This week's five highlights

Geopolitical Tension Persists

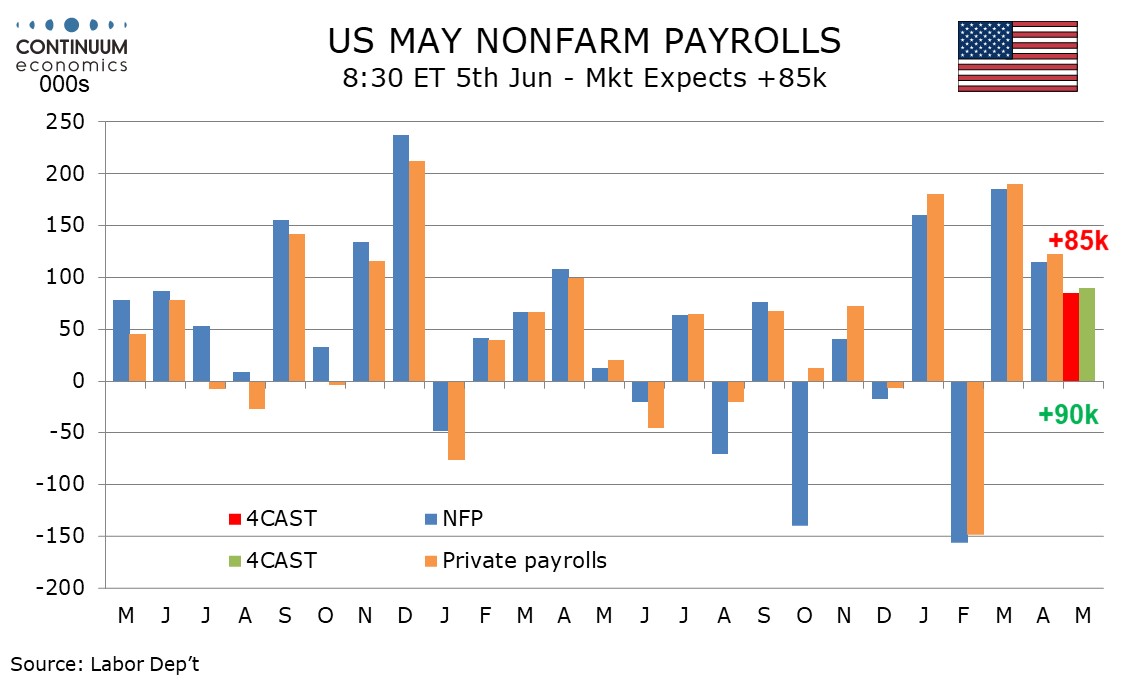

U.S. May Non-Farm Payrolls still healthy

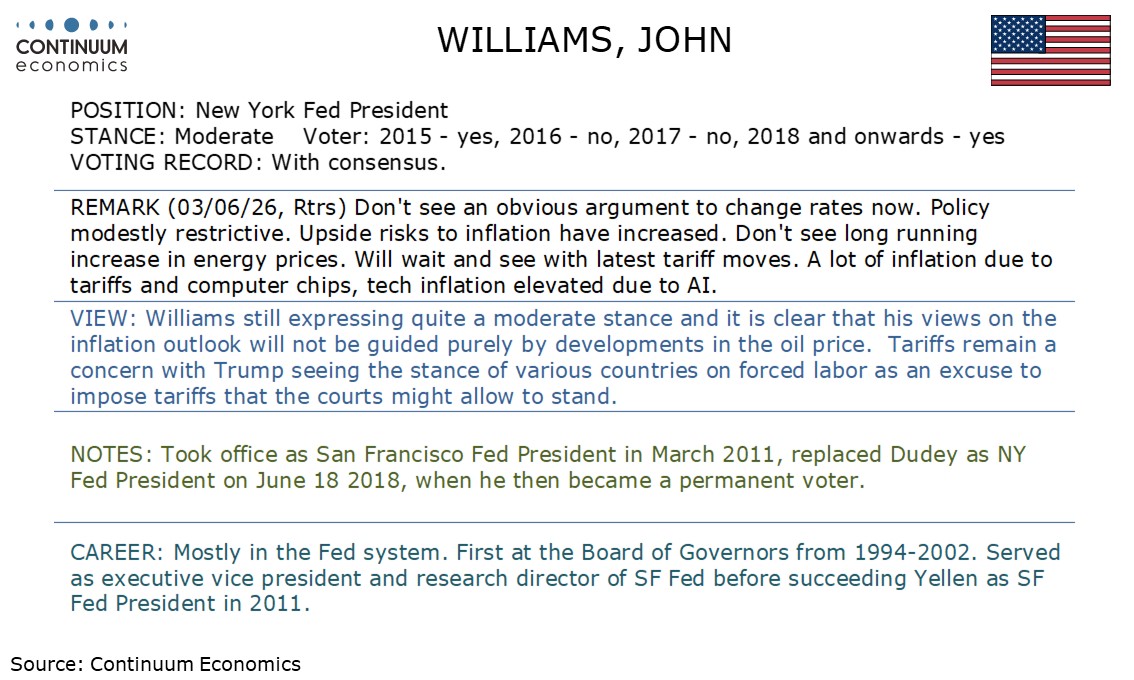

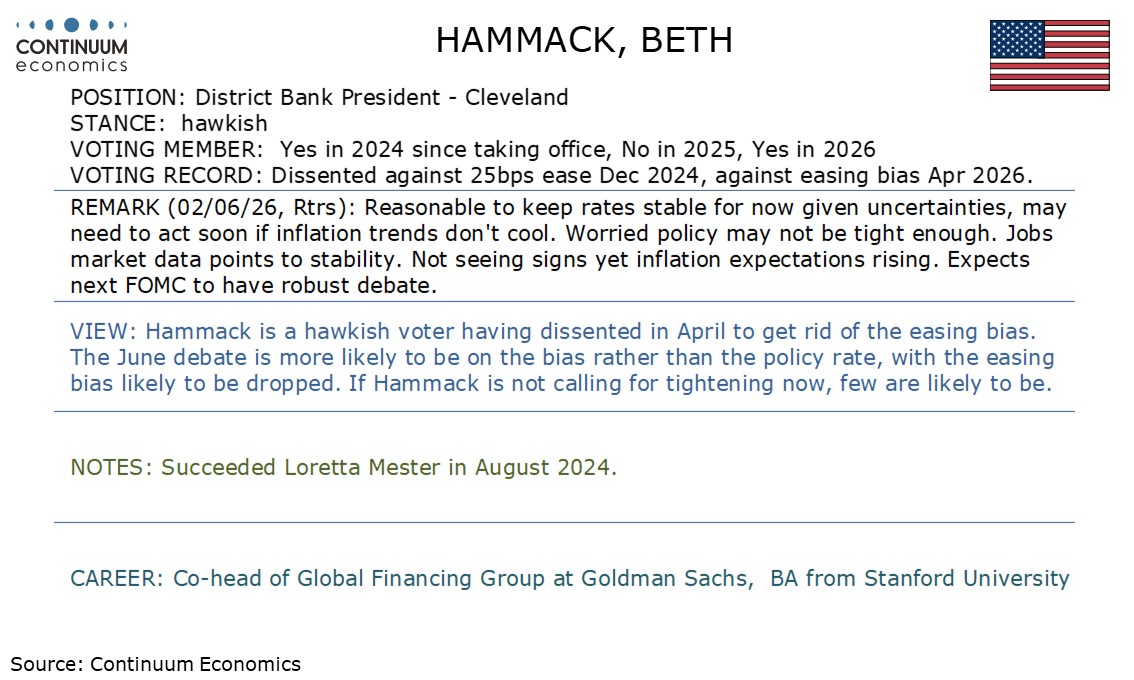

This Week's Fed Speakers

