FX Daily Strategy: Asia, March 18th

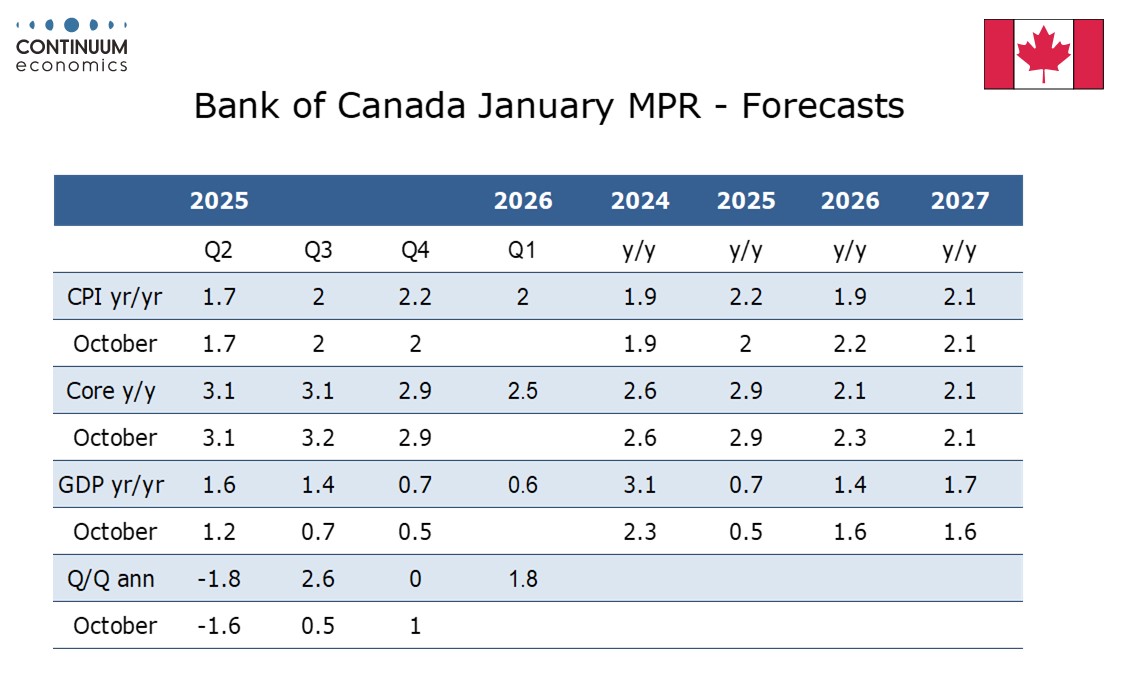

Bank of Canada No change in rates or from January's message

USD/CAD Downside remain limited

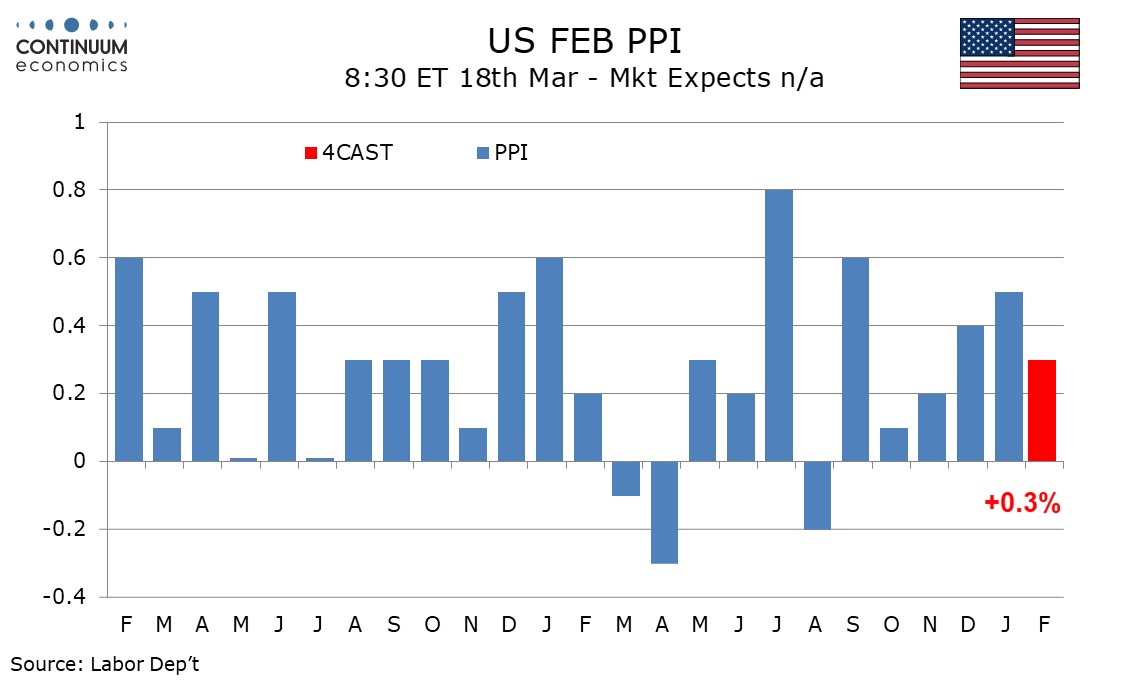

U.S. February PPI Ex food, energy and trade suggests trend at 0.3%

The Bank of Canada meets on March 18 and looks highly likely to leave rates unchanged at 2.25%. The statement is likely to reiterate the message given at the last meeting on January 28, that the policy rate is appropriate conditional on the economy evolving in line with expectations, but uncertainty is heightened and if the outlook changes the BoC is prepared to respond. This meeting will not see a quarterly Monetary Policy Report so the forecasts made with the last MPR on January 28 will not be updated. Since the last meeting Q4 Canadian GDP came in weaker than expected at -0.6% annualized, but with domestic demand up by 2.4%, albeit with significant support from government stimulus, the data is unlikely to change the BoC outlook significantly. Underlying inflation appears to be slowing though strength in oil prices is likely to mean Q1 CPI comes in a little stronger than the 2.0% projected by the BoC in January.

Canada’s economy will be more resilient overall than most to any sustained boost to oil prices, though outside the oil-rich province of Alberta the economy would be likely to weaken. The extra near term inflationary risk reduces what were already quite slim chances of a BoC easing, while tightening still looks some way off. Minutes from the last meeting show that Iran was one of a number of risks discussed, including Venezuela and Greenland, where risks have faded since January. Other risks discussed were threats to the independence of the Federal Reserve, and the upcoming review of the Canada-US-Mexico trade agreement, which persist. The US Supreme Court ruling against some of Trump’s tariffs is a positive development, but uncertainty overall has increased since January, due to the Middle East situation.

