FX Weekly Strategy: APAC, Jun 8-12

Dollar breaking higher on a number of pairs, US CPI next data of note

Fed repricing and tech adjustment could drag the likes of AUD/USD

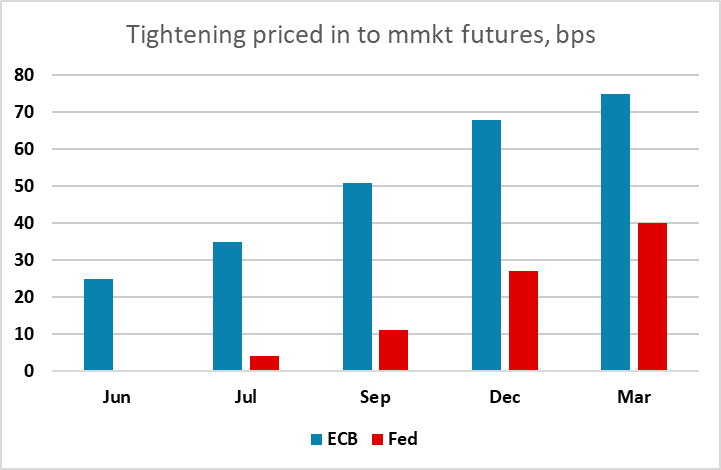

ECB hike already 100% odds. Given 2 more hikes in the market, a lot priced in

A couple of key factors for the week ahead, overlaying the ongoing Iran backdrop. Both are tending to threaten to drive the dollar to break firmer, though much will also depend on the tone out of the ECB.

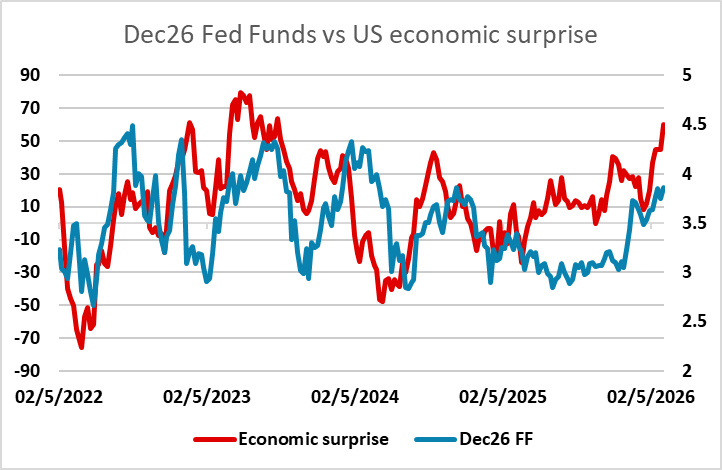

Despite all the reluctance to adjust before understanding how the reaction function at the Fed will look under new chair Warsh, the market is being gradually forced to extend its pricing of the Fed pivot, moving to more firmly skew the odds to a hike by year end.

The trend towards upside data surprises has been strong and compounded by a robust payrolls report on Friday (even granted local government and World Cup hospitality hires may have helped the latest month). With upward revisions, the underlying employment trend has moved further away from stall to solid growth territory while the unemployment rate remains on the tight side of neutral.

