FX Daily Strategy: N America, Jul 16

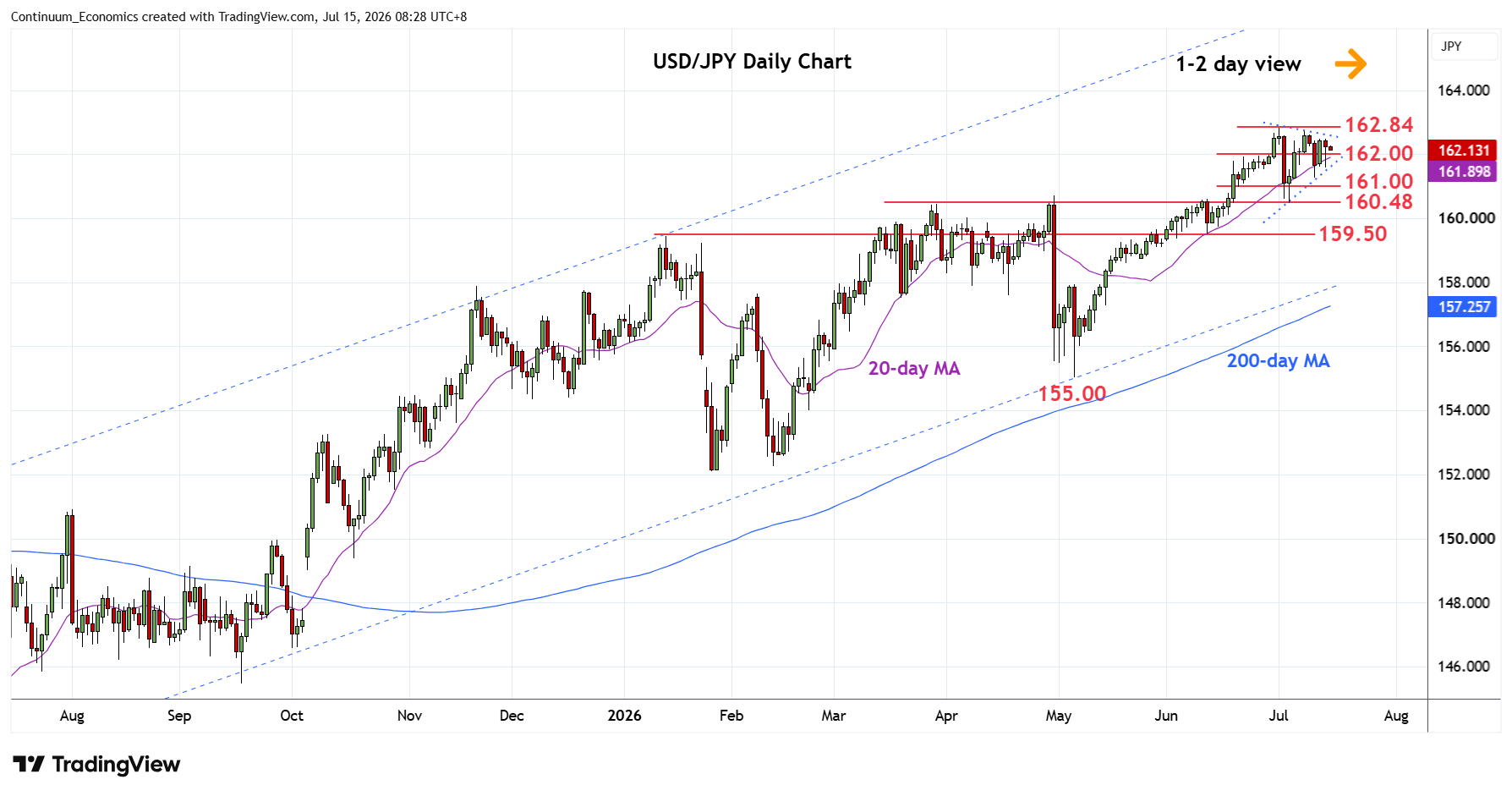

Approaching Japan holiday, so (idle?) speculation might kick in again

Dollar was over-owned, leaks out when headlines quiet

With the market mindful of the self-generated (and maybe spoof enhanced) setback seen into the US holiday, this naturally brings Japan’s Marine day on Monday into focus.

In reality, the argument for MoF to rock the boat with sudden guerrilla action intervention doesn’t feel compelling. But that regardless, it is worth being on alert for real and imagined noise over the next couple of days - some spec interest might indeed decide to step to the side just in case which could allow some nearby slippage.

