Sweden Riksbank Preview (Jun 17): Mild Tightening Bias to Persist But Not Exercised?

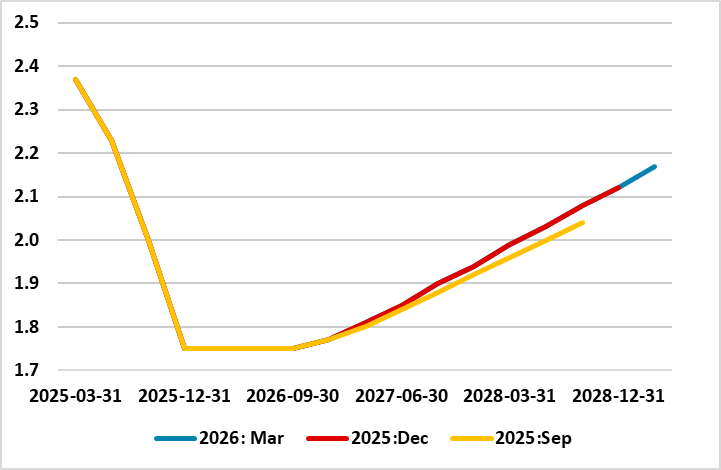

Not only at the meeting next week, we still see stable policy though to end-2027 rather than the small hikes markets are now pricing for late 2026. A similar profile has been offered by the Riksbank since last autumn (Figure 1) and it may decide to bring forward its first hike hint a touch when it presents it updated Monetary policy report alongside its next verdict. Indeed, in March, it tweaked its forward guidance by suggesting that, even amid Middle East conflict making the outlook very uncertain, it was in a good initial position to adjust monetary policy if required to safeguard the inflation target and no longer pointed to no change for some time to come. Somewhat better data in the last on both the GDP and CPI fronts may even harden this guidance, but underlying inflation is still well below Riksbank thinking while its own survey data and the labour market (Figure 2) provide a timely reminder of on-going economic fragility.

Figure 1: Riksbank Policy Rate Outlook

Source; Riksbank Monetary Policy Report

Indeed, the just-released Riksbank business survey underscores both downside risks to growth and inflation. It notes that due to the Middle East conflict uncertainty has increased again, which the companies involved say risks delaying the already prolonged recovery. At the same it notes that while companies do intend to increase their selling prices in the coming year, they emphasise that it is very uncertain to what extent higher costs will actually be reflected in the prices so that at the current juncture they are talking about small price increases. As for actual price trends, the latest CPI figures surprised on the upside (for once). Even so, perspective is needed as CPIF excluding energy (CPIFXE) – an official indicator of underlying inflation – is still only 0.5% y/y, ie almost half the Riksbank's forecast from its most recent March projections

It is always notable how quickly things can change, especially when it is external events that precipitate a shift in the backdrop and outlook. Notably, with inflation and real economy numbers having undershot both its and consensus expectations, the Riksbank might have been contemplating a fresh easing at this juncture if not for events in Middle East. Regardless, the Board has developed a tightening bias, presumably on the fact that the Iran conflict has proved more durable than it previously thought/hoped. In fact, it may even have hiked at this juncture, or given a more explicit tightening bias but could not do so given the downside surprises in both recent CPI and real economy data. And the question is whether the most recent fall in energy prices of late will temper any added Board hawkishness.

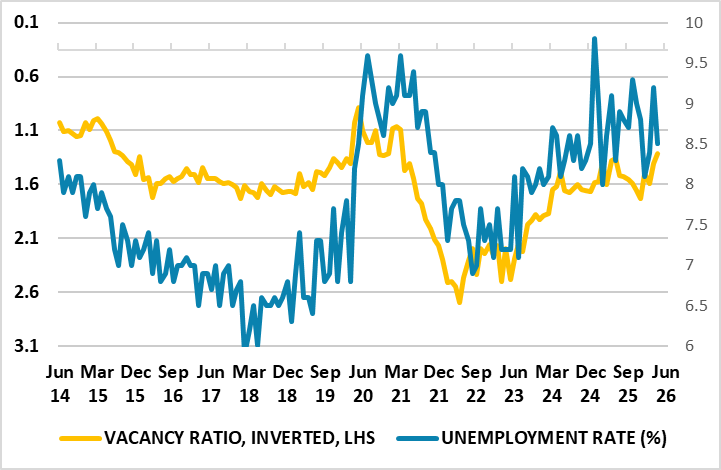

Figure 2: Jobs Harder to Find

Source; Stats Sweden, CE

Otherwise and as we have suggested repeatedly, the current (ie made in March) 2.2% Riksbank GDP projection for this year made in March is increasingly optimistic, possibly by a factor of two, not least after a clear q/q drop in Q1. In this regard, the real economy backdrop is still puzzling and meriting more of a reassessment. But the outlook is even more puzzling given that GDP growth would have to average over 3% annualized in the rest if the year to get to the Riksbank outlook. Despite an apparent 2%-plus GDP jump in the last three quarters if 2025 (twice Riksbank thinking), the economy still looks soggy, not least in the labor market where the vacancy ratio has fallen markedly (Figure 2). Admittedly, much of the recent rise in unemployment to around 9% of late looks to be a result of increased participation, but does this reflect a need by households to boost what have been damaged (real) incomes; if so then there may be little respite with the rate staying around current levels for at least the rest of this year.

It is against this background where we now see a GDP growth outcome nearer 1.4% for this year, with weaker exports causing clear damage that, alongside the likely Q1 drop. Helped by fiscal policy and the anticipated fall back in energy prices we see GDP growth outcome nearer 1.7% next year still below Riksbank thinking but which very much suggests a negative output gap, at least until 2028.