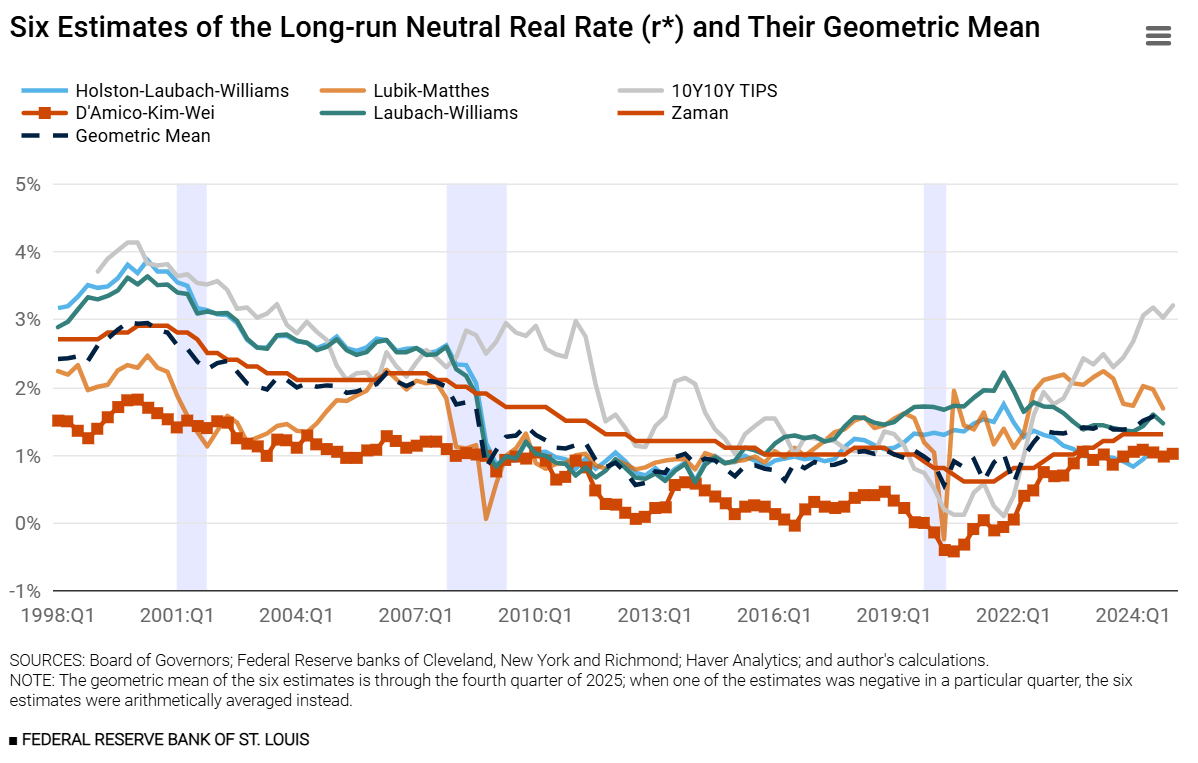

More than just the latest prints, there remains some background debate around whether the current Fed stance could be more accommodative than it seems. Recent short end real rates have been pushed negative on some measures. An ongoing high cyclical deficit together with ‘dot com’ like levels of non-residential investment also at least asks questions of whether the neutral rate, so called r*, is more like 2% and higher, rather than the low 1%s. Even more conventional statistical estimates tend to lean to the upside of the Fed SEP assumptions.

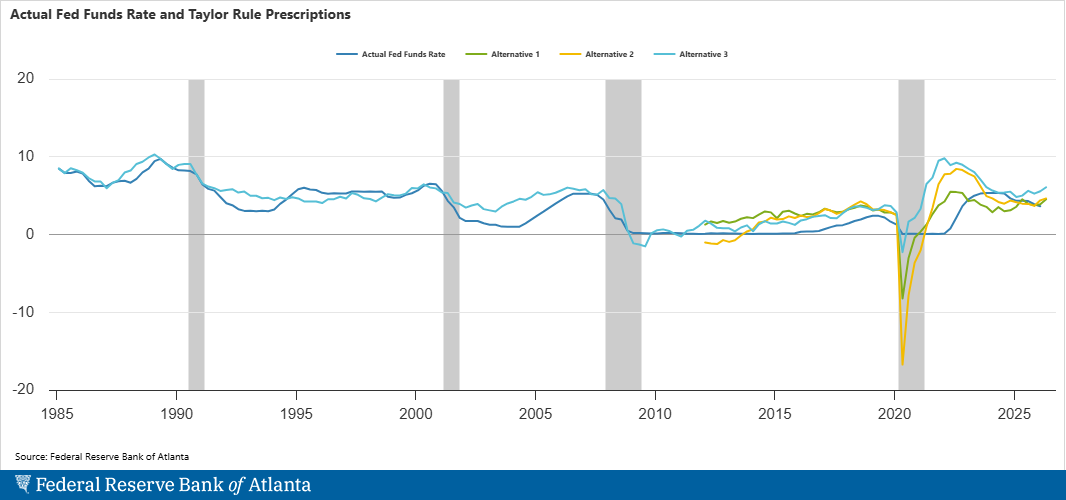

On top of that, most guestimates at the output gap, whether GDP or unemployment rate derived, are on the positive side of zero. With current inflation trends, most versions of any kind of Taylor rule would be saying the policy rate was easy. Iran clearly is a massive uncertainty in that equation of course.

Warsh’s input is another huge uncertainty. Switching to his favoured trimmed mean PCE (2.3%y/y) instead of core (3.3%) does substantially reduce the implied current spot-based inflation overshoot.

