FX Weekly Strategy: Asia, Jun 15-19

Outcome on Iran pivotal and will colour perceptions of other key events

Dollar pairs hold off break levels, regain on kneejerk if deal sealed, failure back otherwise

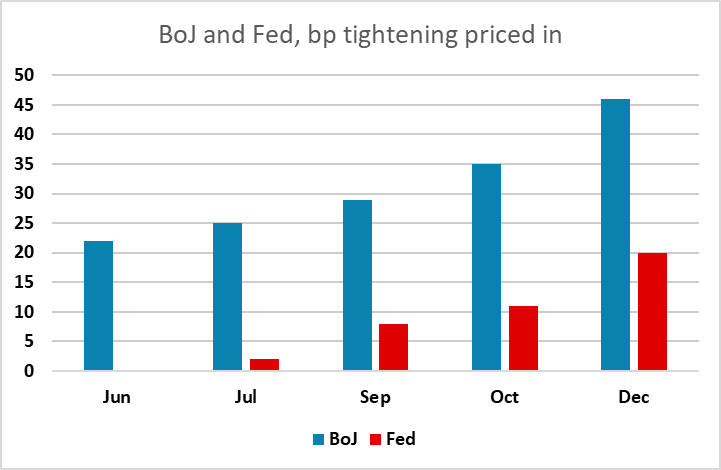

Fed packs in many layers of uncertainty, scope for volatility; mkt may assume 'dots' will be conservative and Iran-contingent

BoJ walks a tightrope to hold the curve and bolster the yen

It’s a pivotal week ahead as a lot of critical factors come to a head: the latest - but this time perhaps more consequential - fork-in-the-road decision on a Iran-US MoU deal; the long-awaited information-dense maiden Warsh-chair Fed meeting and projections; and a BoJ decision where the rate move is largely known, but the guidance and the accompanying decisions on the bond taper are much less so.

It’s fair to say that the first of those provides the critical framing for all the others and whether there’s an outcome could have quite a heavy influence on the tone and stances adopted through many of the others.

Surrounding those key events come the latest from the BoE, RBA, Riksbank and Norges Bank, and in the background the G7 summit in France.

The weekend will also have seen the outcome of the Swiss referendum on capping the population which, at the margin, will also have an independent input on the CHF.

Having lost count of the number of times Trump has teased a deal that hasn’t arrived, the market is wary to 100% commit and in this week-ahead it’s wise not to either. Iran has denied a formal signing is set for Sunday so it’s not in the bag. What can be said at the time of writing is that all the signals on the diplomatic front have suggested a lot of headway has been made on all the major blocking issues. Finding a formulation on freeing up frozen funds was the big sticking point to be cleared in any successful final version. So time will tell whether the deal Trump is willing to sign off does enough to get over the line with the Iran side.

Heading into the end of the week, the oil market was more willing to buy into the finish line than perhaps the FX market, though as yet the oil break of the recent range base has only been tentative. That still awaits confirmation, or not.

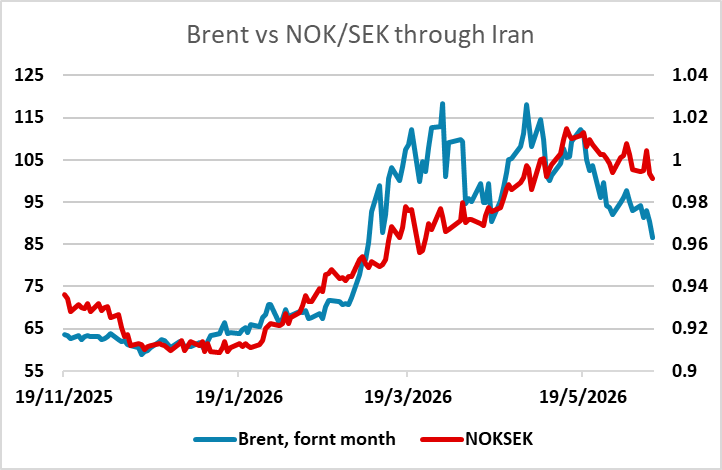

If the deal does go through, then in the immediate kneejerk at least, that will tend to play in favour of some further unwind of recent haven dollar longs. In terms of other candidates, near-term it's likely with the grain of some of the position-driven corrective action seen in NOK. Circa 0.9750 would be the next major reference back on NOK/SEK for instance in terms of retracement on the big 2026 rally.

