FX Daily Strategy: Asia, Jul 10

Empty Calendar Sees Geopolitics in Driver Seat

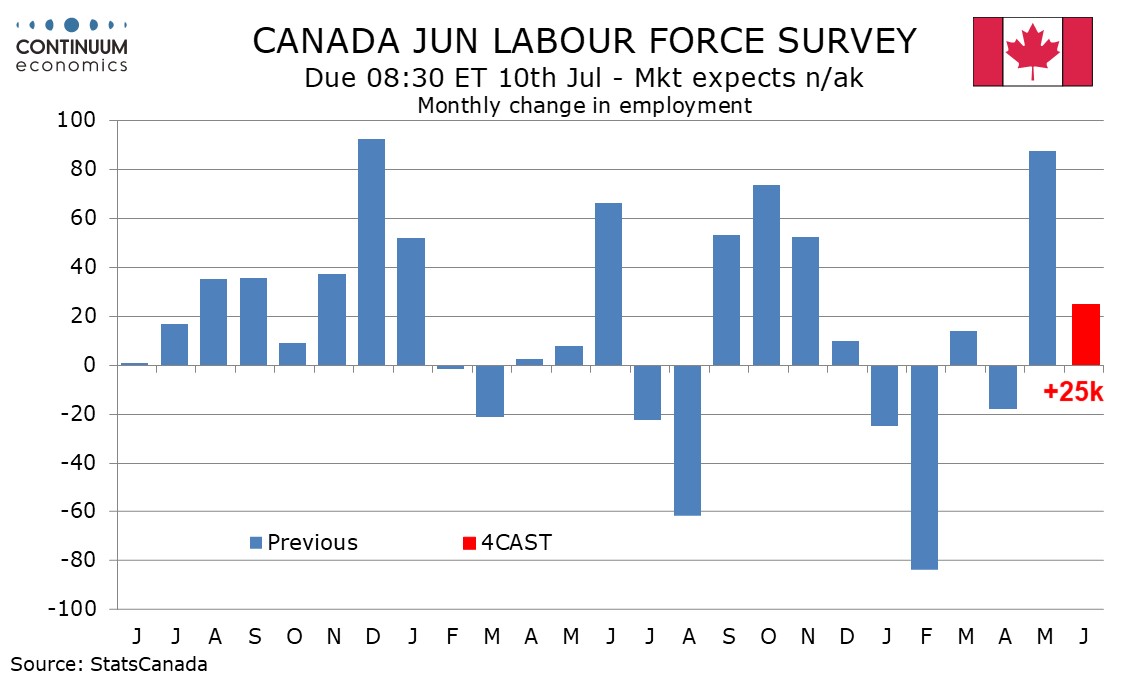

World Cup to help sustain bounce in Canada Employment

But the Loonie Still Chopping

Figure: Iran/Iraq Tanker War 1987-88

| Incident | Comments | |

| USS Stark | May 17 1987 Iraq aircraft attacks USS Stark by mistake | 29 U.S. servicemen killed. Ship has severe list, but avoided sinking and sails to Bahrain. Iraq apologises as they thought it was an Iranian ship. |

| Bridgeton oil tanker | July 24 1987 oil tanker hit by Iran contact mine | Modest damage to huge tanker, but U.S. Navy ships had to follow Bridgeton into Kuwait due to risk of other mines. |

| USS Samuel Roberts | April 18 1988 Iran contact mine hits US frigate | 10 U.S. serviceman injured. Ship keel snapped, but did not sink due to emergency repair work. U.S. launches retaliation attack on Iranian gulf oil platforms 4 days later. |

Source: US Navy/Continuum Economics

With Iran choking the Strait of Hormuz again, how can the U.S. keep oil flowing will be a big question for Trump. Our baseline scenario do not see a full scale invasion from the U.S. to Iran. Apart from their current strategy of neutralizing Iran's capability of holding the Strait hostage, Trump may further instruct the U.S. navy to directly escort tankers through, though the cost maybe heavy.

During the Iran/Iraq war, the U.S. navy with the help of a number of other countries helped to escort tankers through the Straits of Hormuz. This was a difficult experience with Iraq mistaking the USS Stark for an Iran ship and the USS Samuel Roberts nearly sunk due to an Iran contact mine. Iran asymmetric warfare through the Gulf of Hormuz has increased in strength since 1987/88, with drones able to launch from inland against ships through the Straits of Hormuz plus sea boats operating in the Straits. The U.S. minesweeping capabilities is in transition with 4 older minesweepers in Japan and 3 new littoral assault ships with minesweeping capabilities. Additionally, it took 7 months to get the U.S. navy in place to start the escorts in 1987. It could thus be difficult for the U.S. acting alone to quickly force a reopening of the Straits of Hormuz without some Iranian cooperation.

We expect Canadian employment to increase by 25k in June, extending on a strong 87.8k increase in May with the World Cup likely to provide some support. We expect unemployment to slip to 6.5% from 6.6%, reaching its lowest level since January. May’s strong increase was probably largely corrective from preceding weakness, most notably in February, with the 6-month average remaining marginally negative. Without the World Cup, which is likely to boost employment in the Toronto and Vancouver areas, we would have expected a subdued June report.

May’s breakdown contained some hints of support from the World Cup, with employment gains of 41.8k in Ontario, which includes Toronto, and 25.2k in British Columbia, which includes Vancouver. By industry the detail was less convincing. Gains of 19.3k in information, culture and recreation, and 17.0k in accommodation and food services, may have been supported by the World Cup. However, gains of 26.8k in construction and 14.7k in manufacturing look difficult to sustain, as does a rise of 20.4k in the public sector. Less suggestive of a World Cup factor in May was surge of 154k in full time jobs, while part time work, which the World Cup would be likely to boost, fell by 66.2k. This corrected from three straight months in which part time jobs rose while full time jobs slipped. We expect June to see full time jobs seeing renewed slippage, by 25k, while part time work increases by 50k. We also expect June’s gain to be led by a 30k rise in the private sector, with the public sector correcting lower by 5k.

On the chart, the pair is little changed as mixed/negative intraday studies keep near-term sentiment cautious and extend choppy trade beneath congestion resistance at 1.4200. Daily readings are also under pressure, highlighting room for a pullback towards support at the 1.4140 monthly high of 5 November. But positive weekly charts should limit any deeper losses in renewed buying interest towards congestion around 1.4100. A close beneath here, if seen, would turn sentiment negative and signal a deeper retracement towards 1.4000. Meanwhile, a close above resistance at the 1.4248 current year high of 24 June will turn sentiment positive and extend January gains towards the 1.4290 Fibonacci retracement.