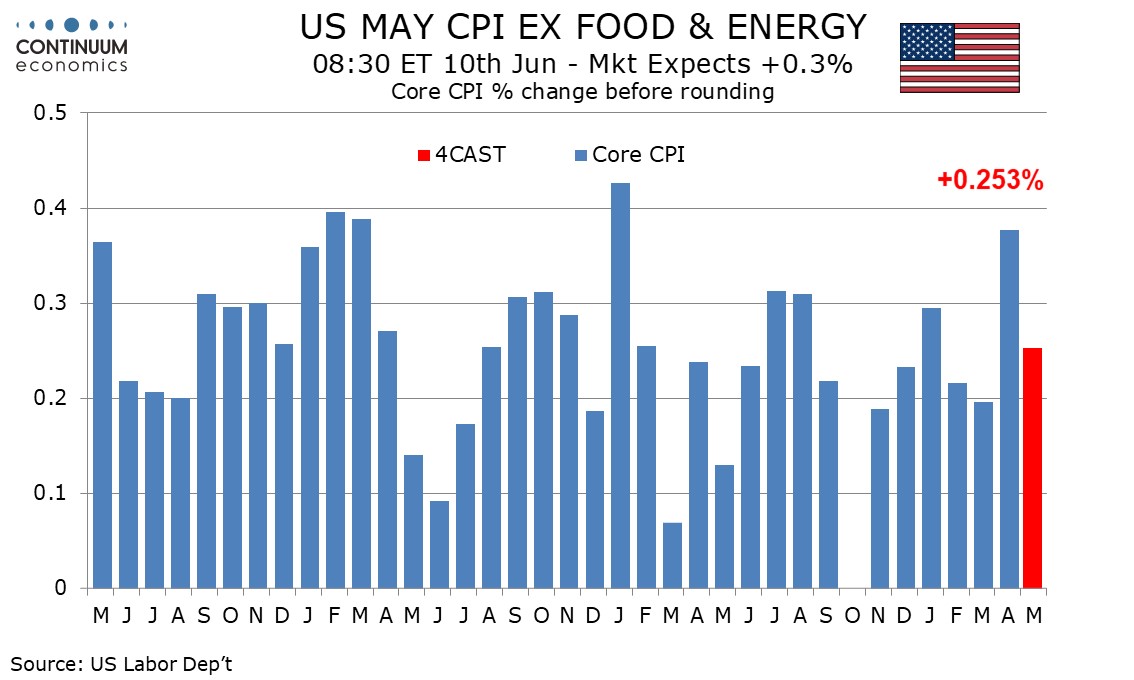

This week’s key data release in that context is May’s CPI. A 0.3% core would keep the direction of travel towards the hawkish side in terms of news flow.

While Fed pricing has been on the rise, and moving spreads in the dollars favour, the flip side of the coin this week is the ECB. Perhaps the key consideration here is the considerable amount the market already has priced in. The June hike is already nailed down as 100% certain, and a further full 25bp priced in by Sep, with a further full 25bp by early next year. Commentary and projections therefore have a lot to do to validate what is already in the curve and could therefore see ‘buy the fact’ as less hawkish if downside growth risks are more evident than second round inflation expectations.

Outside of this week’s central bank focus, if aggravate by the Fed shifts, there is also some attention on whether the loss of steam in tech stocks extends with the chip rotation seen towards the end of last week.

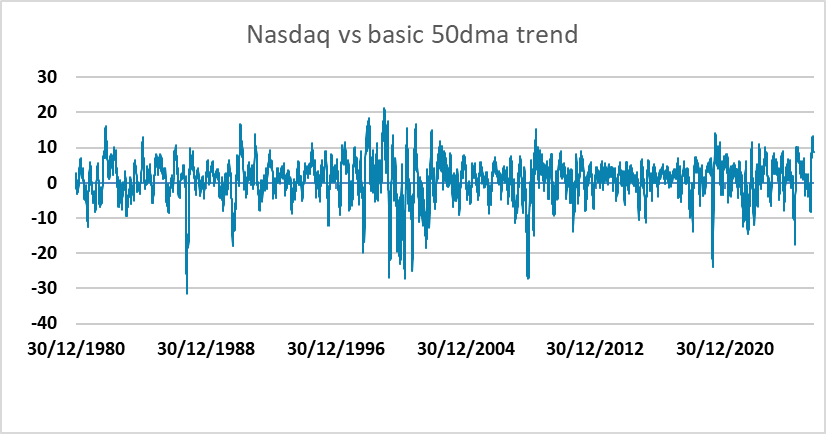

The Nasdaq for example had already looked like it was getting overstretched in terms of outrunning its 50dma trend, potentially playing to a corrective pullback, possibly another 5%+ if momentum does quickly turn. If this happens in a hurry and also spills in metals, that could also play to some further corrective action for the likes of the Aussie (AUD/JPY and AUD/JPY if volatility also picks up).

