FX Weekly Strategy: May 25th-29th

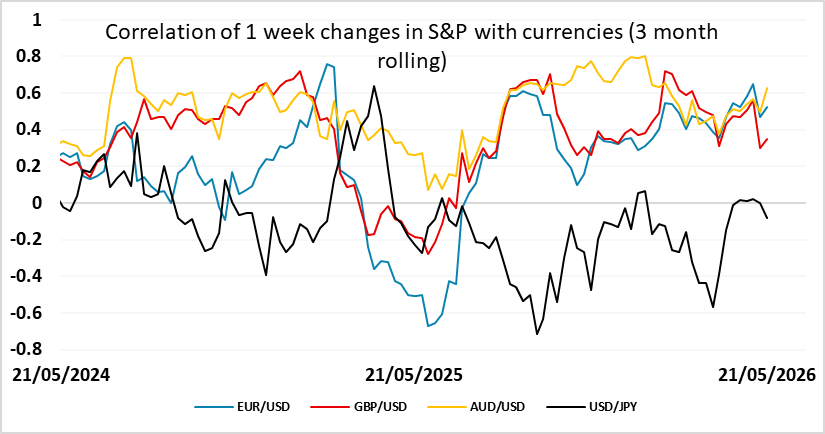

Resilient equity markets preventing much FX movement…

…but sell in May and go away makes sense this year

European currencies vulnerable to any turn lower in risk sentiment

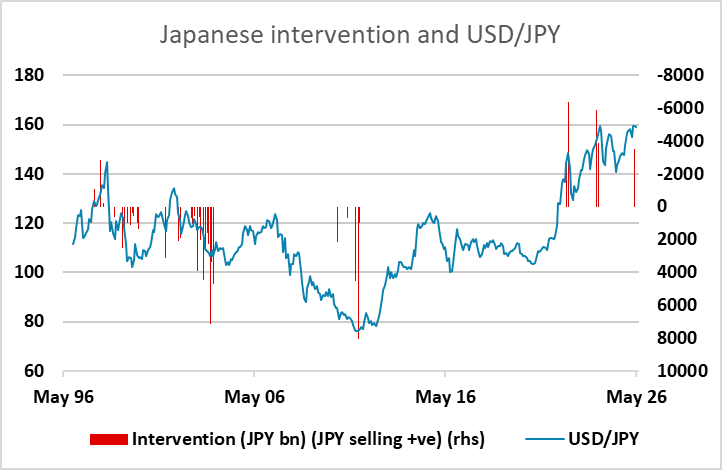

JPY remains favoured with BoJ protecting the downside

Strategy for the week ahead

Resilient equity markets preventing much FX movement…

…but sell in May and go away makes sense this year

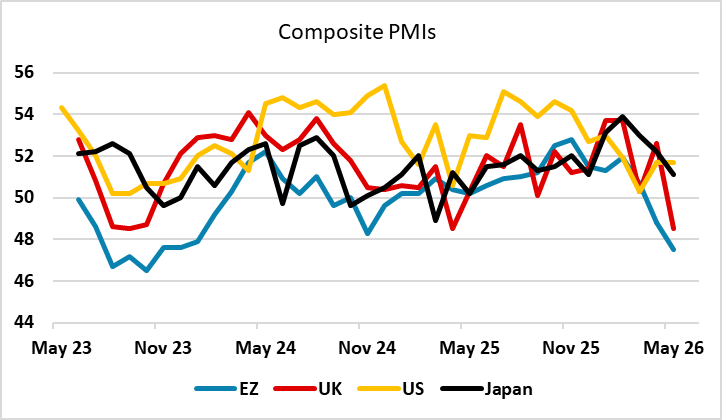

European currencies vulnerable to any turn lower in risk sentiment

JPY remains favoured with BoJ protecting the downside

This is the last weekly I will write at Continuum Economics. I am leaving after 8 years in the job. If any reader wants to contact me my e-mail is adrianschmidt@live.co.uk.

FX markets remain generally quiet. EUR/USD seems glued to 1.16 for the moment, in spite of evidence of some weakening in the survey data, both in this month’s PMIs and last month’s IFO survey. The US should be favoured on a relative growth basis, but the negative correlation of the USD with risk sentiment continues to hold back USD gains as long as equity markets remain resilient. But the strength of equity markets remains hard to justify on a longer term basis, especially given the current risks from the Middle East and the already high oil price and its effects on growth, which are already starting to emerge.

