China LGFV Repair Rather Than Reboot

• Our assessment is that this ongoing exercise will likely have a small boost to GDP growth. LGFV’s debt restructuring could allow some new borrowing, but the big issue is that LGFV and LG finances are dependent on one off property taxes with the building of new property. The overhang of housing supply and lower structural demand due to population aging argues for no major rebound in new construction in the next few years.

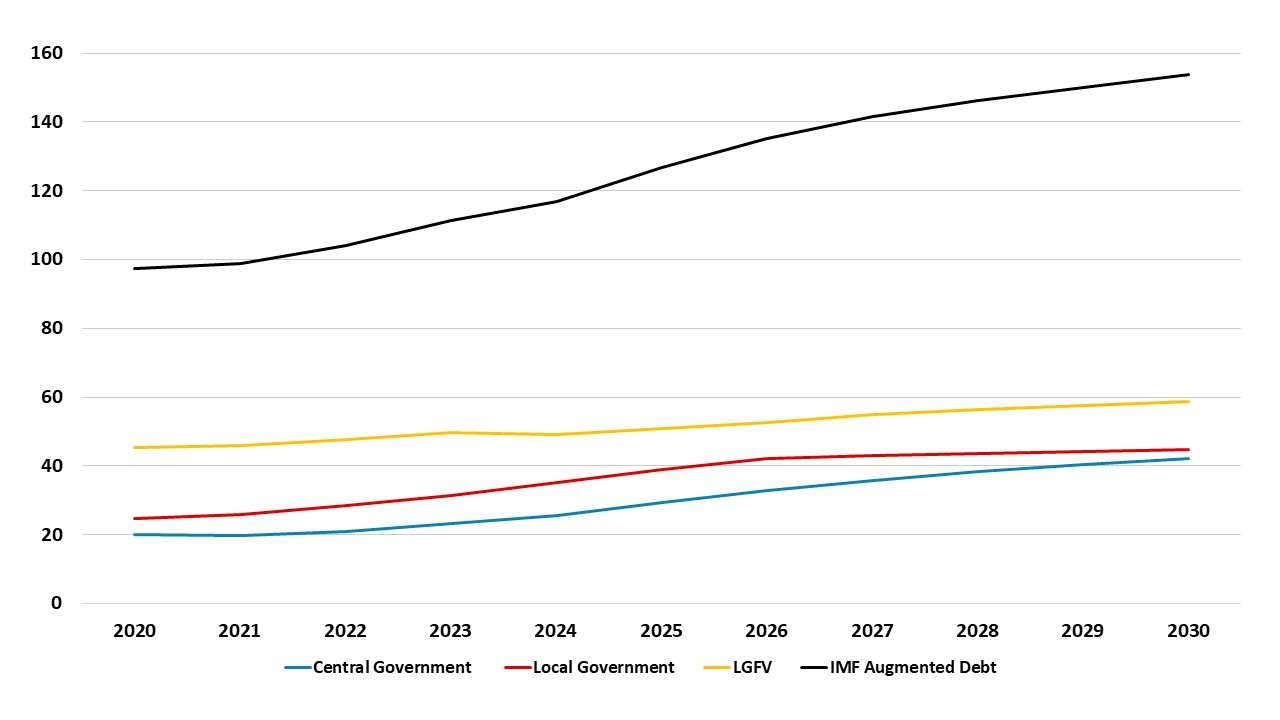

China is restructuring Yuan10trn of Local Government Financing Vehicle Debt (LGFV), which is the largest portion of the IMF measure of augmented general government debt (Figure 1). Could this reboot this also help growth?

Figure 1: LGFV Debt the Biggest Portion of IMF Augmented Debt Source: IMF Article IV Feb 2026

Source: IMF Article IV Feb 2026

China in 2024 announced a 5 year restructuring of Yuan10trn LGFV debt, with two main focal points. Firstly, a takeover of the debt by local government (LG), which would both reduce debt servicing costs and length the average maturity of debt. Moral suasion from the authorities would convince domestic institutional investors and banks to buy the LG debt and help smooth the process. Secondly, remaining LGFV’s would be encouraged to transform into non-financial corporations, with the 2026 IMF article IV noting that 71% of the 18000 LGFV have been reclassified to NFC’s in 2025. However, this latter process is not making these LGFV’s financially sound – China authorities debt measure only includes central and local government debt in Figure 1 and they have had a long running disagreement with the IMF on the scale of official debt.