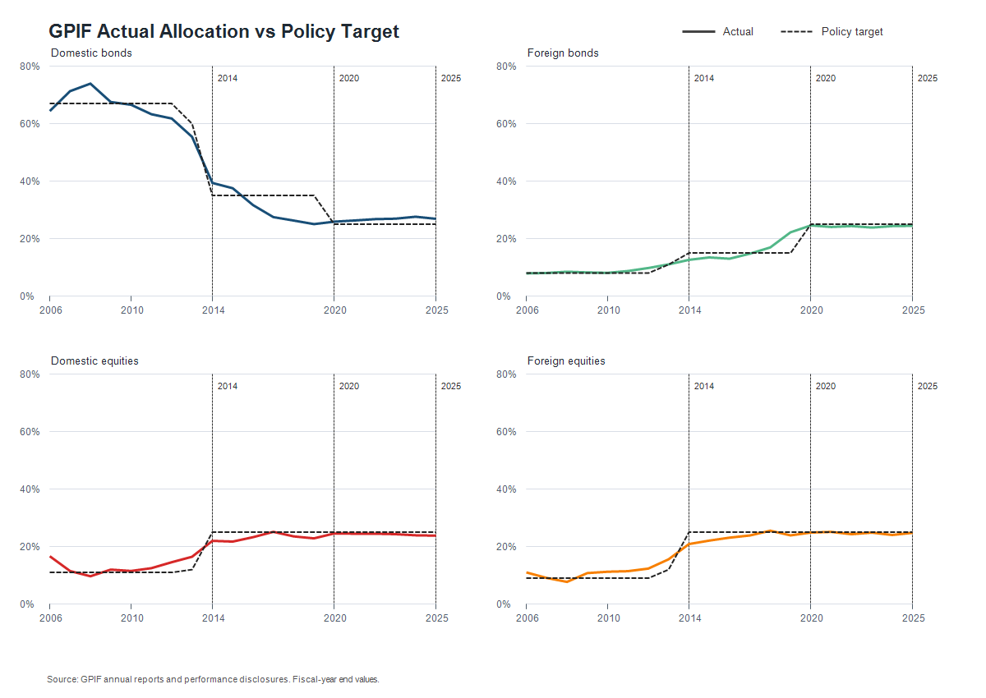

In terms of the broader story, MoF’s attention does seem to have moved on to more strategic ideas though, as highlighted by the GPIF explorations (see here for more on that). It is interesting that some banks do seem to be suggesting anecdotally that maybe some real money and hedge fund adjustment has started to come through on the back of this possible environment shift, although if that’s the case its not really evident in the price action yet it has to be said.

On Thursday, the main European interest came from UK GDP – May coming in broadly as expected at 0.1%m/ albeit with back revisions lifting the rolling 3m/3m rate, while leaving the yr/yr rate as expected.

On the back of recent renewed Iran worries, like most other majors, the BoE is back to being priced by the market for two hikes, if slightly slower (first by November, second by March). The market outlook is more hawkish than our central view – we do see market driven tightening coming through channels like mortgage resets over coming months and the economic picture is expected to weaken. It does need to be acknowledged though that an entrenched abnormal Strait scenario and ongoing supply side impact does make the Bank’s position more challenging especially if food prices also do pick up on the back of various factors like weather and input costs.

