Bank of Canada Preview for July 15: Reduced energy risk may see more attention on trade

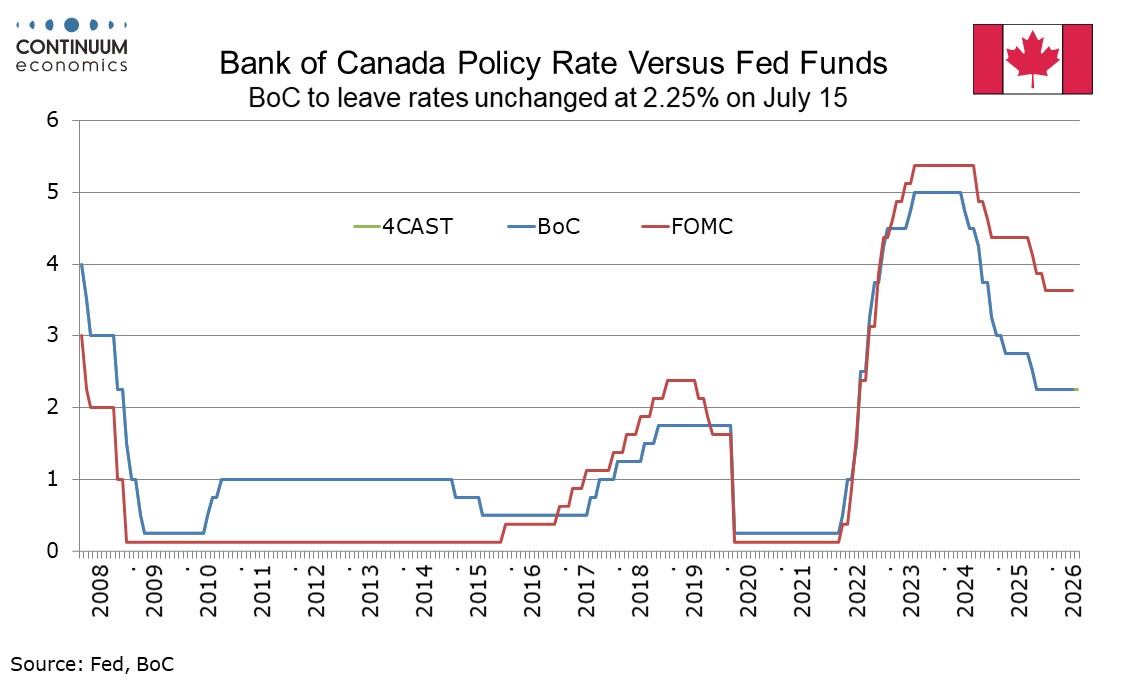

The Bank of Canada meets on July 15 and looks set to leave rates unchanged at 2.25%. The meeting will take place with inflationary risks coming from the Middle East having faded somewhat and escalation of trade tensions with the US a significant risk. This could lead to a dovish lean to the statement. Updates to economic forecasts are also due with the quarterly Monetary Policy Report.

