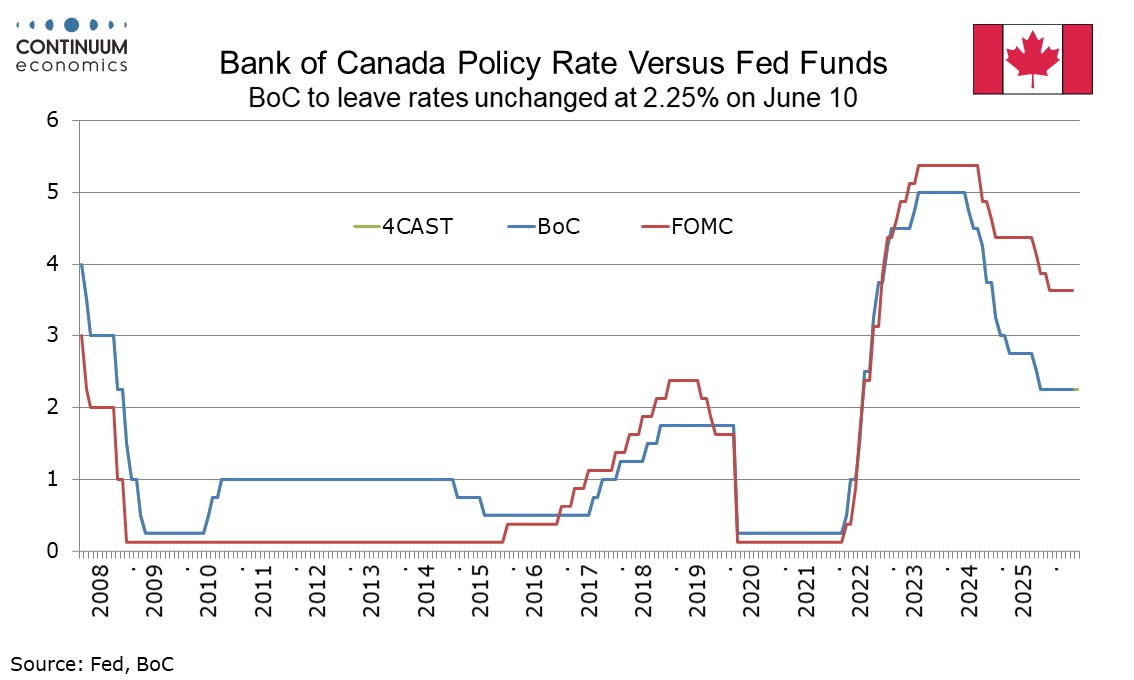

Bank of Canada Preview for June 10: A little less hawkish despite continued energy risk

The Bank of Canada meets on June 10 and looks set to leave rates unchanged at 2.25%. This meeting will contain no quarterly Monetary Policy Report and hence no updated forecasts. However, since the last meeting on April 29 GDP and core inflation have come in softer than expected, but elevated energy prices look likely to be more persistent than the BoC assumed in April. On balance we expect a slightly less hawkish tone, which could reduce the perceived risk of a tightening later this year.

