FX Daily Strategy: Asia, Jun 17th

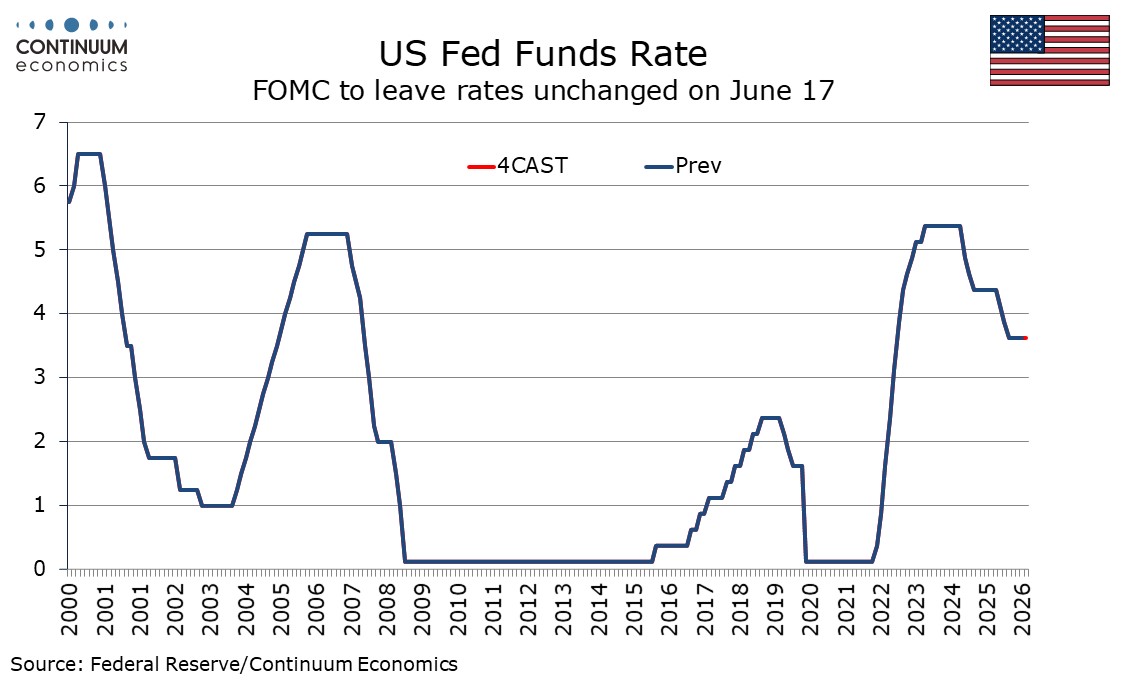

FOMC Dropping the easing bias

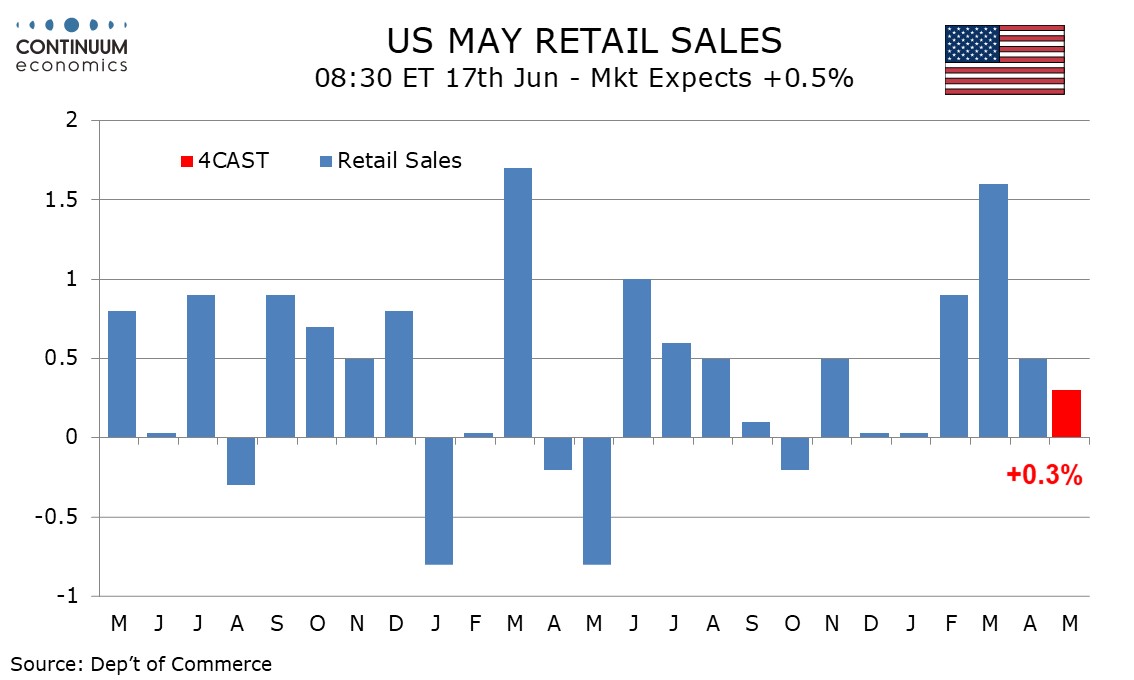

U.S. May Retail Sales a pull back

Riksbank Mild Tightening Bias to Persist But Not Exercised

UK CPI Peaking

The FOMC meets on June 17 and while a change in the Fed Funds target range from the current 3.5-3.75% is unlikely, the statement is likely to drop the easing bias. The median dots are likely to get a little more hawkish with a hawkish skew in the detail, with inflation forecasts, even ex food and energy, likely to see a significant near term upward revision. The post-meeting press conference will be of particular intertest, being the first from incoming Chair Kevin Warsh. He is likely to be less hawkish than some will feel upgraded inflation forecasts would justify.

The last meeting on April 17 saw three hawkish dissents, from Cleveland Fed’s Beth Hammack, Minneapolis Fed’s Neel Kashkari, and Dallas Fed’s Lorie Logan, who wanted to drop an easing bias. Governor Stephen Miran dissented for an easing but he has now left