Technically, last week was ending, as of writing, with some technical range breaks looking like playing out in the dollar’s favour.

AUD/USD clean push through 0.71 figure floor was opening up .7055/.7000 as the next levels down and potentially even fuller retracing the rally from the .6833 March low.

EUR/USD similarly was giving up on 1.16~, managed the quick ½ point extension to 1.1550~ but likewise with some momentum at last could actually play out a fuller reversal of the rally from the 1.14-1.1450 base. Ranges and volatility have been so compressed for some time that when the breaks do come, they can move at a bit more speed and travel than the market has got accustomed to.

Data and events for the week ahead

USA

After a quiet Monday, Tuesday sees May’s NFIB small business optimism survey. April’s trade balance follows, where we expect a narrowing of the deficit to $55.5bn from $60.3bn. We also expect a 2.0% increase in May existing home sales to 4.10m.

The key release of the week is May’s CPI on Wednesday, where we expect a rise of 0.5% overall, and 0.3% ex food and energy, but with the latter only marginally above 0.25% before rounding. The extent of the feed through from energy to air fares may be determine whether core CPI rounds to 0.2% or 0.3%. May’s budget statement is also due on Wednesday.

On Thursday we expect May’s PPI to rise by 0.8% overall and 0.4% ex food and energy, still strong if less so than in April. Weekly initial claims are also due and may correct lower from a preceding rise in a week that included the Memorial Day holiday. Preliminary June Michigan CSI data is due on Friday and will be watched after a weak May outcome showed rising inflation expectations. Fed speakers will be quiet ahead of the June 17 decision.

CANADA

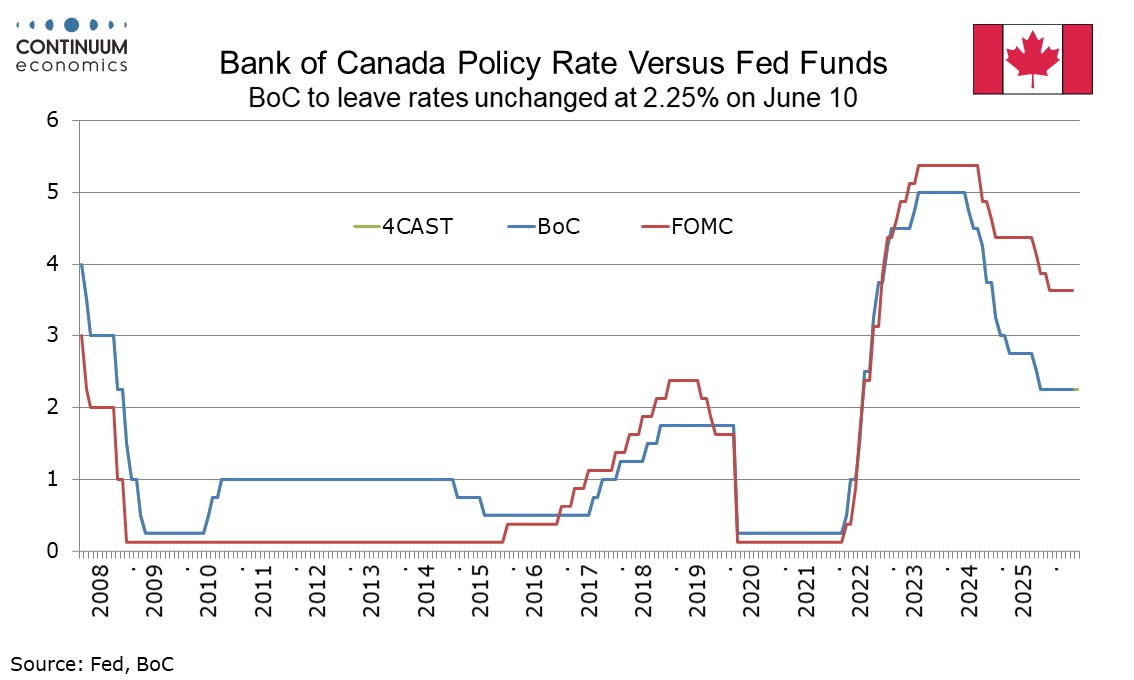

The Bank of Canada meets on Wednesday. Rates look set to be left unchanged at 2.25%. The improvement seen in the May employment report reduces the risk of the BoC taking a significantly more dovish turn at next week’s meeting, but is not enough to suggest a hawkish turn either. The approaching review of the USMCA trade agreement, cited by the BoC as a downside risk in April, remains a concern.

