FX Weekly Strategy: Asia, Jul 20-24

ECB meeting main event, though Lagarde will be reluctance to provide a clear hint on the September meeting.

Tech correction could be more relevant this week, watching performance of broader market and volatility

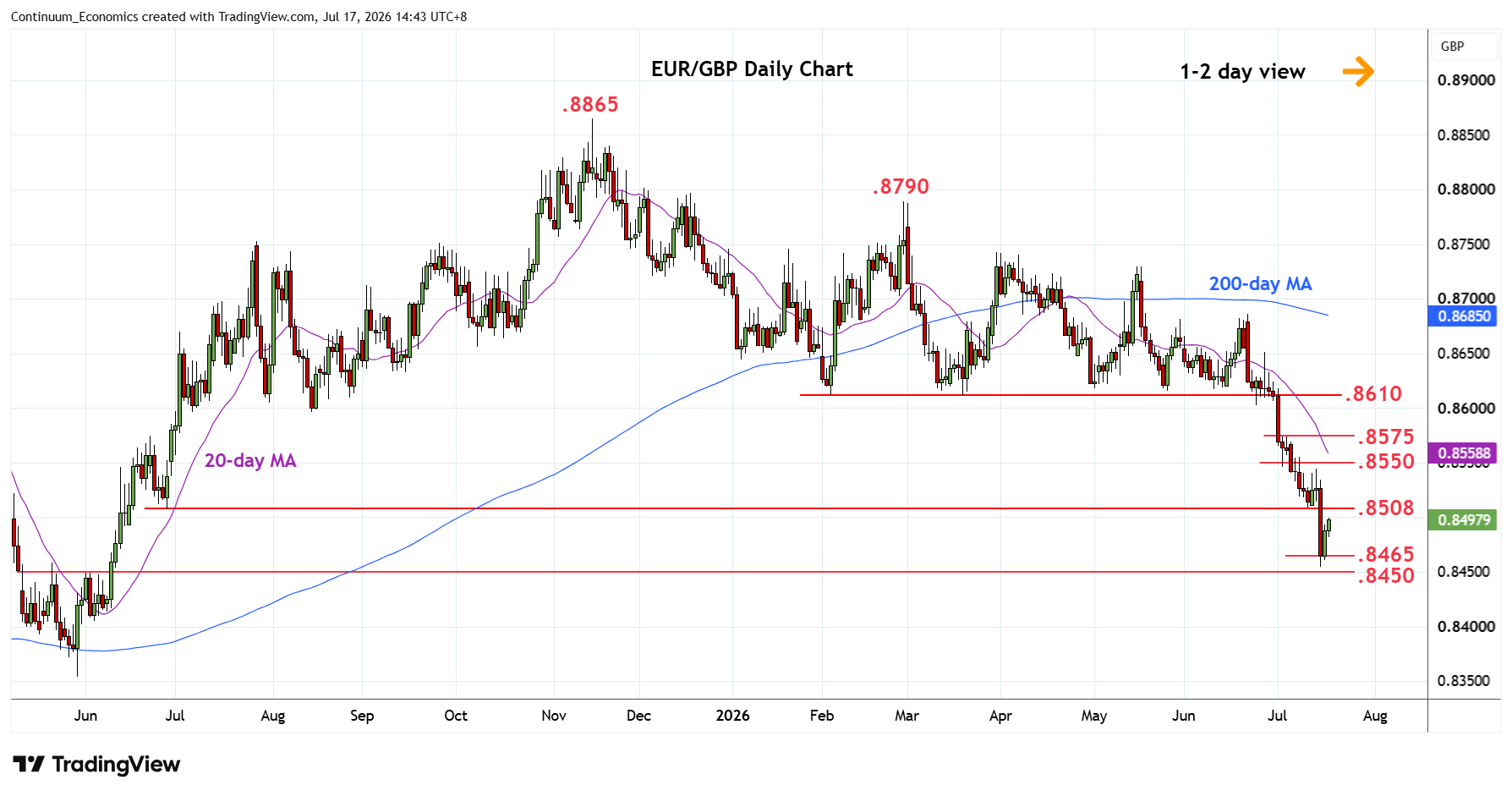

New UK PM takes over and confirms cabinet. Sterling already bought the rumour near-term?