In terms of central banks, our view is that the Norges Bank is perhaps most clearly already on the side of tight, and ahead of the inflation curve, and overly-priced in the market for the medium-term rates outlook. Sweden in contrast has been particularly weighed by the combination of geopolitics, the impact on its trading partners, and as a high beta counter, the recent wobbles in the wider risk market.

For EUR/USD, 1.16~ is acting as the ‘watershed’ level on deal-or-no-deal. In the near-term, Iran is likely more fundamental than even the Fed tone in determining whether the figure is rejected or regained, setting the technical tone for the week.

For sterling, the BoE may see a greater divide of opinion on show on the Committee, but we expect it overall to nonetheless cement the view expressed recently by Bailey that leaving policy on hold is the best way ahead to balancing two-way risks. On the by-election, the market is already fully set for a victory by Burnham both in the seat contest and then in due course for the leadership. Betting now nudges above 50-50 for Starmer out by end of August, while Burnham is 64% as next PM in 2026. Context matters. If the Iran situation does move towards some interim resolution, that matters a lot more for the fiscal position and sterling risk appetite, even granted there will likely be some modest relaxing of the fiscal stance. EUR/GBP is already near the YTD range floor indicative of the market’s greater comfort with political developments. While this could continue to act as a near-term floor in setting the short-term trade, the price action has been quite constructive for sterling overall.