Canada also releases April’s trade balance on Tuesday and April building permits on Thursday.

UK

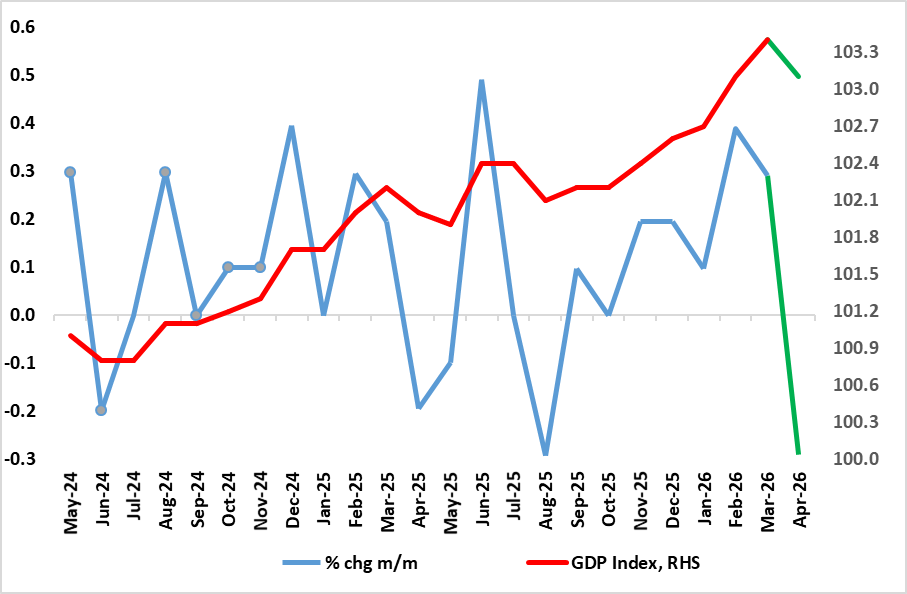

Becoming more important as it now covers war numbers, and given the upside surprises of late, April GDP data arrive on Friday. Indeed, providing yet more apparent signs of such economic resilience and, once again exceeding expectations, GDP grew by 0.3% m/m in March 2026, following growth of 0.4% in February. We think this is more an aberration than a better trend and partly a result of poor seasonal adjustments, meaning that we see April GDP falling back 0.3%, this chiming with both weak(er) business survey activity and employment signals and where what growth may actually have occurred likely to be short-lived boost in inventory building. Trade and construction data arrive alongside, while Thursday (evening) also sees what are likely to be more soft housing market survey data from RICS. The same day also sees BoE Agents survey data while Friday provides what may be important to some MPC members in the forms of household expectations.

Eurozone

Data wise sees German industrial production numbers data (Tue) preceded by order numbers (Mon) likely to see a second successive rise and this coming in the first month of the conflict, ECB wise the week is dominated by Thursday’s policy decision and forecast update. It is again the case that this next ECB Council meeting will be more important for what is said than what is done. In fact, a 25 bp official rate hike is virtually nailed on irrespective of how events in the Middle East may fare in coming days. But the ECB comments and updates projections will give clear signs as to how fast and further, the Council consider policy rates may have to rise. We think that the looming 25 bp hike is more than enough and that this misplaced move will be more than reversed into 2027. But the projections are likely to show HICP inflation back in line with target through 2028, this though largely validating the market view of up to three 25 bp hikes that the outlook will be based on. But the projections will also show an even weaker GDP picture, albeit probably still above our below consensus outlook

Rest of Western Europe

Sweden sees details of what turned out to be less friendly but still soft CPI data this time for May (Thu) and they may have featured in this month’s Riksbank decision. There is also monthly GDP for April, the March numbers having jumped surprisingly and sizably. Otherwise, Tuesday sees business survey data from the Riksbank. In Norway, Wednesday sees May CPI data (Wed) where we see the CPI-ATE measure staying around 3.2%-3.3%, in line with Board thinking but where the Norges Bank Regional Survey (Thu) may be as important.

The Swiss referendum vote on ‘cap the population at 10 million’ is on the 14th so on the radar into the close of the week. Latest polls have nudged toward no (52%, yes 45%) from tied, but still within the margins of error and swing.

Japan

Kickstarting with GDP on Monday. There is little expectation that it will be a major revision. With the household spending number less bad than expected, we might even see a slight revision higher. Else, there are only tier two data for the week.

Australia

A rather empty calendar for Australia next week. The most important data release will likely be consumer confidence on Wednesday and consumer inflation expectations on Thursday.

New Zealand

Only Business PMI on Friday.