It is always hard to oppose momentum, but the motto “sell in May and go away” may be apposite this year. The higher oil price should both limit the scope for lower yields and undermine real consumer spending in most major economies, which together should be equity negative. The US, Canada and Norway (and to a lesser extent the UK) benefit to some extent from being oil producers, but this won’t prevent them from suffering some growth slowdown. While equity markets are benefiting from AI optimism, it should also be recognized that even if AI does have a positive impact medium to long term, there are also big transitional risks to the economy, and a lot of the good news is already priced in.

So we see underlying risks for the traditionally riskier currencies. Of the safe havens, the JPY remains obviously undervalued, and with the BoJ defending against USD/JPY gains above 160, the risks look to be heavily weighed to the JPY upside. If the USD gains in general, the JPY should gain on the crosses. If the USD suffers, either because geopolitical risk fades or the US economy starts to show some weakness, the JPY should have upside scope against the USD.

As far as this week is concerned, there isn’t a huge amount on the calendar. The market will be looking for progress in the US/Iran talks, and this may be the primary market mover. CPI data in the Eurozone might impact expectations for ECB action in June, but there is already a strong case for the EUR to weaken based on yield spreads, so the risks should be mainly on the EUR downside.

Ueda’s speech on Wednesday could be a focus for the JPY, but as we have often noted, changes in Japanese monetary policy have not tended to have much impact on the JPY with risk sentiment largely dominant. Having said this, the JPY is even weak relative to the usual risk metrics since the new government came in last August ,The fiscal fears associated with that have now faded, increasing the case for a JPY recovery.