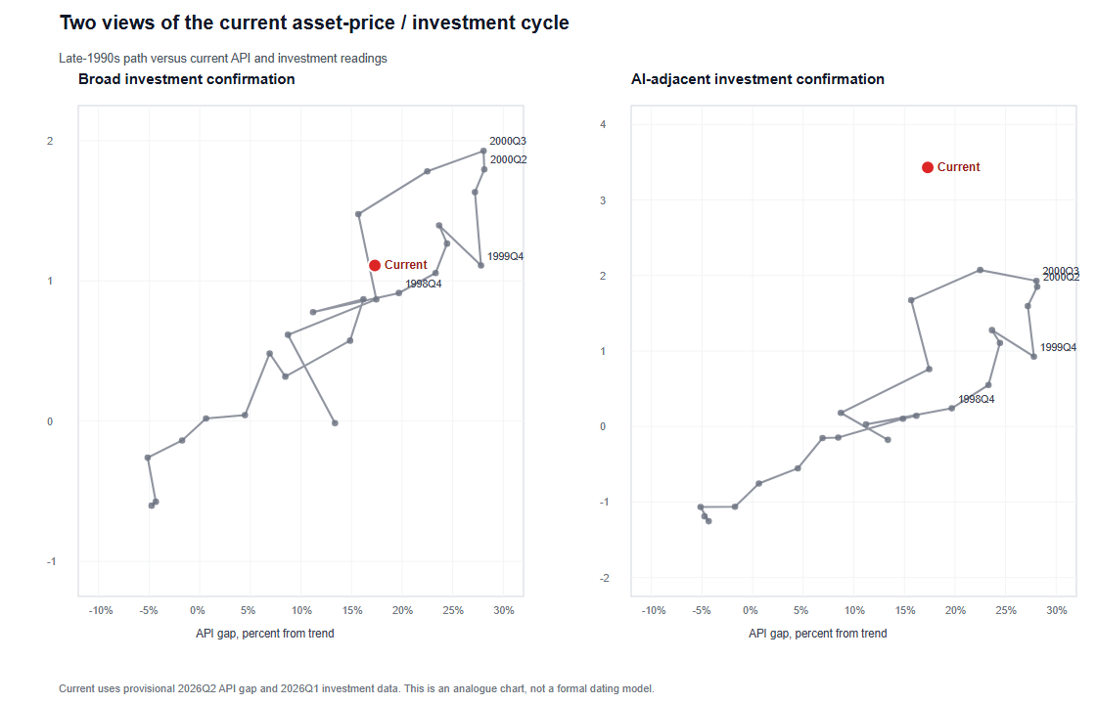

Zooming out from the day to day for a moment, the market remains broadly characterised by what has remained one of the dominant themes since the spring – climbing (or slipping on) the wall of worry coming from Iran on one side, and the AI cycle on the other.

The latter was again surfacing more prominently into the close of last week, as the market starts to question the level of build out commits in the pipeline amid over-capacity, cash and cost-spike constraints concerns, and whether they will ultimately materialise. Overlaying that also came the rate hike and leveraged ETF clamp down from Korea, set against a wild Kospi market that had already notionally moved into bear market territory from its prior moonshot north.

We discuss some of this bigger picture backdrop in a forthcoming report That argues that current asset price conditions might be viewed as ‘late 1998’ in terms of their cyclical extremes, while the narrower AI-adjacent investment path has already exceeded 2000 peaks, albeit with some non-residentials investment substitution and a more capex intensive innovation cycle than dot.com.

That’s more a story for coming months than days to play out, but for the week ahead the rather narrower focus is simply on whether tech profit-taking and in some cases liquidation intensifies and fuels some summer de-risking. And whether recently flatlined volatility sees any life as a result, or whether stock rotation for now saves the day. VIX is still ultra-compressed at present, but back above 20 along with any stirring in FX volatility and it does become slightly more material to very short-term carry sentiment.

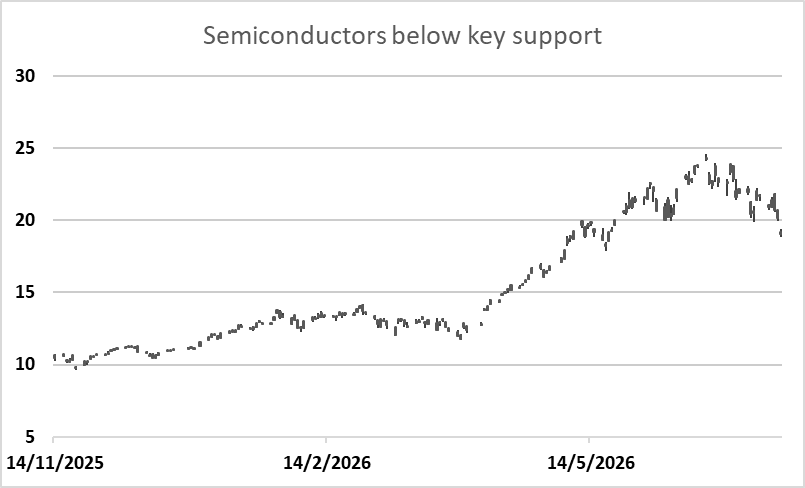

As a narrow sector, semiconductors took out key support Friday (recent major high/low and 38% retracement of the rally from April) with the gap down which could open some quick downside to the 50% retracement (another 8% down) and the 19th May low (-10%).