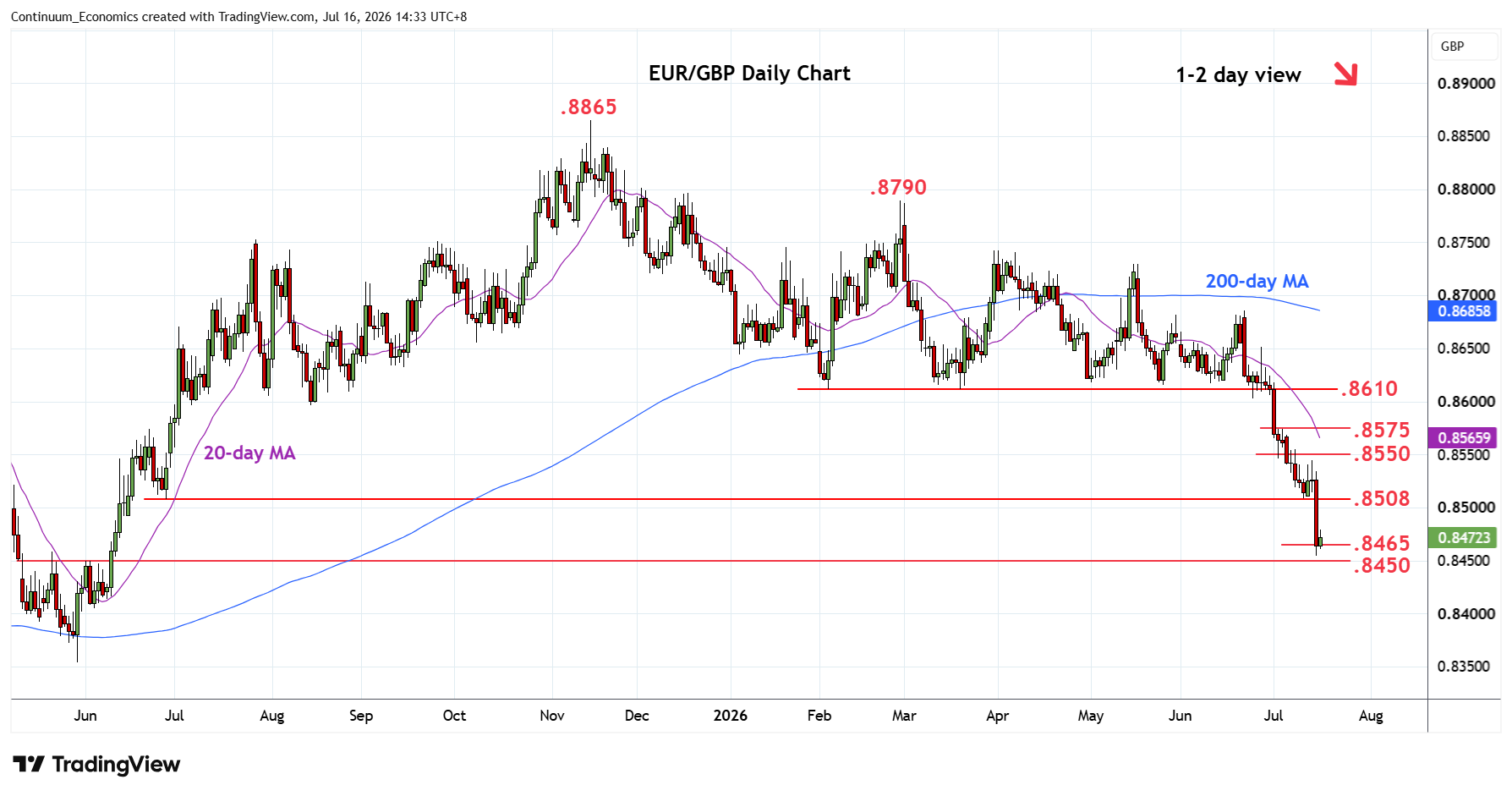

We noted in the early edition that near-term sterling is still tending to focus more on the backdrop coming from the short spec base as well as some politics monitoring, with appointment of Mahmood over Miliband to be taken as sterling positive. This did actually played out late yesterday as the press looked to unofficially confirm the market's favoured appointment, which , together with wider dollar leakage out of the CPI-PPI data, help to squeeze cable and break EUR/GBP downside further, with further short covering on sterling forced through.

That saw the 0.8508/00 prior support give way as well as 0.8475/70 (Jan25 high and 61% back) tested through to 0.8450 round figure before some backfilling to the retracement level . Cable at 1.3550 congestion. Sterling short squeeze now a little overbought intraday but still looking firm, 1.36-1.3650 is the post April range tops and that offers an obvious consolidation area for more two-way flow, as some profit-taking on the range rally comes through

In the US, data has recently been tending to show a lift to sentiment and activity and a drop back in price pressures, but with a large amount of uncertainty over how much of this is durable, especially given the renewed geopolitical backdrop and lift to energy prices.,