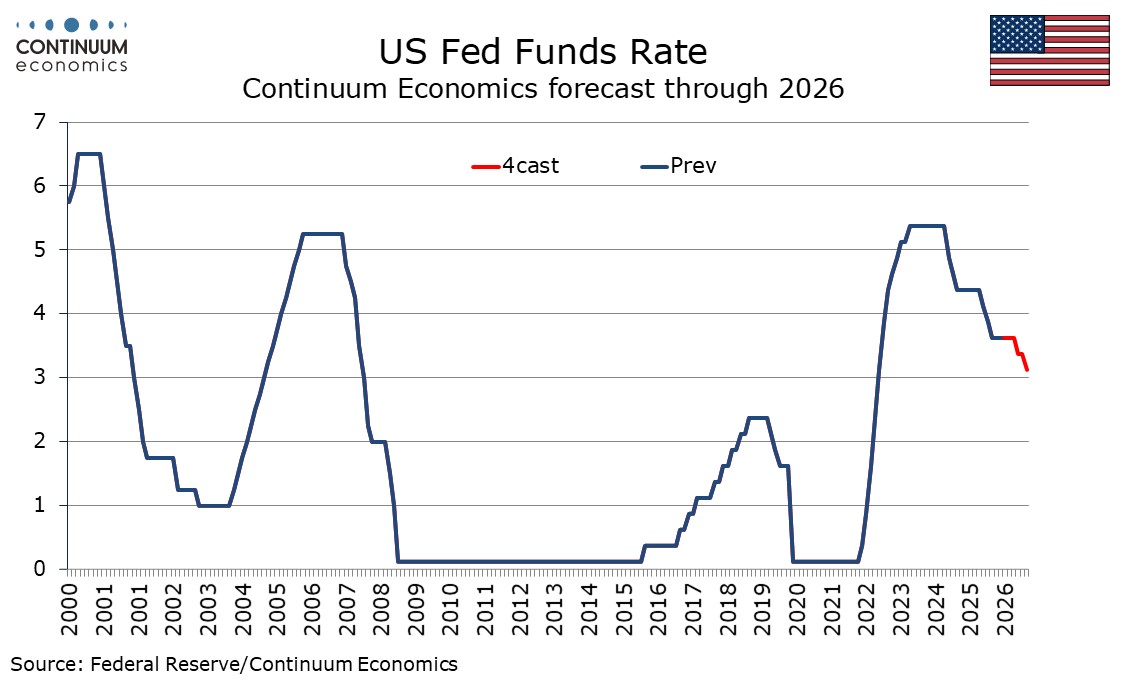

The big wild card for the dollar is whether Warsh arrives with a bang or bides his time on his first appearance. With the projections, the expected shift in bias, and the arrival of Warsh with his own views on policy strategy and possibly even approach to presentation, there is an unusual amount of information density and uncertainty packed in to the event - and reason for options to hedge ahead a wide range of unexpected outcomes. Recent data had been largely ‘hawkish’ but the latest core CPI print did enough to give the wider Committee breathing room to avoid an even harder hawkish pivot. As elsewhere, the market does now have a shift in direction priced, though more modest and backloaded. The ‘dots’ (assuming they are still provided) are expected to show a lower rates profile than the market into next year onwards, but to some extent that is taken as pragmatically driven and would not necessarily see re-pricing. The way the meeting is interpreted could be viewed through the prism of the Iran state of play, as with resolution the market is more likely to view the Fed projections as credible than if the deal falls through and escalates.

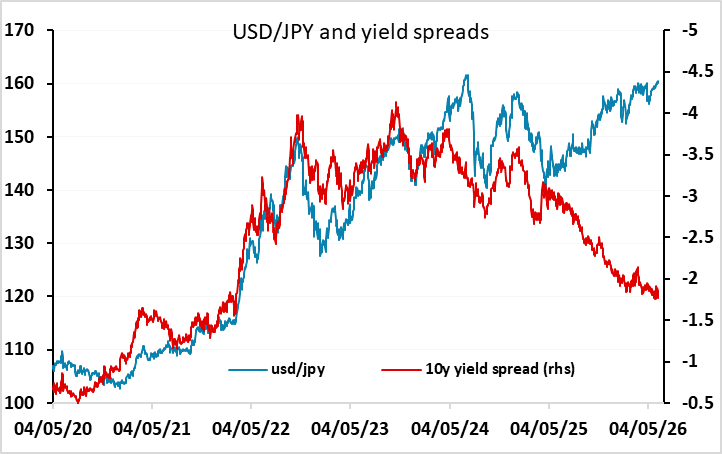

For USD/JPY, focus will be less on the expected 25bp hike than the statement to see how fully it leaves a tightening bias statement in place and what is announced on the bond taper. Not wanting to undercut the impact of the announcement on the yen, while stabilising the JGB market, it makes to keep further hikes on the table while making some moves towards reducing or halting the taper. Any curve flattening out of the meeting - as a marker of credibility and control - could help to further cap USD/JPY, albeit with Iran and Fed outcomes also to play heavily into the mix. The pair has got overbought in recent weeks and any push below 160 on the right mix of outcomes could stretch to 159 with 158.60~ weekly low of 20 May below that.