Data and events for the week ahead

USA

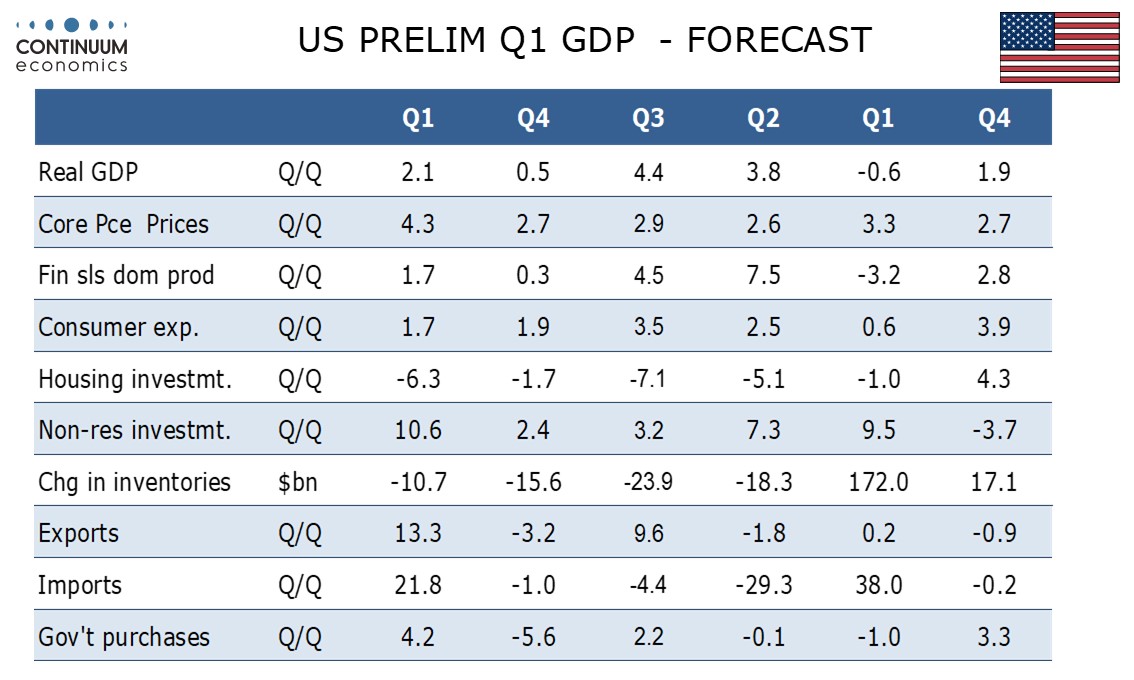

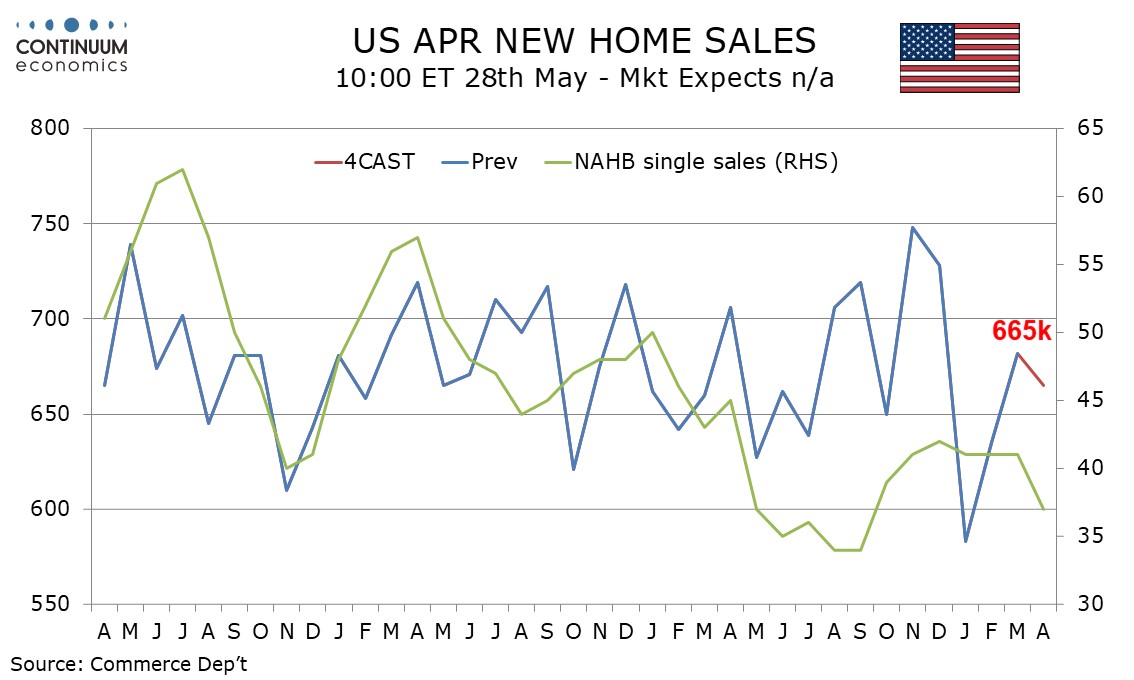

After Monday’s Memorial Day holiday Tuesday sees March house price data from FHFA and S and P Case-Shiller, followed by May consumer confidence. Wednesday sees only minor data releases, but Thursday will be busy. We expect a 0.3% rise in April’s core PCE price index, with overall PCE prices up by 0.5%, personal income up by 0.3% and spending up by 0.5%. We expect Q1 GDP to see a marginal upward revision to 2.1% from 2.0%, and April durable goods orders to rise by a strong 4.5%, with a 0.9% increase ex transport. Weekly initial claims ate also due. April new home sales follow, where were expect a 2.5% decline to 665k. On Friday we expect the advance goods trade deficit to rise to $90.0bn in April from $87.45bn in March. Fed’s Williams will speak on Thursday with Paulson due on Friday.