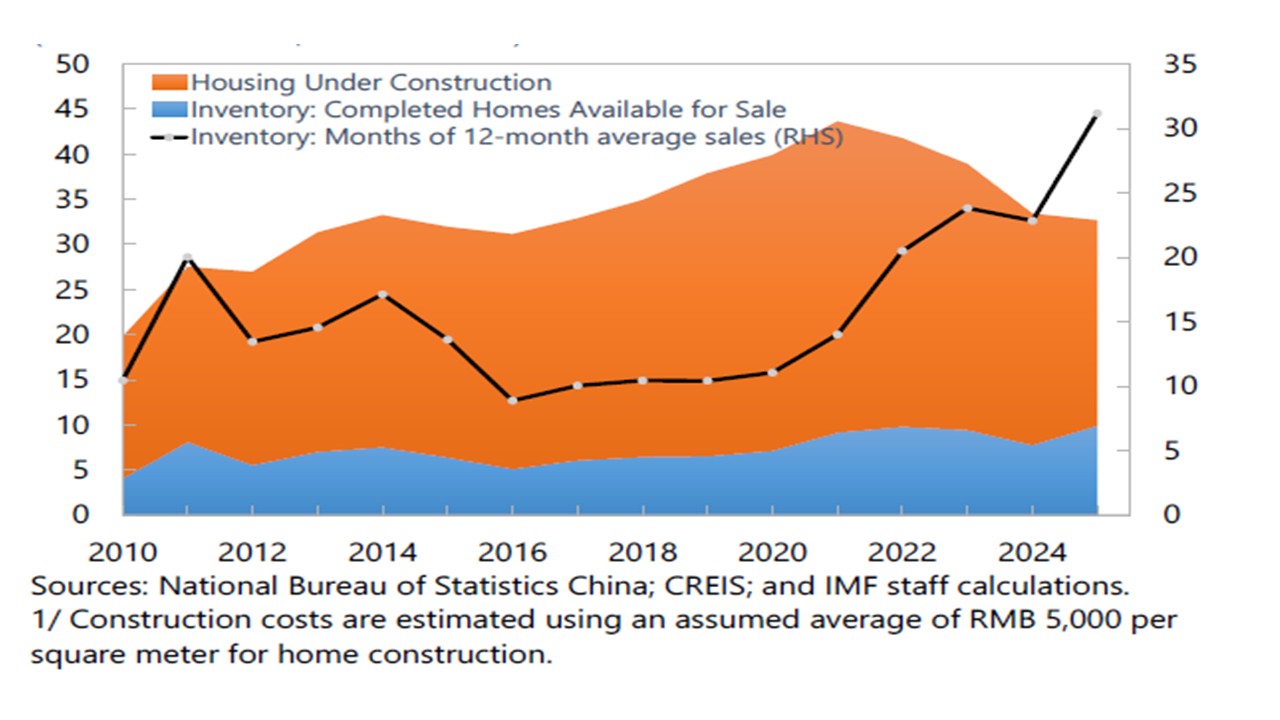

Our assessment is that this ongoing exercise will likely have a small boost to GDP growth. LGFV’s in 2023-24 had been sluggish and an adverse headwind to infrastructure spending and so less worse finances could help to encourage some more investment relative to 2023-24 from this sector. Even so, the monthly fixed investment data has been sluggish at times in H2 2025, due to soft LG and LGFV spending! The big issue is that LGFV and LG finances are dependent on one off property taxes with the building of new property. However, though the residential property sector is getting less worse, the overhang of housing supply (Figure 2) and lower structural demand due to population aging argues for no major rebound in new construction in the next few years. This leaves LGFV and LG finances structurally weak and unlikely to reboot infrastructure spending substantively. This places extra weight on central government infrastructure investment, but each March the extra measures are modest rather than aggressive. Though the authorities argue that government debt is lower than the IMF measure, they act fiscal restrained as though taking account of the IMF measure of debt.

Figure 2: Housing Supply (LHS RMB Trlns end of period; RHS Months of Supply)

Source: IMF Article IV Feb 2026

Source: IMF Article IV Feb 2026