Data and events for the week ahead

USA

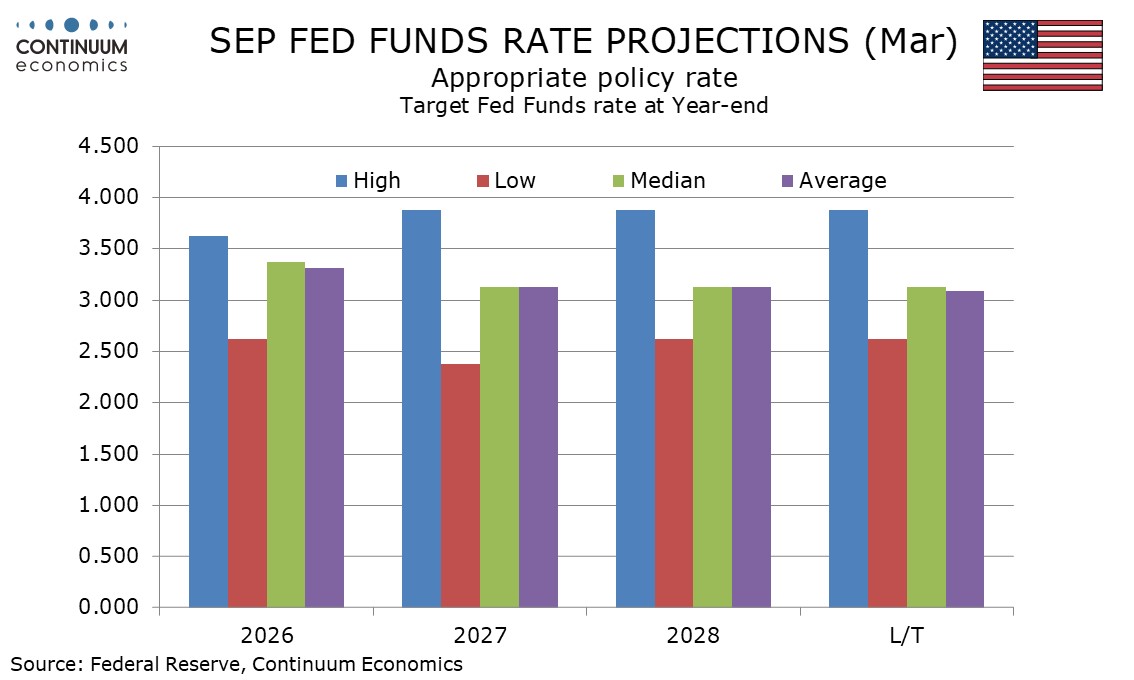

The US calendar highlight is Wednesday’s FOMC decision, the first under incoming Chair Kevin Warsh. We expect no change in rates from a 3.50-3.75% Fed Funds target but a removal of an easing bias to a balanced one in the statement, which will also reflect stronger employment and inflation pictures compared to April. We expect the median dots to see no change in policy this year with a hawkish skew, contrasting a median for 25bps in easing in March’s dots. We expect June’s median dots to see 25bps of easing in both 2027 and 2028. A more hawkish view will be justified by an upward revision to the inflation forecast. We expect core PCE prices to be seen ending 2026 at 3.1%, compared to 2.7% in March, though we expect Warsh to strike a moderate tone in his press conference.

Monday’s data sees June’s Empire State manufacturing survey, while we expect a 0.4% rise in May industrial production, with manufacturing up by 0.3%. June’s NAHB homebuilders’ survey is also due. On Tuesday we expect May housing starts to fall by 2.4% to 1.43m, with permits falling by 0.2% to 1.42m. May import and export prices are also due. Wednesday’s retail sales report for May will be a significant release. We expect gains of 0.3% both overall and ex auto but a 0.1% decline ex autos and gasoline to hint at a loss of consumer momentum. April business inventories follow, where existing data implies a 0.5% increase. Thursday sees weekly initial claims and June’s Philly Fed manufacturing survey. Friday’s calendar is quiet.

CANADA

Canada releases May housing starts on Monday. Also due are April manufacturing shipments, for which the preliminary estimate was for a 4.6% increase, as well as April wholesale sales, for which the preliminary estimate was for a 0.1% increase excluding petroleum. May’s IPPI and RMPI are due on Thursday, while Friday sees April retail sales. Here the preliminary estimate was for a 0.6% increase.

UK

Politics moves towards centre-stage with the by-election on Thursday at which Labour politician Andy Burnham is favoured to win and return to the Commons, thereby setting the stage for what could be drawn-out and acrimonious bid for party leadership and the PM position. The same day sees the next BoE verdict. Not only this month, but we see the BoE being on hold for the rest of the year with rate cuts then resuming through 2027. Although markets are pricing just over two hikes from the current 3.75% with a 50%-plus probability of the first being delivered at the July 30 MPC meeting, our view is hardly eccentric, largely chiming with the UK economist fraternity and even the more recent OECD prognosis.

