FX Daily Strategy: APAC, Jun 16th

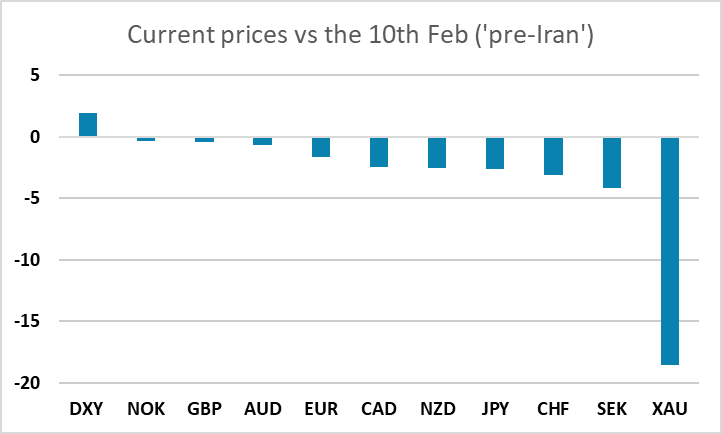

Since Iran kicked off, gold holds on to the biggest remaining losses, SEK next

BoJ in focus, 25bp hike universally expected, attention on statement and bond program

RBA tone also to be scrutinised.

Broader dollar tone still waiting on the new era Fed

Before turning to the next round of key events, it is worth briefly taking stock of where current prices sit, relative to the pre-Iran levels, to give some basis of comparison if we assume the benign scenario plays out from here (see here for the latest risk scenario odds and implications).

Gold remains the biggest net changer, still down just under 20%, but it has been bouncing. It would need to be back above 4450, so another 100pts, to be regaining the broken 200dma. This is a market where mood had turned extremely bearish having previously been super bullish, so it is prone to contrary sentiment excesses.

Otherwise, it’s SEK as high beta counter that is still down the most on mid Feb, and this is where the most major FX reactiveness has been seen so far as a result, at least as long as broader risk trade is able to sustain its recover as well (i.e. the tech risk bounce holds rather than running into more distribution).

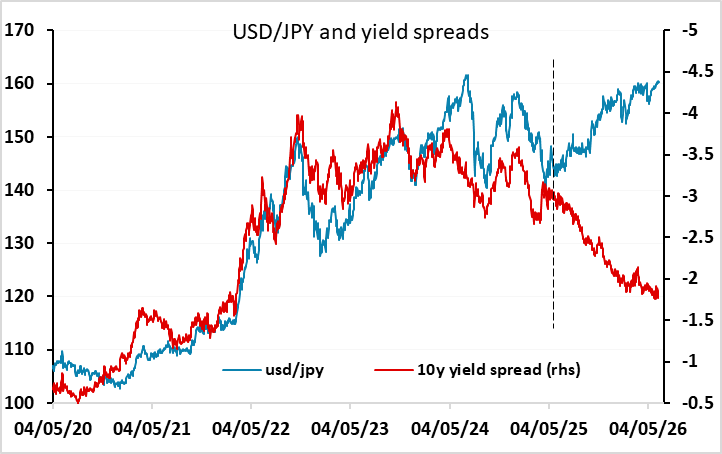

As to whether the yen also has a little room to reset and give up the 160 handle, that is where the focus does shift to the key central bank meetings, kicking off with BoJ.

A 25bp hike is a given, but focus will be on the tone and forward guidance as well as on the bond program. We believe it is possible the BoJ could temporarily pause their tapering at the end of current plans, 2.1 trillion JPY by Q1 2027. Given how USD/JPY has diverged from yield spreads, the key factor will be credibility and whether the Bank’s actions shore up confidence in bond stabilisation in tandem with confidence in policy being up with the inflation curve. On USD/JPY, a close back below 160.00 will add weight to sentiment and put focus on congestion around 159.00. Latest IMM data showed spec yen shorts had extend further into the post 2024 highs, so there is a short base there to squeeze but it still needs a trigger.

The RBA is also in focus overnight, not so much for rates, seen unchanged, but any dilution of the hawkish tone and clearer shift to data dependency.

Dollar direction overall though may remain lacking until Wednesday’s FOMC given the unusually large amount of uncertainty and information packed into this maiden Warsh meeting. EUR/USD is back to fairly neutral at the 1.16~ area prior to that, both in terms of levels and in terms of positioning. If Iran relief is sustained, and it further allows the Fed to avoid a stronger hawkish pivot, that could see a little stretch of the bounce (1.1650/70) but momentum isn’t strong.

In terms of the rest of the calendar Tuesday, there’s the latest ZEW survey data in Europe where some improvement in sentiment is expected on geopolitical progress hopes.

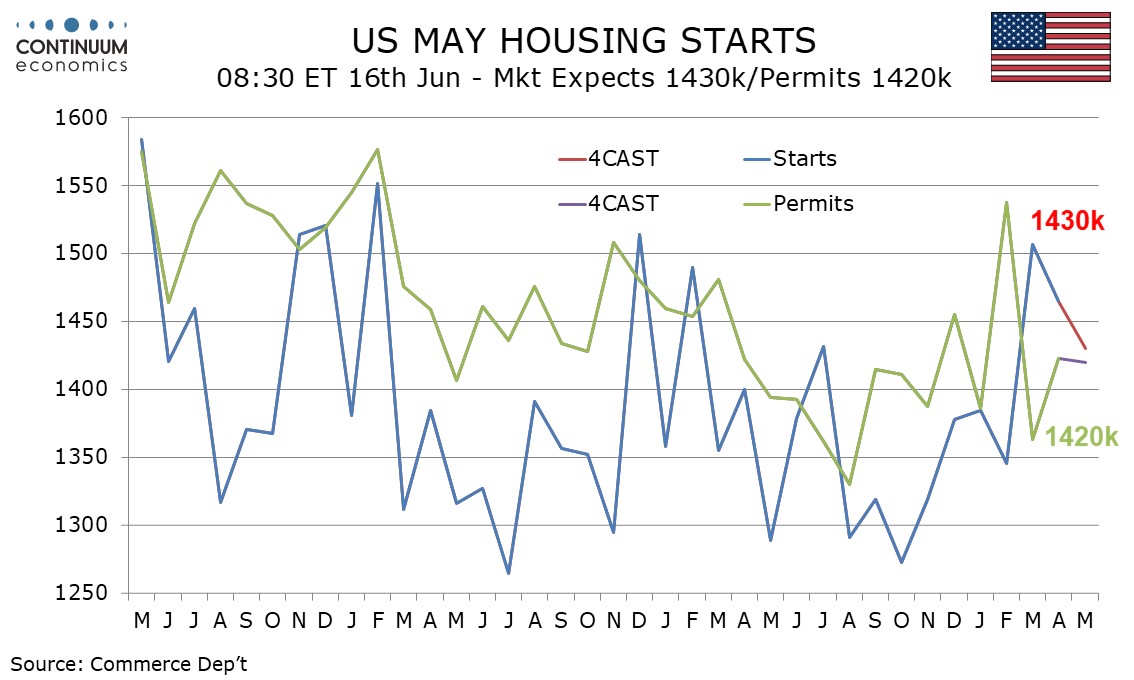

In the US, we expect May housing starts to fall by 2.4% to 1.43m, with permits falling by 0.2% to 1.42m. May import and export prices are also due.