The test of resistance within congestion around 1.3700 and the 1.3725 monthly high of 6 February has given way to a pullback, as intraday studies turn down, with prices reaching congestion support at 1.3650. A test beneath here cannot be ruled out. But rising daily readings and improving weekly charts should limit any break in renewed buying interest above further congestion around 1.3600. Meanwhile, resistance remains at 1.3700/25. However, a close above the 1.3755 Fibonacci retracement is needed to turn sentiment positive and extend late-January gains towards 1.3800/20.

We expect PPI to rise by 0.3% in February, slower than January’s 0.5% and December’s 0.4%. Ex food and energy we expect a rise of 0.2% after a strong 0.8% January increase. Ex food, energy and trade however, we expect a fourth straight increase of 0.3%, which would signal where trend is. We expect food and energy to see partial corrections from respective January declines of 1.5% and 2.7%. Energy looks set to see a stronger increase in March. Food trend has turned negative in recent months, but bad weather poses some upside risk after January’s decline.

Recent data ex food, energy and trade suggests an underlying trend of 0.3% per month, and that is consistent with inflation remaining above the Fed’s target. Trade prices look set for a correction lower after two straight strong gains that more than fully erased two straight declines. We expect a 0.2% rise in services restrained by trade and a 0.3% rise in goods ex food and energy, the latter slowing from a 0.7% January increase that probably reflected new year pricing decisions. Despite the slower monthly gains, we expect yr/yr growth to pick up to 3.0% from 2.9% overall and to 3.7% from 3.6% ex food and energy. Ex food, energy and trade however, we expect a slowing to 3.2% from 3.4%.