FX Daily Strategy: Asia, Jun 10th

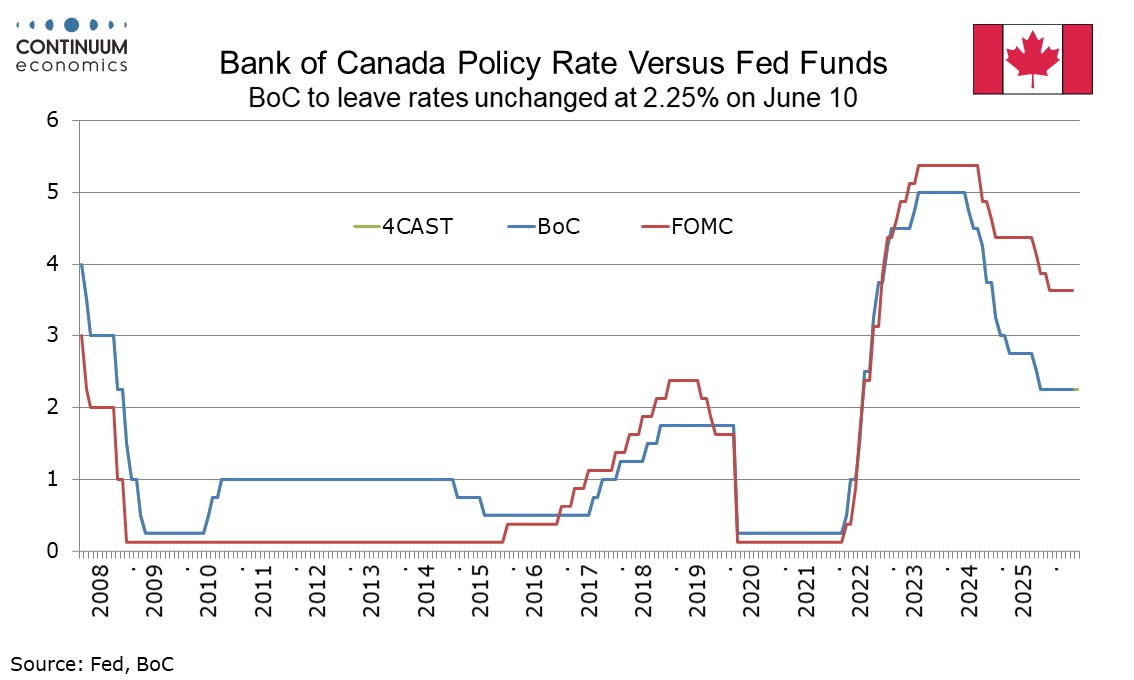

Bank of Canada A little less hawkish

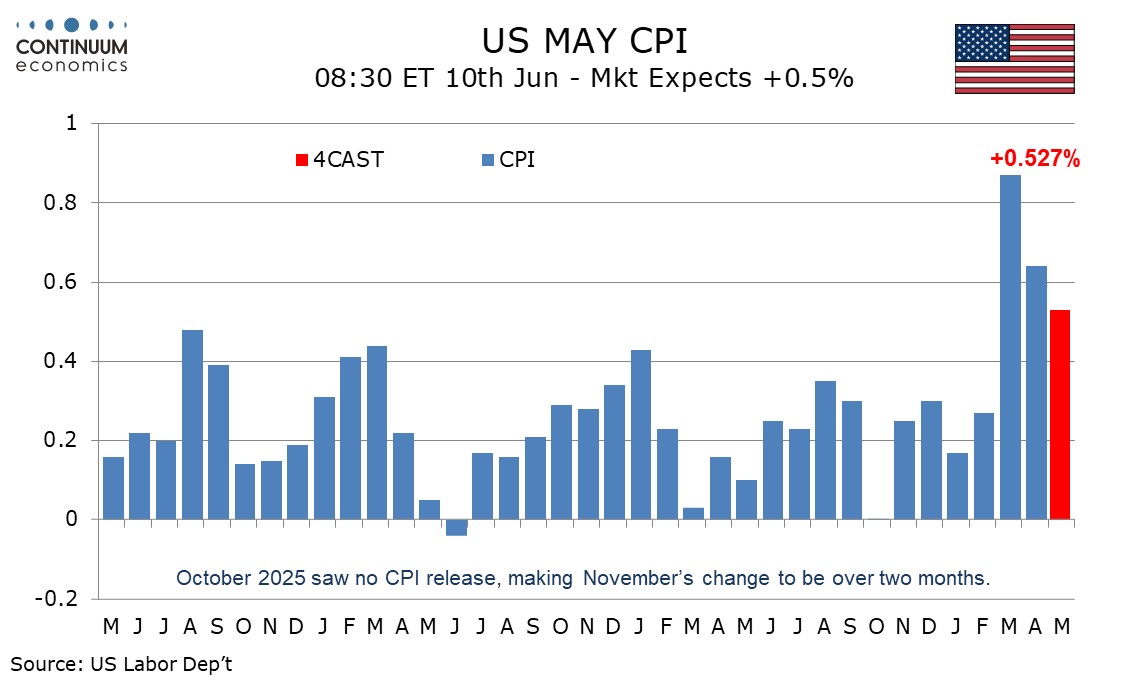

U.S. May Energy and air fares CPI to lead

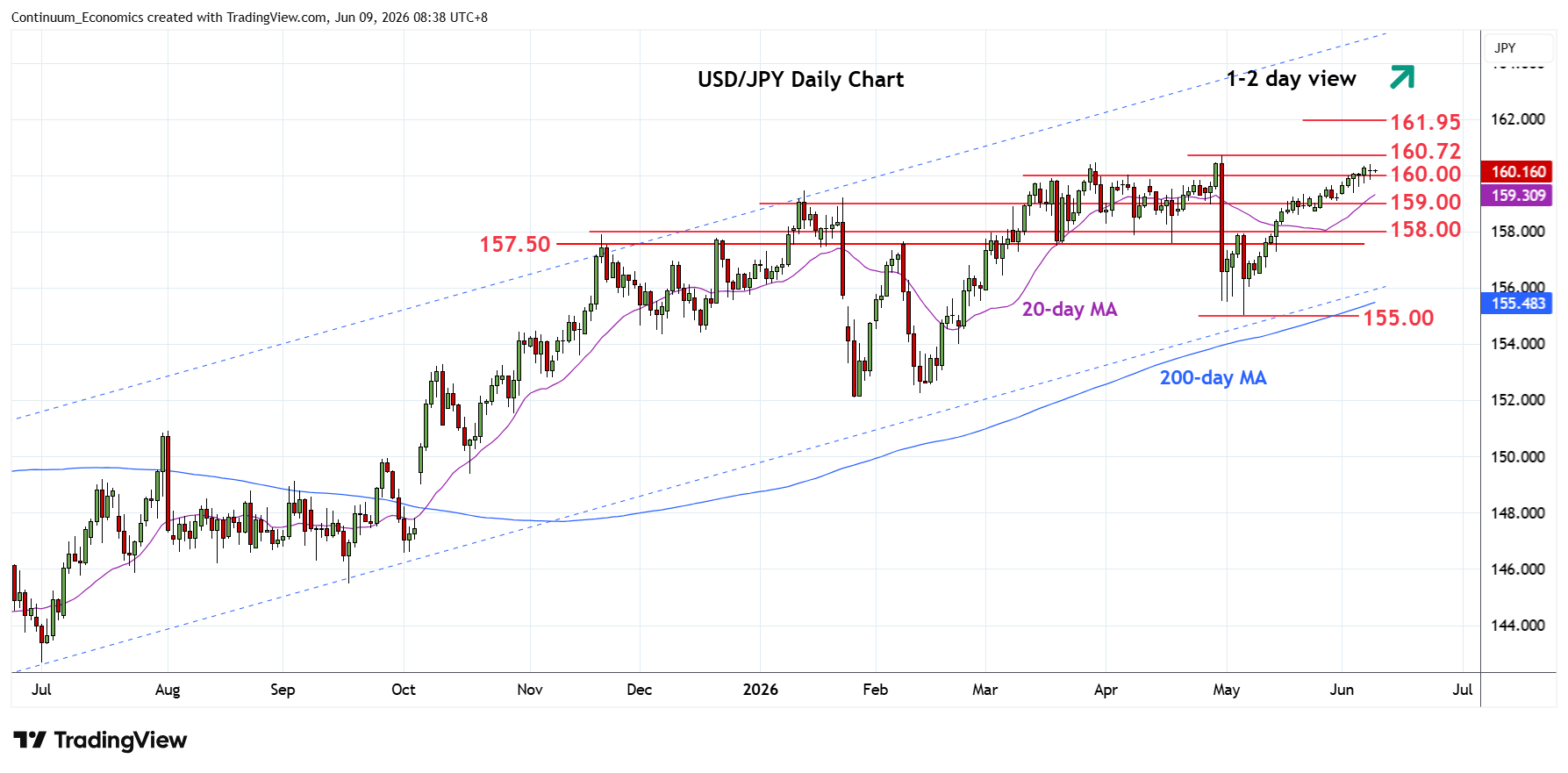

Is BoJ's Intervention Imminent

The Bank of Canada meets on June 10 and looks set to leave rates unchanged at 2.25%. This meeting will contain no quarterly Monetary Policy Report and hence no updated forecasts. However, since the last meeting on April 29 GDP and core inflation have come in softer than expected, but elevated energy prices look likely to be more persistent than the BoC assumed in April. On balance we expect a slightly less hawkish tone, which could reduce the perceived risk of a tightening later this year.

On April 29 the Bank of Canada agreed to look through the immediate impact of the war in the Middle East on inflation. Governor Tiff Macklem however stated that they are committed to not allowing persistent inflation to develop and if that happened there may need to be consecutive increases in the policy rate. The BoC assumed oil prices declining to around $75 by the middle of next year with CPI peaking around 3.0% in April and easing back to the 2.0% target by