FX Daily Strategy: N America, Jun 30th

Still in dollar consolidation/correction mode. Period end, options, wait for payrolls also

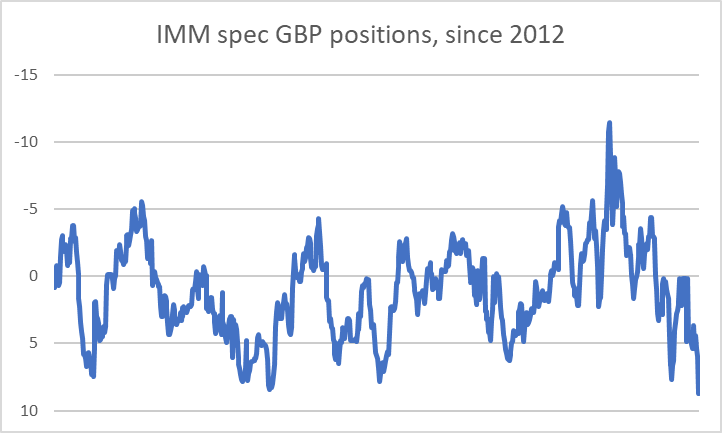

Spec mkt long dollars and at extreme for GBP. Latter could risk a squeeze

Markets threatening to be a bit sidelined for by the usual wait on payrolls Thursday, a decent chunk of options at and around the current vicinity (i.e. EUR/USD 1.14 +/-), period end a consideration, and a slight standoff as overbought dollar conditions attempt to unwind.

On the latter front though, it was notable to see just how large and broad dollar long positioning now is on the latest spec data.

This was particularly stark for sterling, up at new extremes for the last decade. While the back testing on this is mixed, it does highlight the clear, albeit not guaranteed, risk of a bit of a short squeeze for sterling at some point in the next few weeks.

There is some potential logic for this, be it ‘buy the fact’ on Burnham, or just the dangers of people running stops if EUR/GBP is forced to take out the range floor that has been in place for some time for instance. Burnham’s big set piece speech focused on devolution and council house building as largely expected and gave a nod to keeping to the fiscal rules (even if its not particularly clear how regional/local growth boosting spending gets covered on this vision).

Even a false break could flush out shorts even if later recouped. UK economic news is hardly bright – the latest batch of credit and housing finance figures were soft and consistent with no hikes – but positioning might be the more important near-term consideration

Near-term, the weakest side is probably further dollar leakage as it sees the consolidative correction complete. Cable has up to 1.33 if the modest bounce extends, while EUR/USD has 1.1450 as the next level up as the oversold recovery stretches further. That said, any drift is proving reluctant to date and at the moment it's proving more of a 'time correction' than any significant backfilling.

USD/JPY meanwhile does indeed look to be getting the suspected boost into the quarter-end with relative equity performance a factor, MoF reiterated rather than escalated the jawboning and the question remains how they play it from here: hoping the market is self policing, or in any case wary of intervening against the grain of the dollar; or drawn in to attempt to avoid the new 40 years highs propelling further breakout activity. Some tactical appearance seems likely at some point, but maybe not until the market is viewed as more extended and at maximum spec yen short?

On the calendar from here, the US sees June consumer confidence as well as April house price data from S& P Case-Shiller and FHFA. Canada releases April GDP. We expect a 0.3% increase, slightly below a 0.4% estimate made with March data.