreme NZD short into the RBNZ hike and squeeze. AUD/NZD is at a key area now, the 1.1985/78 end May lows so if that doesn’t hold then there is some further range extension down to 1.1930/00 at least.

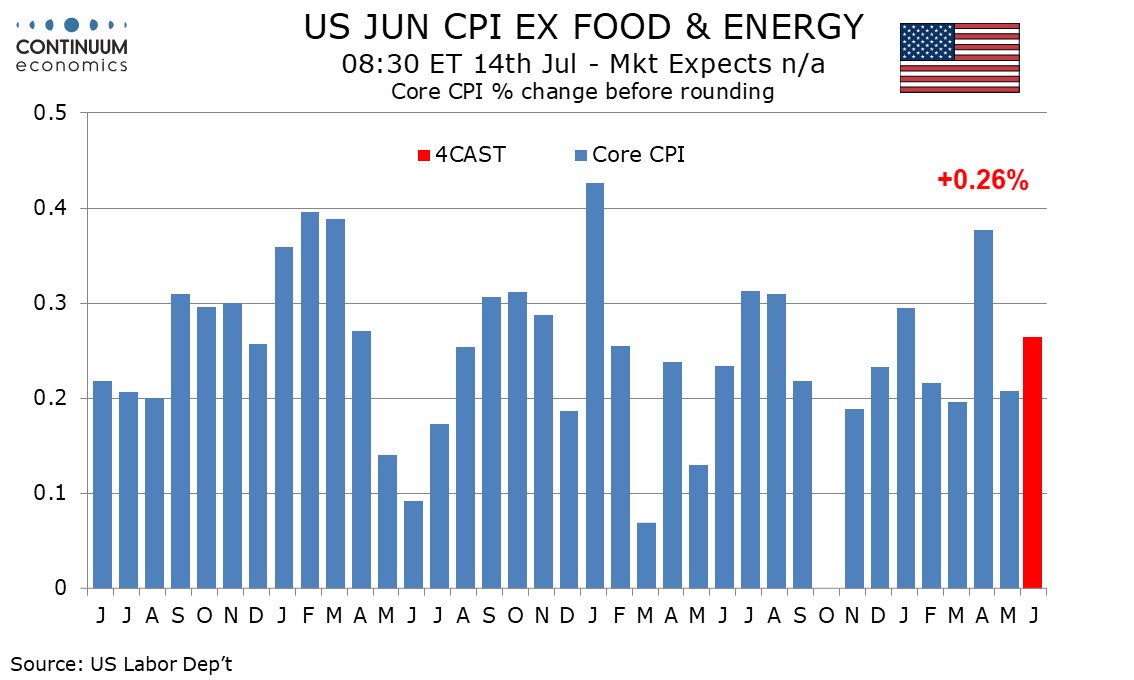

Meanwhile, what is otherwise quite a slow week sees its main calendar focal points on Tuesday, with the US CPI data, followed closely by testimony from Fed Chair Kevin Warsh to the House Financial Services Committee due 90 minutes later.

In terms of CPI, we are broadly in line with market in looking for unchanged overall, but with a slightly firmer 0.3% rise ex food and energy, 0.26% before rounding. It is hard to ignore the overarching Iran context even here though as that number can be read very differently in the midst on an ongoing supply chain constriction than it can in an environment of full return to supply chain normality.

Warsh may well want to continue to stick to the message of no forward guidance but it may well still surface headlines of note.

As thing stand going into it, Fed funds future have 25bp fully priced in by September/October and 50bp mostly priced in by March/April.

Interesting from both will not just be the results but the impact or lack of. Spec data has been implying a market that is already broadly quite long dollar already (outside of the euro) and that does seem to be one of the factors (alongside spill over to everyone’s monetary policy reaction functions), that is tending to keep dollar haven blips relatively limited and short-lived at present, at least while volatility is still pretty stable and low.

EUR/USD in particular has found it harder of late to sustain looks below rather than above the tight 1.14~ pivot, with 1.1350~ support yet to really be challenged. 1.1450/1.1473 congestion and recent high is still the limit of ambition on bounces too though.