the middle of next year. The BoC stated that if the economy evolves in line with its forecasts, policy changes are likely to be small. Minutes from the meeting however showed that if oil prices were to remain elevated for a prolonged period the risk of broader and more persistent inflation would increase.

We expect May CPI to increase by 0.5% overall and 0.3% ex food and energy, with respective gains before rounding being 0.527% and 0.253%, meaning that the core rate is a close call between 0.2% and 0.3% before rounding. The extent of the energy feed through to air fares may be the swing factor in the core rate. April’s 0.4% core rate (0.376% before rounding) following two straight gains of 0.2% was inflated by a distortion caused by October’s CPI not having been measured due to the government shutdown. Some components of housing are updated only every six months, leaving the April data catching October’s changes as well. Housing CPI rose by 0.7% in April after two straight gains of 0.3% while owners’ equivalent rent rose by 0.5% after rising by 0.3% in March and 0.2% in February. Housing got an extra boost from a 2.4% rise in the volatile lodging away from home sector which may correct in May. We expect gains of 0.3% in housing and owners’ equivalent rent in May.

USD/JPY has broken through 160 and stay above the level. The major catalyst remain haven USD buying on geopolitical tension. Market confidence erosion led JPY losses seems to have lost traction as JGB yields moderate. With the current pace of rally, it maybe hard for the BoJ to justify an imminent intervention. Their last intervention attempt did stall the weakness for a month but fundamental drivers are needed to keep JPY from further weakening. The potential June hike maybe their grace and keep them from intervening now.

On the chart, the pair is still stretching as prices extend gains above the 160.00 figure to approach the 160.46 resistance. Bullish gains from the 155.00 May low keep pressure on the upside and see scope for extension to retest the 160.46 March high then the 160.72 April current year high. However, would expect these to cap and give way to fresh selling pressure later. Break, if seen, will turn focus to the 161.95, July 2024 year high. Meanwhile, support at the 159.35/159.00 congestion area underpin. Would take break here and then 158.60 low of 18 May to fade the upside pressure and open up room for deeper pullback to retrace gains from 155.00 low.