Preview: Due June 25 - U.S. May Personal Income and Spending - Core PCE Prices to outperform CPI, Savings to fall further

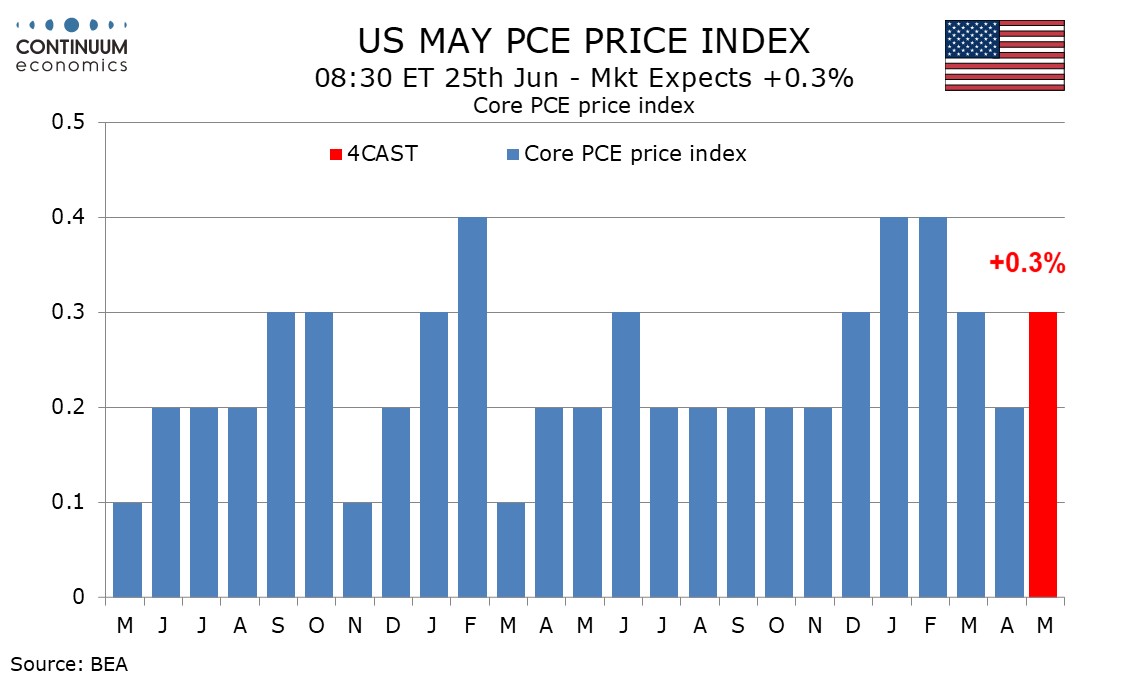

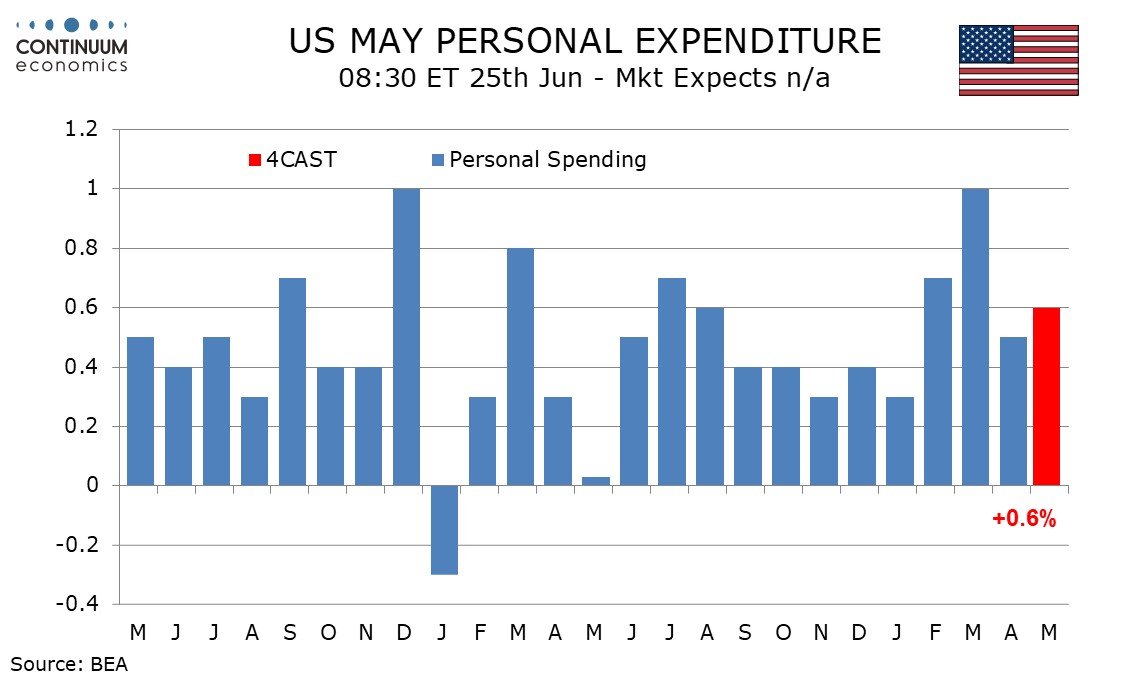

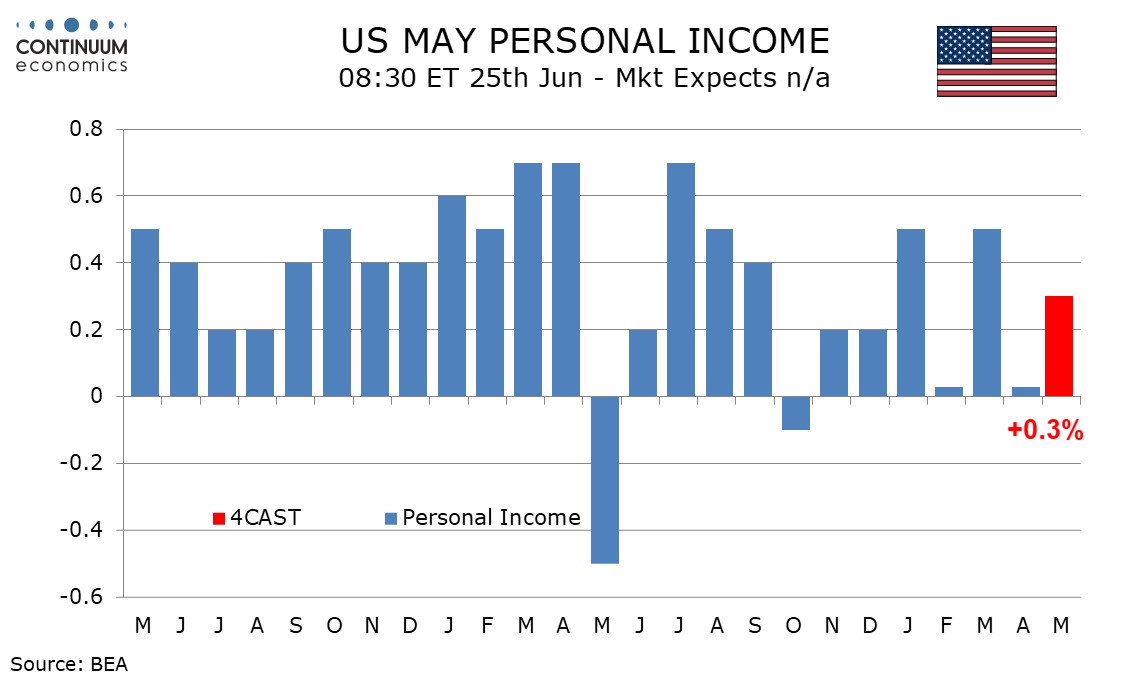

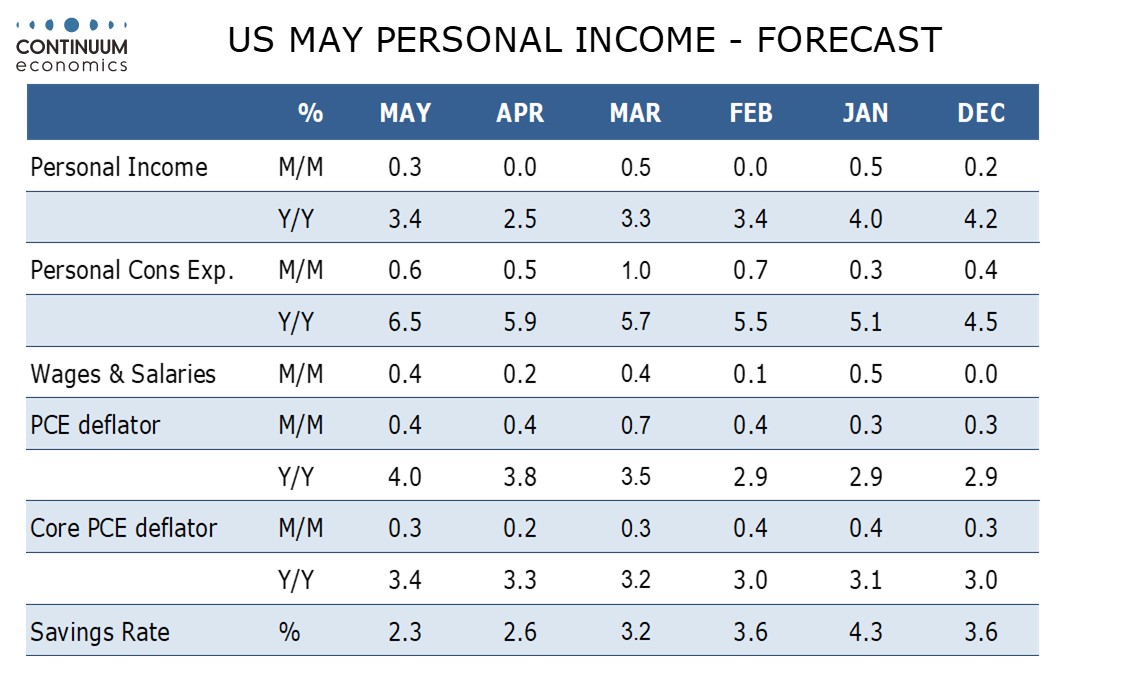

We expect May’s core PCE price index to rise by 0.3%, though probably on the low side of 0.3% before rounding, with overall PCE prices up by 0.4%. We expect a 0.6% increase in personal spending to outperform a 0.3% rise in personal income, extending a recent sharp decline in savings.

A 0.3% rise in core PCE prices would be stronger than a 0.2% rise in core CPI, which was 0.21% before rounding, Strength in May’s PPI suggests core PCE prices could exceed the core CPI, though the gain is likely to be only marginally above 0.25%.

Overall CPI rose by 0.5%. or 0.47% before rounding. PCE prices tend to be less sensitive to gasoline than CPI so we expect overall PCE prices to underperform the CPI even with outperformance on the core rate. Yr/yr data would then show overall PCE prices at 4.0% versus 3.8% and the core rate at 3.4% from 3.3%, reaching their highest since May 2023 and October 2023 respectively.

Retail sales rose by 1.0% if a soft month from eating and drinking places (which are included in services consumption) is excluded. We expect a third straight 0.4% increase in services consumption leaving overall personal spending up by 0.6%.

May’s healthy non-farm payroll detail implies a 0.4% rise in wages and salaries. We expect overall personal income to rise by 0.3% as the other components of personal income return to a subdued trend, following a decline in April that corrected a strong March inflated by farm income.

Spending outperforming income would see the savings ratio slip to 2.3% from 2.6% in April, which was already the lowest since June 2022, when consumers were using up savings built up during the pandemic. Weak savings imply downside risk to consumption going forward despite May resilience.