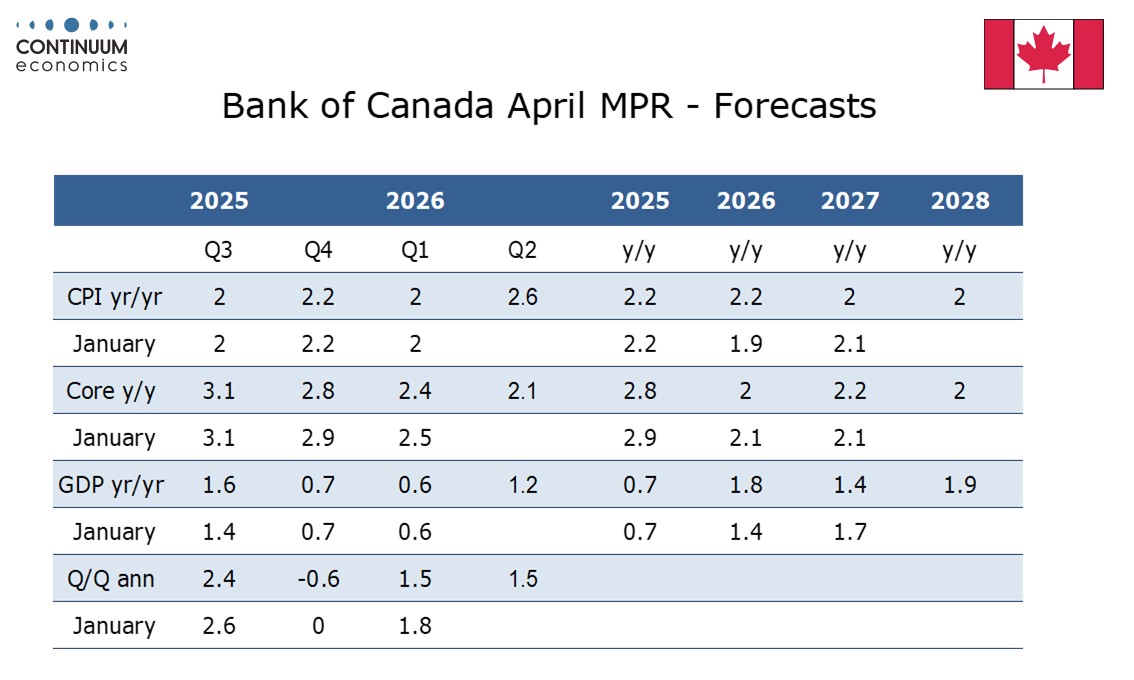

On April 29 the Bank of Canada agreed to look through the immediate impact of the war in the Middle East on inflation. Governor Tiff Macklem however stated that they are committed to not allowing persistent inflation to develop and if that happened there may need to be consecutive increases in the policy rate. The BoC assumed oil prices declining to around $75 by the middle of next year with CPI peaking around 3.0% in April and easing back to the 2.0% target by the middle of next year. The BoC stated that if the economy evolves in line with its forecasts, policy changes are likely to be small. Minutes from the meeting however showed that if oil prices were to remain elevated for a prolonged period the risk of broader and more persistent inflation would increase.

April CPI at 2.8% yr/yr was softer than expected due to very soft core inflation, with the CPI-Median and CPI-Trim rates moving close to the 2.0% target, and CPI ex food and energy, not targeted by the BoC, even softer at 1.5%. However Q2 CPI looks set to be stronger than a 2.6% BoC forecast made in April, with 3.0% looking more likely, meaning that the BoC’s worries about oil will have increased. However, the BoC will need to balance this against recent soft core CPI data, which on the trend seen in the last few months looks set to move below target by the second half of this year. A downside surprise on Q1 GDP, falling by 0.1% annualized after a 1.0% decline in Q4. BoC Senior Deputy Governor Carolyn Rogers downplayed the significance of this signaling a technical recession, and early signals are that Q2 will see a return to growth. However the weakness of recent activity and core CPI data probably outweighs the persistence of elevated energy prices.

While the BoC in April pointed to oil prices as a risk that could necessitate tightening, Macklem also stated that if the US imposes significant new trade restrictions, the BoC may need to ease policy. In April the energy risks got more attention than the tariff risks, but with a review of the USMCA trade agreement due in July the trade risk may get increased attention this time. Trump has already included Canada among those countries not seen as taking sufficient action against imported goods made from slave labor, which has become a potential excuse for tariffs after the US Supreme Court ruled against some of the 2025 tariffs. The BoC will keep its options open on policy, and energy-led inflation remains a concern for the BoC, but it may be seen as less likely to force a tightening this year than previously after this meeting. We expect the BoC to remain on hold this year, before two 25bps tightenings in 2027 return rates to the midpoint of the BoC’s neutral range of 2.25-3.25%.