Canada

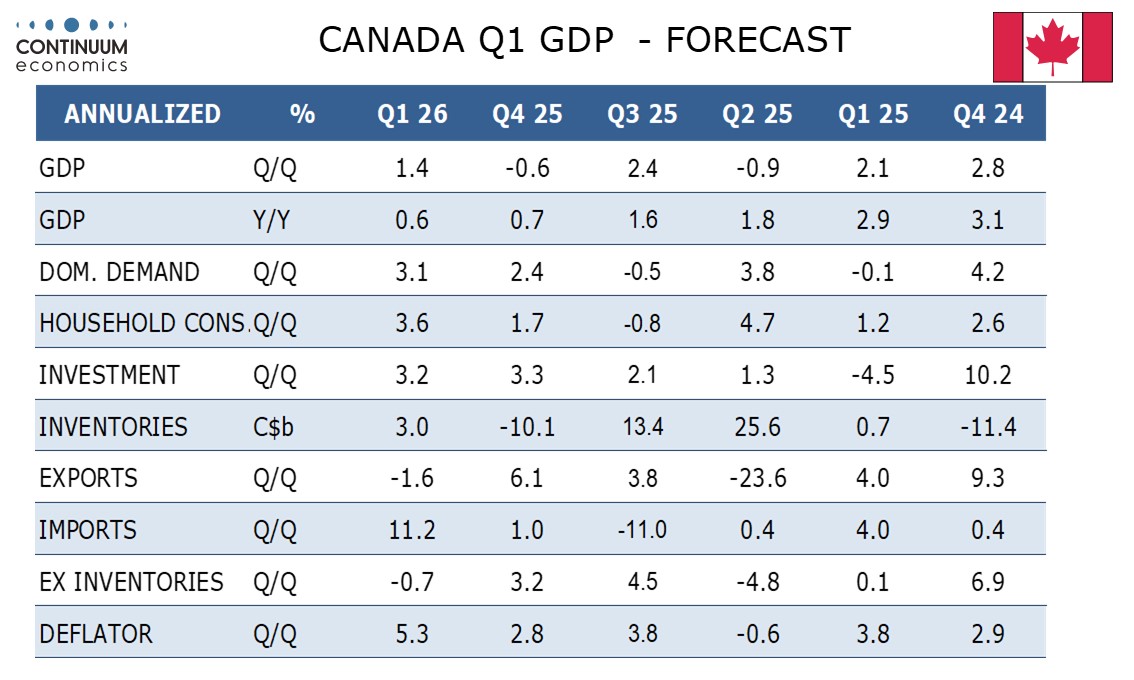

In Canada Q1’s current account is due on Thursday with Q1 GDP on Friday. We expect a 1.4% annualized increase in GDP, close to a 1.5% Bank of Canada estimate with details mostly positive outside a decline in net exports. We expect March’s monthly GDP data to be unchanged, in line with a preliminary estimate.

UK

Especially with Monday’s holiday, it a quiet week ahead, with perhaps a key event being BoE Governor Bailey speaking (Fri). There may be house prices data from Nationwide, likely to tell a somewhat sorrier story.

Eurozone

There are various important data updates due before the EZ HICP data in early June which will be preceded by national CPI/HICP data with key German data (all due next Fri) and where we see a relatively larger May preliminary reading jump from 2.9% to 3.3%-3.4%, the question being the extent to which such a pick-up remains almost entirely energy driven – NB there is a risk that service prices may have started to edge higher even though retail fuel costs may be relatively steady! But survey data will also be important with it key to see if European Commission numbers (Thu) chime with the downside growth risks posed by May’s flash PMIs. Otherwise, there are ECB (and UK) speakers at a BoJ conference (Thu).

Rest of Western Europe

There are some key events in Sweden, where more bad news may come in the Economic Tendency Survey due on Thursday and then the Riksbank’s Financial Stability Report (Fri). Friday also sees Q1 GDP numbers likely to confirm the contraction seen in the monthly indicator. In Switzerland, Friday sees the latest KOF survey update. Norway on Tuesday releases the latest credit numbers, alongside updated Unemployment figures. GDP numbers (Thu) may show still positive growth for Q1, but possibly half that seen in the Q4 mainland result.

Japan

Tokyo CPI on Thursday will normally capturing more eyeballs but market participants have already anticipated a stimulus watered down number. Besides, most are looking forward to Ueda’s speech on Wednesday as it could provide cues for BoJ’s take on recent yields rally. The key point to note will be change of pace in bond purchase tapering or any mention of special operation. We also have retail sales and labor data on Thursday that will likely be overlooked.

Australia

Monthly CPI on Wednesday will points toward inflation target being breached. The magnitude of y/y impact will likely be greater than m/m. Yet, the triple hike from the RBA could keep them from aggressively hiking more in the coming months. Thus, Aussie reaction could be purely knee-jerk.

NZ

The all important RBNZ rate decision is on Wednesday. Widely expected to be a non-event but as inflationary pressure creeps in, the RBNZ may have to revise their baseline scenario. It could contribute towards a hawkish tilt in forward guidance yet unlikely a surprise hike.