After what may be softer Rightmove housing data (Mon), the coming week sees several important economic updates looming, most notably the CPI (Wed). Even with Government-paid support measures, CPI inflation will rise afresh from this release for May – we see it back up to 3.2%-3.3% with calendar effects taking services up toward 4% and the core 0.3 ppt higher to 2.8%, all similar to BoE thinking. But the headline may then be at (or near) a peak, especially given the already visible drop in diesel prices.

There are also the ever-more important labor market numbers the softening in which even arch BoE hawks admit could tame second-round effects. But this data release (now partly post-Iran War), encompassing updates not just from the long-standing ONS but also real time figures from the HMRC (which we suggest are more authoritative data and are now officially accredited) is likely to see further drops in the official earnings data. landed, private sector regular earnings are now running at below 3%, the lowest since pandemic related pressures softened them in mid-2020 and down to a pace consistent with the 2% CPI target. Only a little further drop is seen in the looming update. Otherwise, the HMRC numbers are likely to show that employment is continuing to contract and maybe more broadly so as far as the private sector is concerned, while its pay data may suggest a fresh slowing.

Friday sees monthly public borrowing numbers which are very prone to revisions of late. Elsewhere, war-induced worries should feature again and possibly more strongly in the GfK consumer confidence numbers (Fri) arriving on the same day as we expect a similarly-driven further correction in May retail sales figures, especially as the early Easter effect may go into reverse.

Eurozone

Still suggesting weakness even before the Iran War started, construction data (Thu) may show softness. But survey day appears Tuesday with what will be Moe soft ZEW numbers. Otherwise, final May HICP data may show no revision but provide more signs as what drove services inflation higher.

Rest of Western Europe

There are key events in Sweden, not least what have been volatile but trending higher jobless data (Mon). But the focus on Wednesday’s Riksbank decision. Not only at the meeting next week, we still see stable policy though to end-2027 rather than the small hikes markets are now pricing for late 2026. A similar profile has been offered by the Riksbank since last autumn and it may decide to bring forward its first hike hint a touch when it presents it updated Monetary policy report alongside its next verdict.

In Switzerland, there is Thursday’s SNB assessment. Once again and in line with consensus thinking we see SNB policy being unchanged when it gives its next quarterly assessment this month with little shift in the forecasts for either growth or inflation. Admittedly, the tone of the economic outlook will remain guarded but where it will be underscored that it remains too soon to make material changes to the outlook given current continued heightened uncertainties. The strong Swiss Franc will be mentioned but its current strength needs context.

Norway sees the Norges Bank verdict (Thu). It may not have been a close call, but amid what were divided market expectations, the Norges Bank hiked afresh last month by 25 bp (to 4.25%), the first such move in two years. Admittedly, it had given a clear pointer in March of at least one rate hike probable in subsequent next couple of months, implying a good chance that a further such hike will occur is on the cards. Notably, rather than this month, markets are not pricing in such a move until around the November 5 Board verdict.

JP

The all-important BoJ decision is on Tuesday. Our forecast for a 25bps hike remains and very likely they will also suggest a pause in bond purchase tapering. If not, the condition maybe too hard for the JGB market and see yields rise. We are not seeing any change to forward guidance though it does not mean they are hawkish. We still expect 1% to be terminal for 2026 and most part of 2027. Else, we have national CPI on Thursday and should see the number stay artificial suppressed by energy stimulus. It will be a hawkish surprise to see CPI above 2%, a bigger if driven by consumption.

AU

The RBA will also announce their interest rate on Tuesday yet we do not see another rate hike. They made it clear in the last meeting they will take a pause after three consecutive hikes. The headline CPI has shown moderation, should keep the RBA comfortable for now. Forward guidance will likely be not so hawkish and indicates data dependency.

NZ

GDP on Wednesday will be the most important release for NZ next week. Little expectation of any surprises. We also have trade balance on Thursday and other tier two data throughout the week.