SARB Hikes Policy Rate to 7.0% Amid Rising Geopolitical and Inflation Risks

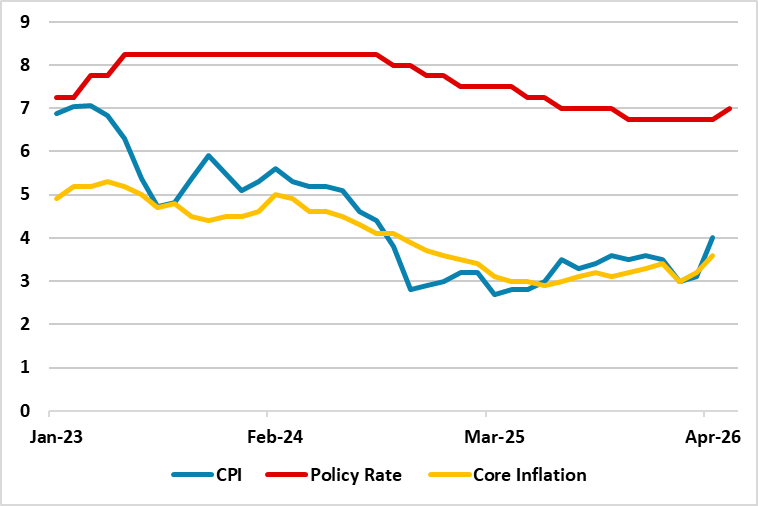

Bottom Line: South African Reserve Bank (SARB) Monetary Policy Committee (MPC) convened on May 28, and announced that it hiked the key rate by 25 bps to 7.0%. This decision was driven by mounting upside risks to price stability, most notably the conflict in Iran, a volatile rand, and rising headline inflation, which hit 4.0% y/y in April due to costlier energy and transport. The SARB also decided to adjust its inflation outlook upward driven by geopolitical anxieties; the inflation forecasts for this year and 2027 were raised to 4.4% and 3.7%, respectively, compared to prior projections of 3.7% and 3.3%.

Figure 1: Policy Rate (%), CPI and Core Inflation (YoY, % Change), January 2023 – May 2026

Source: Continuum Economics

South African Reserve Bank (SARB) Monetary Policy Committee (MPC) convened on May 28, and announced the third key rate decision of the year. As we expected, SARB increased the key rate by 25 bps to 7.0%, marking the first interest rate increase in three years. The MPC decision was a close call as four of the six members of the MPC preferred a hike, while two favored no change.

We think SARB is primarily concerned with the upside risks to inflation including Iran conflict, volatility of ZAR and elevated inflation which increased to 4.0% y/y in April due to higher energy and transportation prices. (Note: According to Stats SA’s announcement on May 20, inflation edged up to 4.0% y/y in April from 3.1% in March, reaching its highest level since August 2024 with fuel prices rising 11% in April).

SARB Governor Kganyago characterized the rate hike as a significant measure to keep inflation expectations anchored to the 3% midpoint target. Kganyago warned that inflation risks have escalated, as severe and concurrent global shocks will likely trigger second-round effects that necessitate a monetary response.

Alongside with this, the MPC statement outlined three alternative economic scenarios, each signaling a need for further monetary tightening. In the worst-case scenario—which factors in a prolonged Middle East crisis, El Niño weather patterns, and non-linear economic shocks—inflation is projected to breach 6%, potentially forcing three additional rate hikes in 2026.

It is worth mentioning that the SARB raised its inflation forecasts for this year and next to 4.4% and 3.7% respectively, from 3.7% and 3.3% previously. The SARB also cut its domestic growth forecasts for this year and next to 1.2% and 1.7% respectively, from 1.4% and 1.9%.

The domestic inflation outlook remains highly exposed to the geopolitical conflict in Iran since the country is sensitive to international energy market disruptions as a net importer of petroleum products. Under these conditions, convergence toward the 3% inflation target will likely be delayed unless geopolitical risk premiums recede and oil prices moderate. Absent a de-escalation of the conflict in Iran, the SARB will feel the pressure to consider additional monetary tightening in H2.