FX Daily Strategy: APAC, Jun 11th

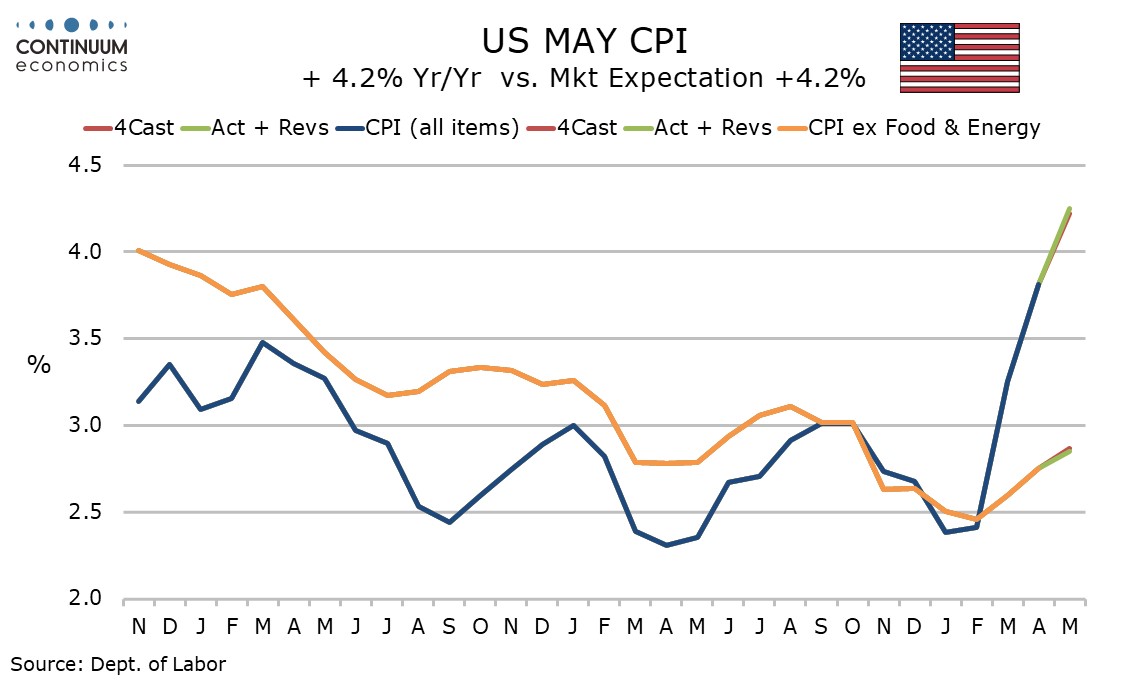

US CPI avoids sticker shock, gives some breathing room, but yield back off limited

Iran headlines still a mix of diplomatic and non-diplomatic, hope and jeopardy

ECB next focus, already a lot in the curve to validate

One event risk has been negotiated for the week, with US inflation avoiding the sticker shock with core coming in on the low side of expectations at 0.2%, if still on-market at 2.9%y/y. The latter is still moderately high of course and at a time of at the very least no output gap. But the lack of further acceleration does at least give the Fed a bit more breathing room than otherwise going into its next meeting as Iran continues to play out, easing some of the pressure to hard-pivot even more hawkish.

Short-tend yields have backed off a bit but not hugely though and the Iran situation itself remains unpredictable. Unpredictable in the sense that the background diplomatic processes are making some headway on the thorny nuclear issues, at least if press reports are to be believed. But the foreground processes are more on the skids - Trump back to infrastructure threats and impatience and Israel holding the ceasefire only in the Trumpian sense (less rather than no strikes). A whipsawed market is seeing an ever diminishing reaction function to the headlines while skewing to the hopeful scenario. The jeopardy of course remains.

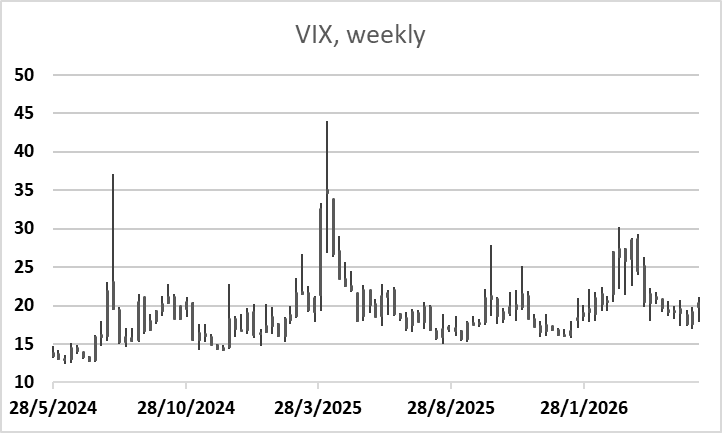

Daily bars on the tech markets have become much wider as intraday volatility has been injected, even if overall volatility remains contained with VIX off the lows but not really sustaining and building from the 20~ reference point.

While the Nasdaq holds off Tuesday’s big spike low and also makes the May low break currently false then it’s trying to find its feet. It has at least done a job to pare what was quite an air pocket from its supporting moving average uptrend, so in that sense it has close to fulfilled the minimum scenario of a light “overstretched acceleration” correction. Especially if there is a following time correction. That given, such pullbacks more often than not do tend to see more follow through before recovering even in the benign shakeout variety so it is premature to call it done. In the fuller retracement scenario of the last rally leg, then it has another 4-8% to go from levels as of writing. Absent major Iran news, that is still the more immediate driver leading USD-high beta majors right now. These pairs are still tending towards pressuring support from a technical perspective.

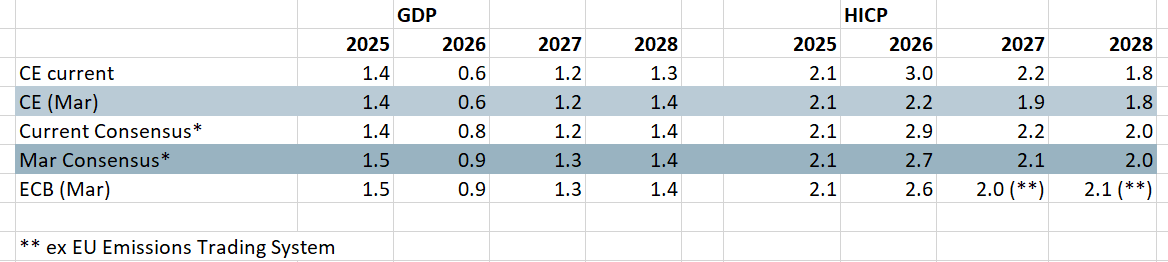

Figure 1: Economic Outlook From Various Perspectives

Source: CE, ECB, Consensus Economics

Focus switches to the ECB meeting next where a 25bp hike is 100% priced in. As such, the ECB comments and updates projections will be the main issue and give clearer signs as to how fast and further the Council consider policy rates may have to rise. Given what the market already has priced in by next Spring, there is a lot there already to validate. In that sense the bias might be skewed towards ‘sell the fact’ for the euro, and quite a high bar for it instead to prove net hawkish and bullish on the day.