FX Daily Strategy: Asia, Jun 2nd

Breakdown over Lebanon a concern unless it's quickly neutralised

Has potential to escalate unless US intervenes

Mkt remains a binary trade driven by dollar haven swings

Developments were not particularly looking fruitful anyway, but Israel continues to act as the worrying spoiler, deliberate or otherwise.

As the price action attests, this and Iran’s response is the much bigger concern than the noise of background military skirmishes. Fresh action seen in Lebanon clearly cannot be seen as consistent with a ceasefire so it remains highly problematic unless it draws a response from Trump. The Iran threat to completely close down the limited Strait access but also to extend to other fronts including the Bab al Mandeb Strait marks a clear escalation and one that could trigger more significant fresh military confrontations and up the ante further for commodity bottlenecks. The market would be incredibly sensitive to news headlines on the latter.

The upshot is that unless we hear from Trump something along the lines of his April comments that ‘Israel will do what he tells them’, or past expletive-filled rebukes then the situation remains a powder keg.

That unfortunately remains the start and the end of the market’s focus for now and very little in the way of other news or themes will make much of a dent until there is fresh clarity on the latest flare up. FX action will similarly remain very binary across the board.

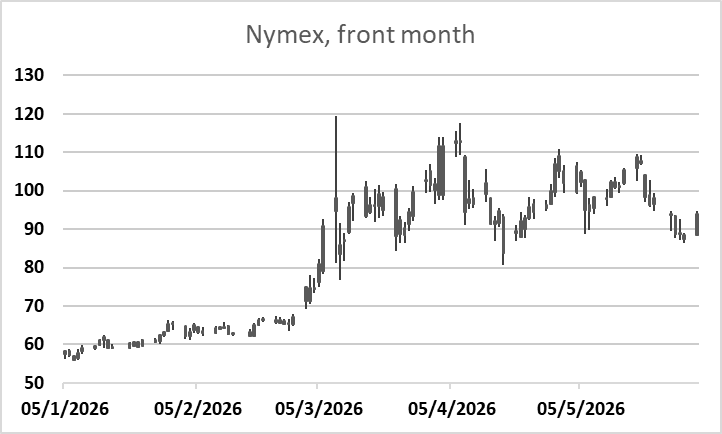

Nymex front month has rapidly unwound last week’s moves to lift back from the old 50% retracement to the old 38% mark and prior highs. Without a US reaction to shut down this dispute then it could quickly find itself back at 100/104 ½ in no time. Quick neutralisation is needed to instead leave the market within Monday’s bar. It’s worth noting that already with the news betting on a fresh agreement by June30 has dropped below 50% odds.

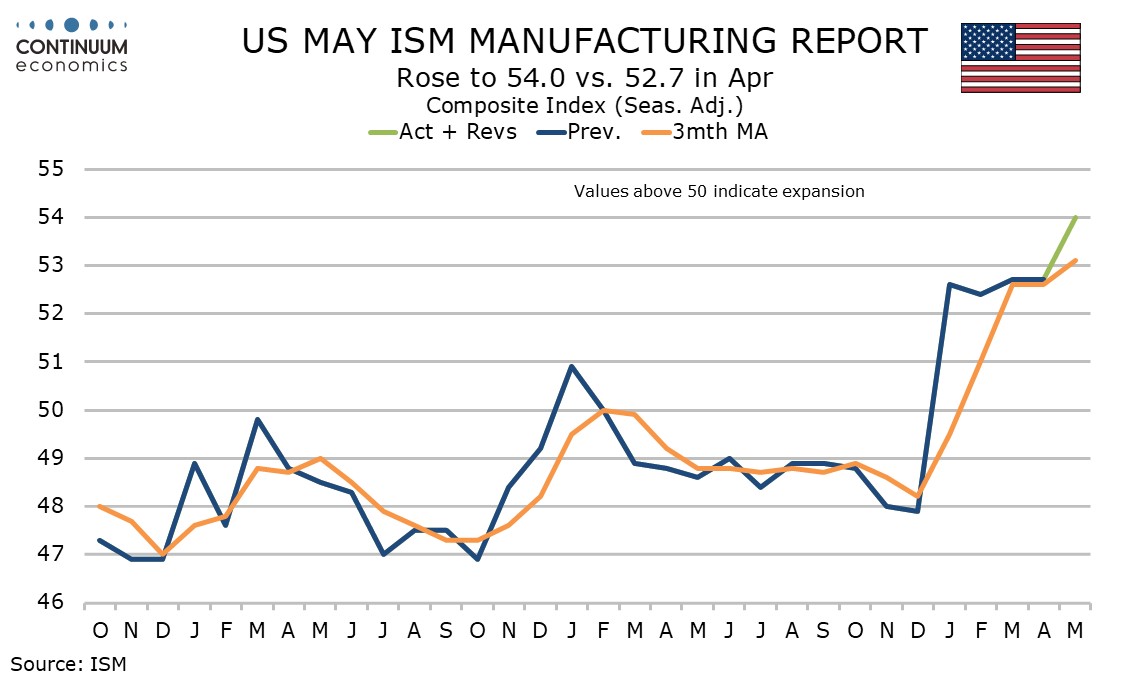

In many ways, the latest flare up is thus the most concerning for a while, so not surprising to see the haven dollar bid suddenly aggravated. Lost in the noise was the latest US ISM meanwhile which tended to play to US exceptionalism (growth supported by AI), but one side of the dollar smile very much secondary to the other at present.

Range rejections tended to amplify the action on the most sensitive pairs (NZD/USD turned back from 0.60 band tops for instance and USD/SEK to a lesser extent from 9.2~) but the action is broad based and dollar driven at present, although also highly whipsaw. For example, USD/CHF has been noisy within a tight band of 1 figure + /- stretch since April. For more contained EUR/USD, 1.16~ is back as the key support again on the latest reactive moves.

The calendar is very much secondary right now. The UK has BoE money supply and lending data while Eurozone has May HICP, with consensus at 3.2% from 3% after mixed national figures, but less crucial given the ECB has already signalled apparent willingness to hike in June pre-emptively.

The US has JOLTS turnover data but with the Friday payrolls the next real focal point.