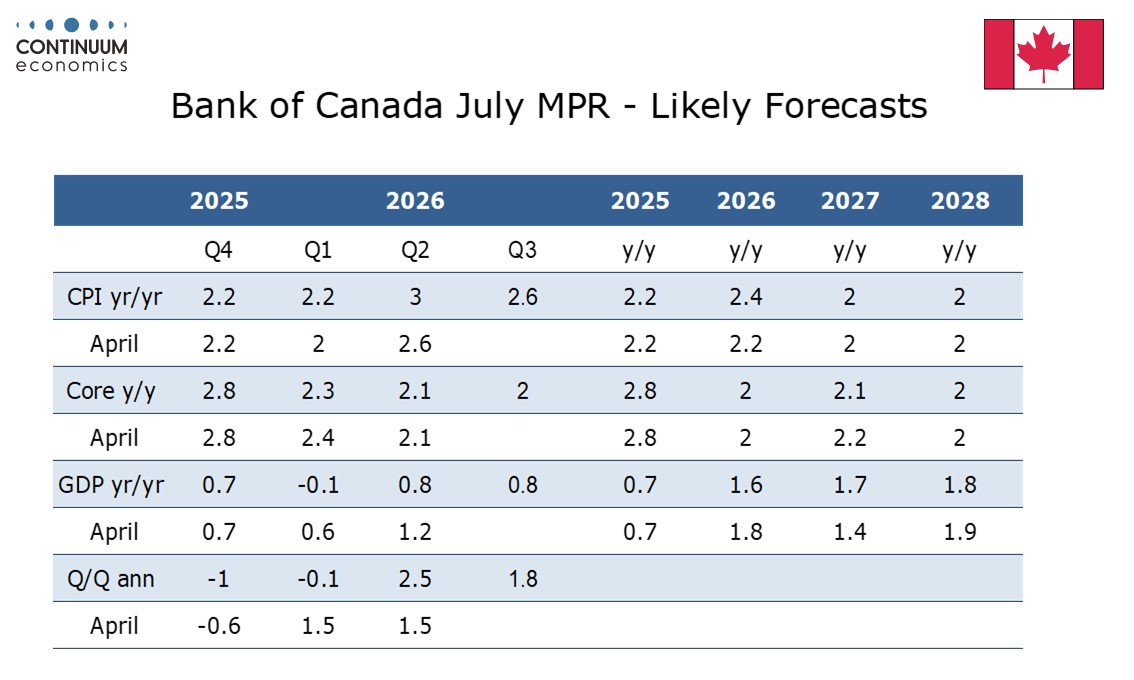

The Bank of Canada last met on June 10, but last updated its economic forecasts on April 29 when the last Monetary Policy Report was released. Since the last MPR Q1 GDP came in well below the BoC’s 1.5% annualized projection, at -0.1%, but early signals for Q2 are positive, with April GDP up by 0.5% on the month and May seen up by 0.1% in a preliminary estimate. This suggests Q2 will be stronger than a similar 1.5% BoC estimate made in April. 2026 GDP may still be revised a little lower, but that could be offset by an upward revision to 2027.

Q1 CPI at 2.2% yr/yr came in above a 2.0% April BoC forecast, and even with a modest slowing in June Q2 looks set to come in around 3.0%, versus a 2.6% April forecast. However core CPI (measured by the average of CPI-Median and CPI-Trim) has been in line with, or even marginally lower, than the BoC expected, and is now close to the 2.0% target. Recent declines in oil prices are likely to see headline CPI slowing in the second half of the year, and while year-end CPI may still be seen a little higher than the 2.2% seen in April, 2027 and 2028 will probably be seen close to target, both for overall and core CPI.

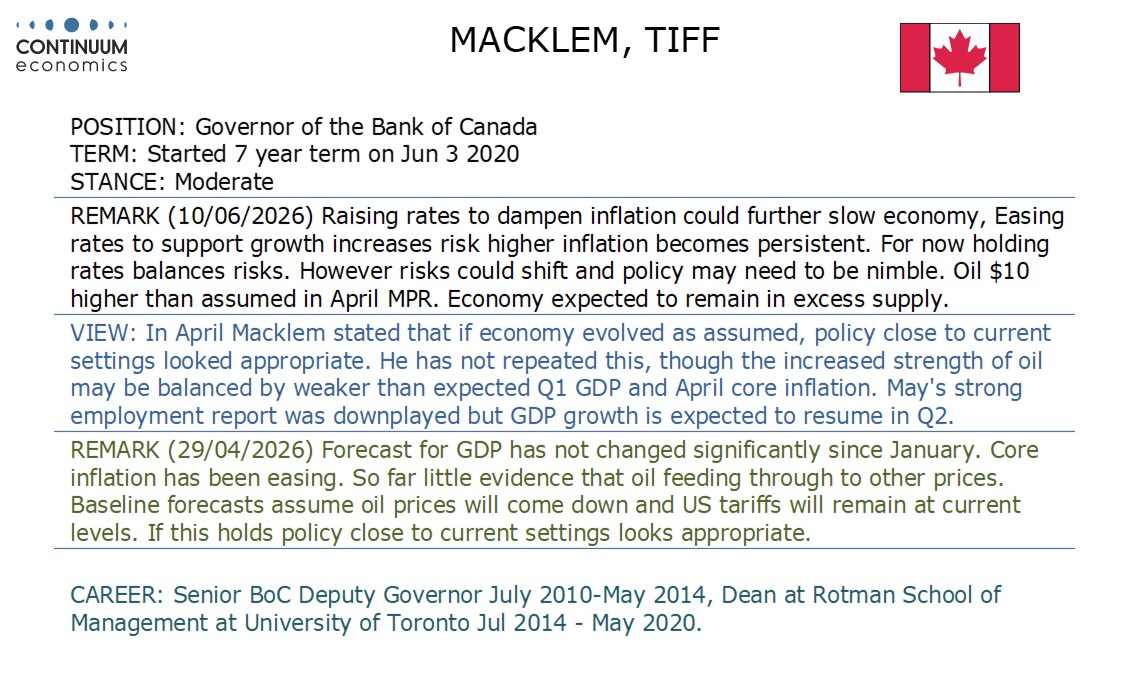

The picture on balance does not appear to have changed much since April, when BoC Governor Tiff Macklem stated that policy settings looked appropriate on an assumption that oil prices would come down and US tariffs remained at current levels. The BoC at its June meeting noted that oil prices were around $10 per barrel higher than assumed in April but prices are now more consistent with the BoC’s April view, suggesting that the rates level will be seen as appropriate. In both April and June the BoC stressed uncertainty and a willingness to implement consecutive tightenings should inflation become persistent and to ease should the US impose significant new tariffs.

The BoC is likely to again state a willingness to move rates in either direction, but inflationary risks have faded somewhat since the last meeting. Risks from the Middle East remain significant, but with the USMCA trade deal now due for renegotiation, risks of fresh US tariffs may be given greater prominence. We do not expect the BoC to move rates again until 2027, with 25bps tightenings in Q2 and Q3. That would put rates back in the midpoint of the 2.25-3.25% range the BoC sees as neutral.