Mexico: Banxico Pause, But MXN and USMCA Renegotiations

· As expected Banxico left the policy rate unchanged at 6.50%, with the focus now on the lagged benefit of easing and also what will happen with the USMCA negotiations. Banxico will likely keep the current policy rate through end 2026, given concerns that the Fed could tighten – even in 2027 we see stable policy rates, while the Fed ease 50bps. On USMCA we will see a volatile phase over the summer that could see MXN move lower, but Trump likes Mexico more than Canada. We expect an agreed addendum by end 2026/early 2027.

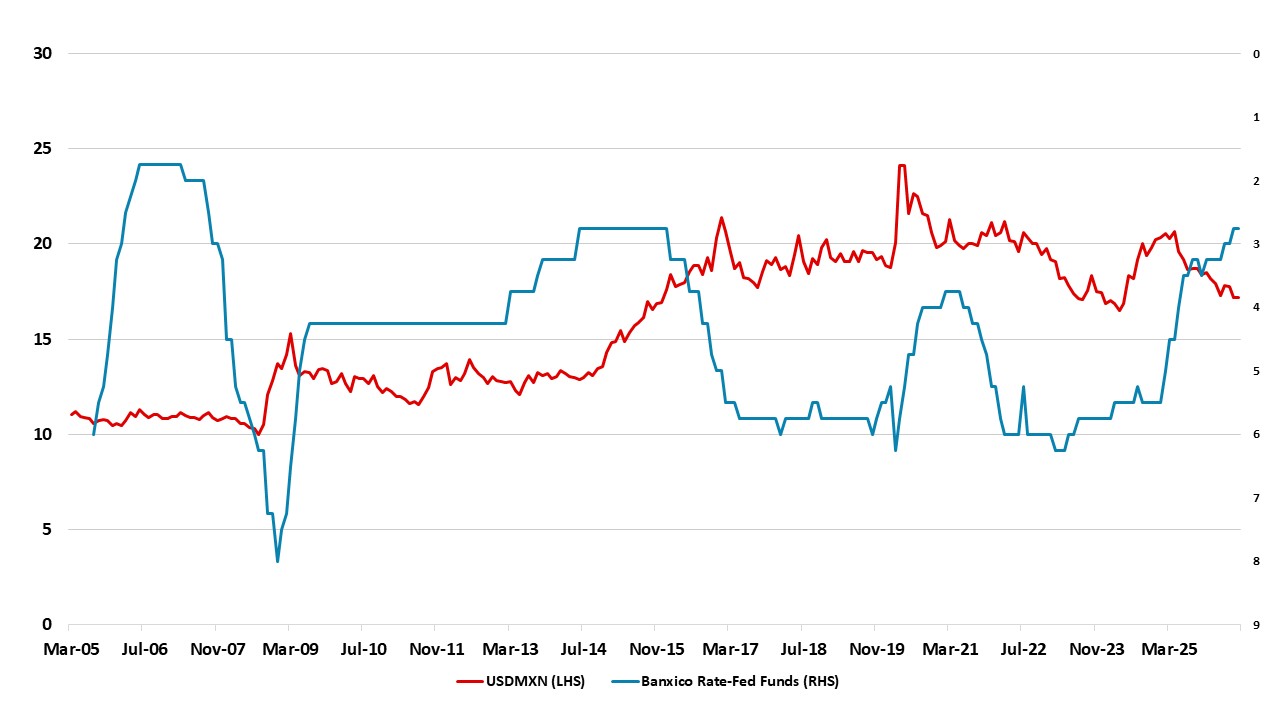

Figure 1: USDMXN and Inverted Banxico-Fed Funds Policy Rate Spread (%)

Source: Datastream and Continuum Economics

The MXN has remained resilient after an initial knee jerk selloff on the Iran war. However, the USMCA is an event risk, as the U.S. will likely negotiate hard during the summer. USTR Greer is clear that Trump wants separate addendums for Mexico and Canada for the USMCA, which suggests that bilateral threats could still increase volatility when negotiations intensify around July 2026. This may mean that MXN could see a correction through mid-year. It also worth noting that the MXN has now become overvalued versus 10 and 25yr average on an REER basis, which leaves MXN vulnerable to domestic bad news or global risk off. This could bring USDMXN back to 17.75 MXN, with the USMCA negotiations. Even so, MXN will be supported by the view that U.S./Mexico will agree a renegotiated USMCA successfully by early 2027, given President Sheinbaum willing to compromise with Trump. We see USDMXN at 17.65 by end 2026.

For 2027, though we expect the Fed to cut by 50bps and the Banxico to remain on hold, the multi-year policy rate spread between Mexico and the U.S. is below average. The MXN lost ground 2014-17 when the policy rate spread was this narrow in the past. The cycle of MXN rebound and narrowing bond spreads has become mature for global investors and the BRL looks more attractive. This can see the MXN slipping to 18.00 on USDMXN by end 2027, given the current MXN overvaluation on a REER basis.