In terms of carry, the yen has been compressing up into a coil amid the current two-way standoff which could (though not necessarily) be building for a faster breakout move. If it does turn out to be a carry-trimming downside one, rather than an eventual triangle continuation move, then 160.50-00 is the draw. The market has got a bit comfortable with sleeping on ‘summer low vol carry’ so there’s always the potential for these little shakeouts when the lethargy breaks. Japan is also on holiday on Monday though so far the yen has avoided any self-inflicted sell-offs on thin market intervention concerns.

Regarding the S&P break back lower in the recent top range has 7400 close inner range support (so far easily held) then 7200 as the key short-term wider support, with further quicker downside where that to give way.

The highlight of the week comes from the ECB meeting and press conference, although we do not expect it to provide much guidance regarding September, sticking to the non-pre-commit language to keep options open depending on data and geopolitical events. That will probably leave market expectations (currently almost fully priced for Sep) unaffected and more attuned instead to energy developments and the next rounds of inflation data.

EUR/USD has marginally widened its recent trading band but not substantially. Range upside has been slightly lifted to 1.15 with 1.1375-25 on the downside but the 1.14 recent pivot still broadly holds sway.

The UK has its busy week but data is not seen moving the BoE away from its summer wait-and-see stance and focus is going to directed to the launch of Burnham’s premiership, and cabinet appointments.

Cable may now have broadly completed its range-rally squeeze, for now, and bar more impulsive action may have become a little stretched. If we see ‘sell the fact’ after buy the rumour on a market-benign cabinet appointment (more on that below) then that too would suggest that the leg has run its course and with more profit-taking on the tactical long coming in. If equity tone does remain risk off, that also tends to skew sterling towards an underperforming bias.

Data and events for the week ahead

USA

It is a very quiet week for US data and Fed speakers will be quiet as the July 29 decision approaches. Thursday’s initial claims data will cover the survey week for July’s non-farm payroll. On Friday we expect improved S and P PMIs for July, manufacturing at 55.5 from 53.9 and services more modestly at 51.5 from 51.2. We also expect a correction higher in June new home sales, by 6.0% to 615k, but trend has slowed in the year to date.

CANADA

Canada releases June CPI on Monday, and we expect yr/yr growth to slow to 3.0% from 3.2% on energy, but with CPI-Median at 2.1% and CPI-Trim at 2.0% both unchanged from both April and May. Thursday sees May retail sales, for which the preliminary estimate was a rise of 1.0%. On Friday June’s IPPI and RMPI are due.

Eurozone

The key event is the July 23 ECB meeting and the statement and press conference, as the market seeks to understand whether the ECB could hike in September or later. Lagarde however will likely not provide specific guidance re September.

Elsewhere, July 24 sees the provisional PMI data for EZ and major countries. The EZ composite is expected to be down marginally to 50.0 from last month 50.2.

UK

The key event will be the announcement on a new Chancellor, with Andy Burnham set to take office on July 20. If Shabana Mahmood is confirmed as largely assumed by the press and market by the end of last week (85% now on betting), that’s seen as gilt market friendly, while Ed Miliband (<5% now) would raise concerns over fiscal slippage.

A heavy economic data schedule is led by the June CPI figure on July 22 where headline is expected to move up to 2.8% from 2.4%, but core inflation to fall 0.1% to 2.6% Yr/Yr. June retail sales on July 24 will also attract attention with the world cup expected to have boosted the monthly and yearly figures. Labour market data is also released on July 21. They key will be the average earnings ex-bonus, which is expected to remain unchanged at 3.4%.

JP

Key release for Japan next week is on Friday, where we have the June national CPI. Widely expected to be kept under 2% from stimulus, core-core could have exceeded expectation as rising real wage and recovery in household consumption squeezes. Else, there is also trade balance on Tuesday.

AU

Labor data on Thursday should continue to points toward a solid Australian job market. The historic participation rate is here to stay while unemployment and headline changes will likely chop seasonally. It would be great to see an upbeat full-time employment changes after a strong part time growth in May.

NZ

We have trade balance on early Monday and the more important Q2 CPI on Tuesday. Q2 CPI will likely be close to 4% in light of the energy shock. While being previewed by the RBNZ, the jump will likely lead to gains in the Kiwi as market participants confirm the hawkish tilt in RBNZ OCR path.