FX Daily Strategy: Asia, May 21st

Eying risk and bonds out of Nvidia, auction and Minutes

Big picture, have some seen re-pricings within established ranges (EUR/USD 1.15-1.20 give or take)

Need to see more decisive developments on Iran and/or asset volatility to be making new strides

Global PMI data in focus

A certain amount of rebalancing has been seen over the last week or so. Step back from the noise and EUR/USD has been 1.15-1.20 give or take since last summer. Having become a little too comfort light on dollar again, the market has now worked back down in that range. Maybe the easiest part of that adjustment has been seen now, as far as relative macro and central bank re-pricing is concerned, though there is a little more downside through the 50 pip level down from 1.16 to 1.15 as and when the market has consolidated its slightly oversold correction.

FOMC Minutes, the auction result, and the Nvidia earnings will have come out overnight and set the immediate backdrop into today’s sessions - with a particular focus on where US bonds and equities ended up - but broader stories are likely to remain the same.

For any major escalation out of this broader range pattern, be it 1.15 base on EUR/USD or circa 100~ on DXY, then this is likely to need something a little more disorderly and a more notable escalation in what is still compressed cross market volatility.

MOVE has shown a bit of life on the bond side this week, but yet to the point of leading VIX higher, and we really need to see a scenario where higher yields and/or overstretched sectoral gains of recent weeks see something closer to rapid profit-taking and position culling. Or, of course, something that goes beyond verbal noise on Iran.

USD/JPY remains its own story, still in that stairs-elevator mode, and tending to grind its ways on either dollar or risk leadership whichever is winning day to day.

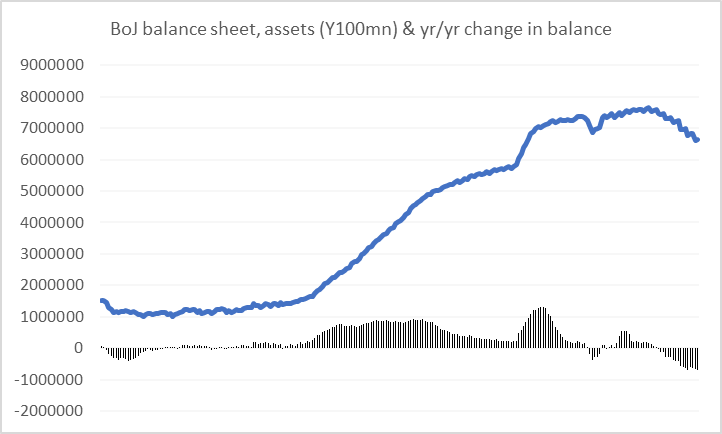

We discussed elsewhere how the BoJ could, if it decided to be more daring than is its norm, see to try and short-circuit some of the recent dynamics. This would be a riff on the idea of ‘Operation Twist’. Rather than selling short and buying long, this version would raise the policy rate (and more than expected) while significantly slowing its aggressive balance sheet taper. There’s even a case for the BoJ to catch the market flat footed by hiking by 50bp as well as laying out a more aggressive taper. That is probably too radical for the conservative Bank, but a more sedate version would be a more measured trend of upside surprise to the trajectory over coming months. This also has the advantage of being in tune with US Treasury Secretary Bessant’s insistence that policy needs to back up action and be unconstrained and would thus be seen to cement US appeasement with intervention as needed.

All the above is not immediately pressing but worth keeping an eye on into June as an unexpected shift that could change some of the backdrop to the yen narrative.

Sterling also seems to have somewhat exhausted some of its recent idiosyncratic momentum. Soft data this week, and BoE TSC testimony, have all tended to go with the grain of our view that the market was being overly-aggressive and pre-emptive in its summer hike risk pricing.

Politics is likewise in a hiatus as we wait out the by-election, though Burnham’s odds of winning and eventual leadership have been firming up further in the betting markets. His reported support for the fiscal rules have taken a bit of the sting out of things too, even if we can expect the rhetoric to become more populist focused during campaigning.

EUR/GBP is still largely a 1 figure or so range trade at present, drifting back towards the low side, with ½ figure stretches at the extremes.

In terms of today’s calendar, Japan has PMI and machinery orders data, while Australia’s focus will be on the employment data. External backdrops on Iran, tech/metals risk performance, positioning, and the dollar tone however remain the dominant influences here.

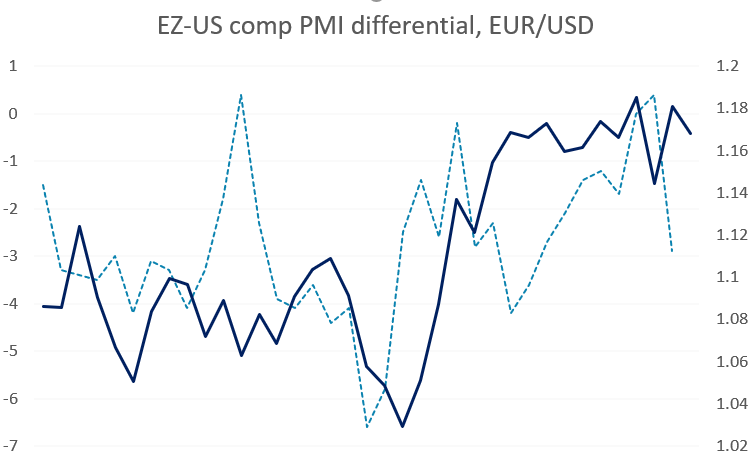

Europe and US also see the main focal point being the respective PMI data. This is expected to continue to highlight a theme of US relative strength, one that is broadly thematically consistent with the Europe/USD pullback if that now somewhat better reflected in the spread adjustments of recent days.

On the US side, we expect a correction lower in May’s S and P manufacturing PMI to a still firm 53.5 from 54.5, but an unchanged S and P services PMI at a still subdued 51.0.

The US also has Philly Fed, housing starts and initial claims data to complete the picture.