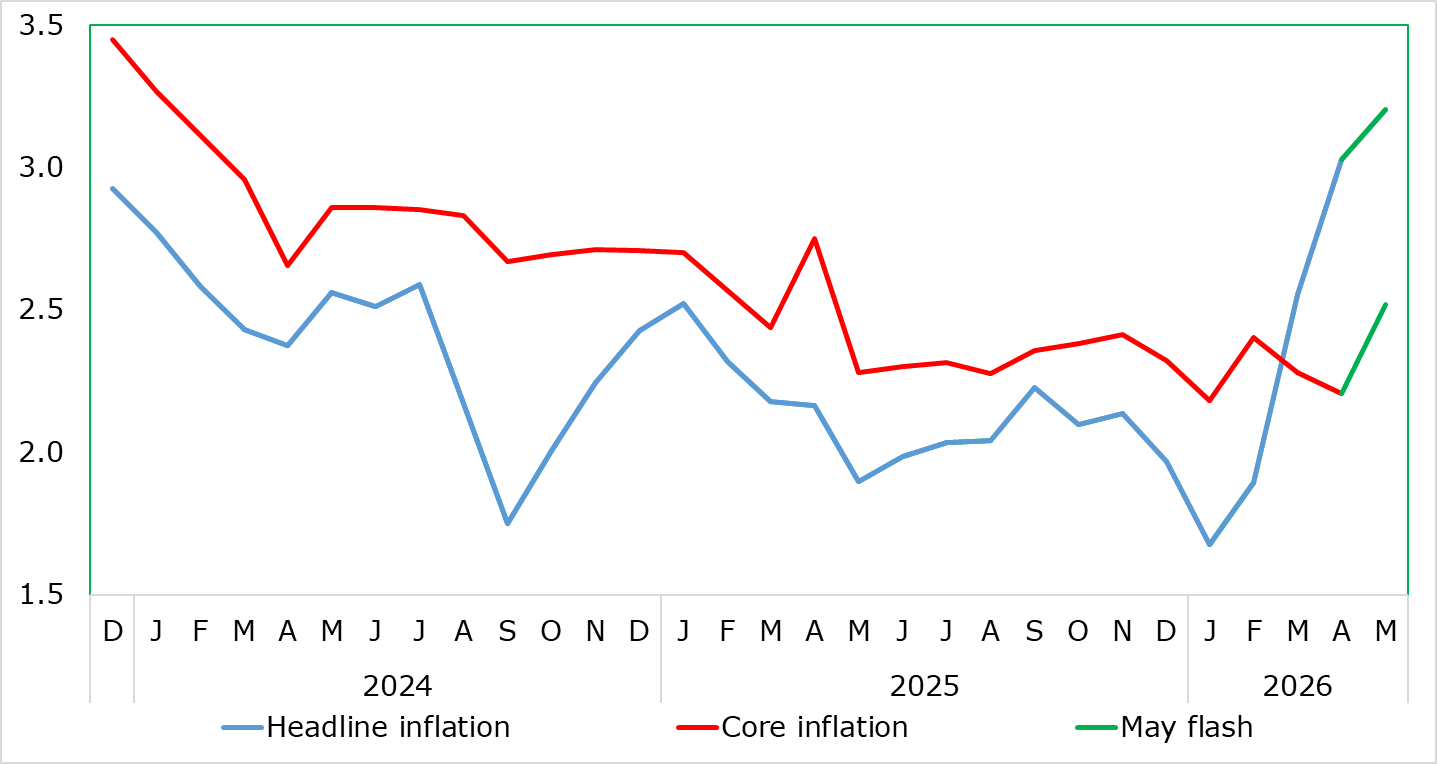

EZ Headline HICP Rise Capped by Food & Energy

More Controlled Yuan Appreciation

Geopolitical tension persist in the Middle East as we see little concrete progress being made. Both sides are sending conflicting rhetoric with U.S.'s Trump barraging the headline with a deal is close while Iranian keep denying and launching rockets. It is very hard to tell where it is heading and market participants are clearly aware of such. The equity market has shown cracks in endless hopium and will likely rotate lower to end the week.