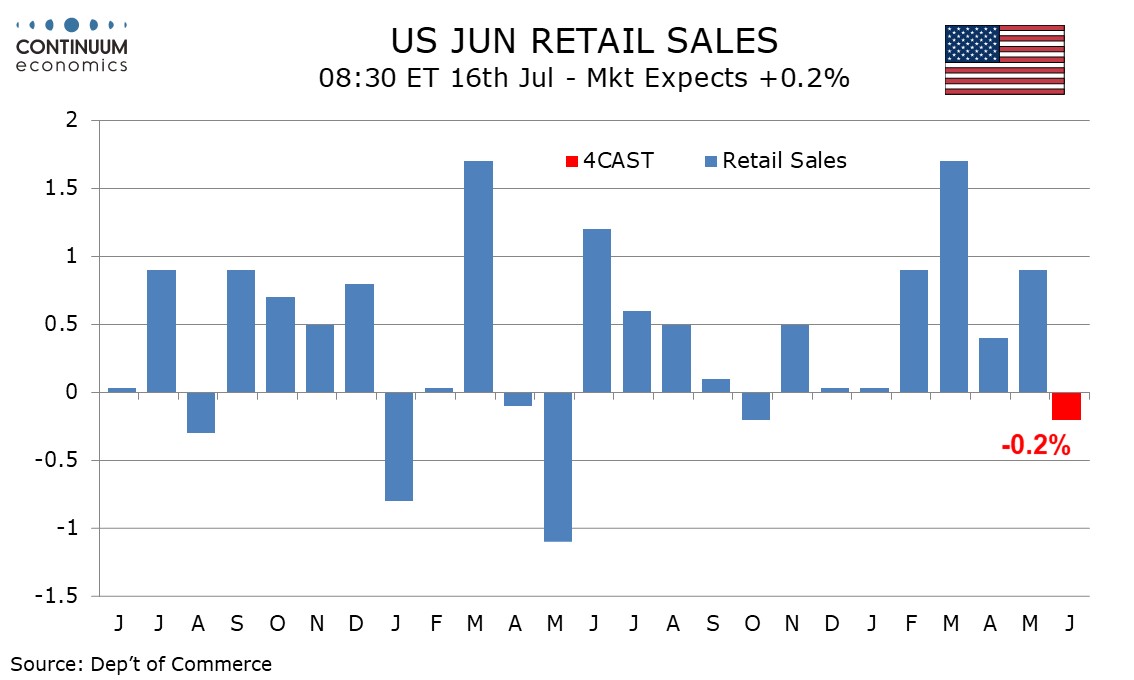

Thursday sees weekly initial claims and June retail sales. The latter will be watched to see if recent consumer resilience persists. We expect a 0.2% decline overall and a 0.4% decline ex autos, but a 0.2% increase ex autos and gasoline. May business inventories, where existing data suggests a rise of 0.6%, July’s NAHB homebuilders’ index, and June pending home sales follow.

The dollar having got a bit overbought has tended to lean a bit heavy (at least when its not being spiked by headlines).

Most pairs have been a bit dollar-heavy by virtue of that long positioning and we saw that baggage drive a burst of dollar leakage across the board late yesterday, with EUR/USD stretching the recent tight upside cap and widening that out to 1.1450-1.15 now.

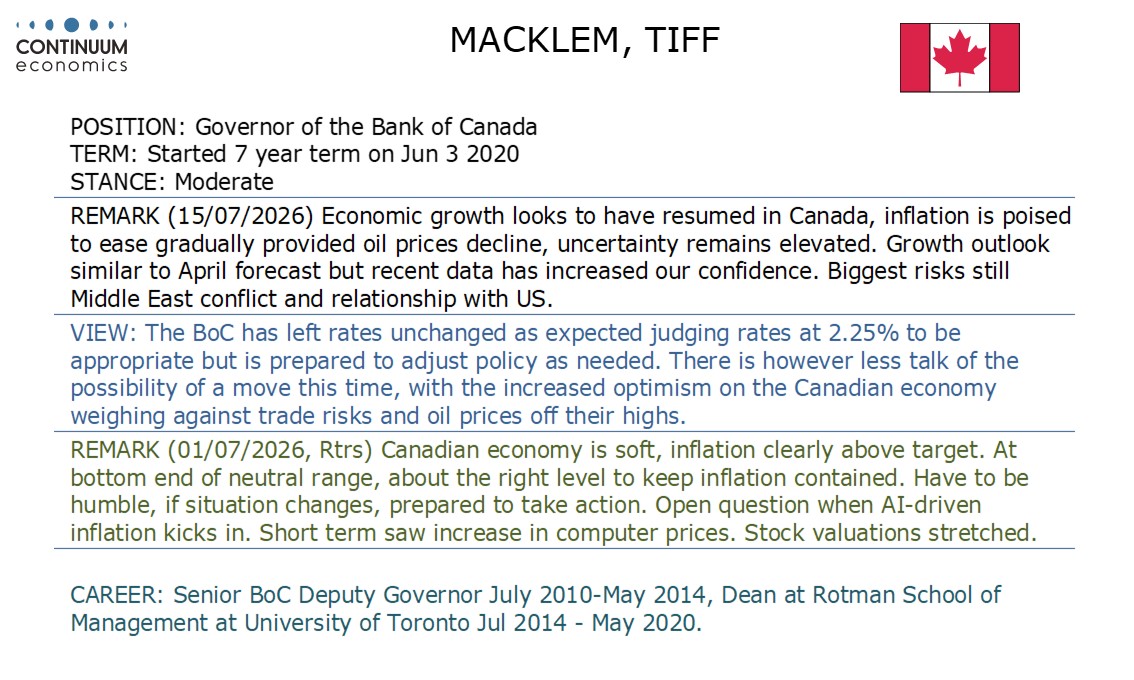

USD/CAD was one such, and did in the end manage the suggested stretch to the target of 1.4/1.398~ (38% retracement), That came from the dollar side as the BoC didn’t seem to give the market much initial further impetus, slightly disappointing its hopes for something a bit more tightening-biased perhaps. The Bank is more positive on the economy though still highlighting the huge risks and uncertainties and in no hurry to be changing policy. CAD, like other pairs, more driven in the last few hours by dollar positioning more than domestic drivers, though the recent mark up in oil, coming together with a lack of FX and risk volatility, hasn't harmed either.