We expect May’s non-farm payroll to rise by 85k overall and by 90k in the private sector, less strong than in March and April but still showing a healthy labor market given a lack of growth in the labor force, leaving unemployment at 4.3% for a third straight month. We expect a 0.3% rise in in average hourly earnings, slightly firmer than two preceding gains of 0.2%. A rise of 85k would still be stronger than April’s 3-month average of 48k and its 6-month average of 55k. For the private sector the 3-month average is 55k and the 6-month average 68k, with trend in government getting less negative now that the DOGE cuts are done.

Figure: Headline Higher Again And Core Up Modestly Too

Even given what seem to be a series of reassuring aspects, the May flash HICP data is unlikely to have a material impact on ECB thinking. As expected, and helped by German fuel subsides which kept the energy rise to around zero, headline HICP rose just 0.2 ppt to 3.2%, still a 32-mth high, but where softer food prices and stable non-energy goods helped temper what were higher services inflation (up 0.5 ppt to a six-mth high of 3.5%). This latter increase is obviously unwelcome and will reverberate among the ECB hawks whose talons now dominate the Council to a degree where a rate hike this month is all but sealed. But we think that the services jump is partly seasonal (Pentecost holiday was early this year and is normally associated with steep airfare rises). Moreover, the headline may now be close to having peaked, not least as a marled fall in diesel prices in late May could take 0.2 ppt of the y/y rate in June.

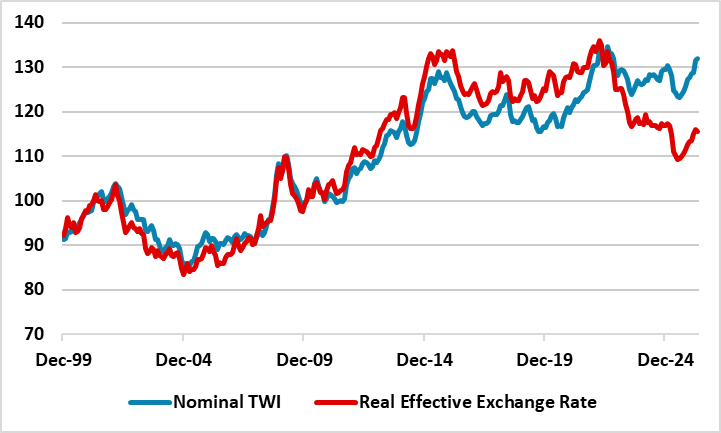

Figure: Yuan Nominal Trade Weight Exchange Rate and Real Effective Exchange Rate (Index)

The Yuan has been appreciating driven by a large trade surplus; the ongoing trade truce with the U.S. after Trump May visit and official acceptance of Yuan gains. Even so, we feel that China’s authorities will pause appreciation at times via FX intervention to stop the move becoming too fast, but then allow appreciation to restart. A reopening of the Straits of Hormuz would make the authorities more willing to accept appreciation. We now see further Yuan appreciation to 6.65 by end 2026, though the authorities will be reluctant to see much more.

China authorities are allowing a slow controlled appreciation of the Yuan. The Iran war has so far not hurt China economy, with coal/renewables playing a bigger part in electricity production. Additionally, monthly trade numbers also show that exports are still performing well, both due to Chinese companies keenness to export but also as the real value of the Yuan has fallen since 2021 with overseas inflation outstripping inflation in China (Figure 1). The current account surplus will likely be around 3.5% of GDP in 2026 and this will keep the Yuan firm. The May 2025 Xi-Trump summit has also reinforced the sense that tariffs threats are now under control and China/U.S. trade truce can hold. Nevertheless, China authorities need to see when the Straits of Hormuz is reopened, as a prolonged closure into Q4 could hurt global trade and China export prospects. We feel that the authorities will pause appreciation at times via FX intervention, but then allow appreciation to restart. A reopening of the Straits of Hormuz would make the authorities more willing to accept appreciation. This willingness to allow slow appreciation also appears to be linked by official desire to increase long-term usage of the Yuan. President Xi Jinping's 2024 speech also noted that the yuan should be widely used in global trade, investment, FX markets, and more importantly, have the status of a global reserve currency. We now see further Yuan appreciation to 6.65 by end 2026, though the authorities will be reluctant to see much more. Additionally, the 2yr spread between the U.S. and China also argues for slow further appreciation.