the FOMC. Then Chair Jerome Powell hinted at the press conference that others were inclined to drop the easing bias, and minutes from the meeting stated that many were. This is likely to happen at this meeting, though given high levels of uncertainty the statement is more likely to be open to moving rates in either direction rather than giving an explicit tightening bias.

We expect May retail sales to increase by 0.3% both overall and ex autos, but with a 0.1% decline ex autos and gasoline, which would suggest that consumers are starting to pull back as elevated gasoline prices increasingly weigh on real disposable income.

Gasoline prices increased further in May, even if May’s gain, like April’s, was less sharp than in March. While gasoline looks set to be a significant positive on prices, autos look unlikely to have much impact. Industry data shows only a marginal increase in sales, not fully erasing a modest decline in April.

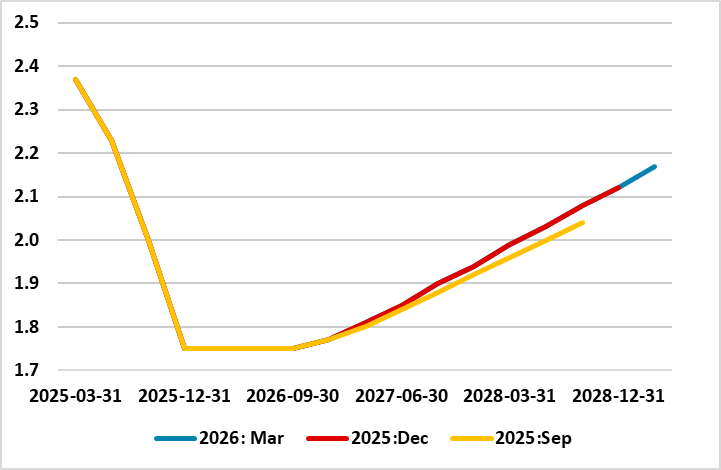

Figure : Riksbank Policy Rate Outlook

Not only at the meeting next week, we still see stable policy though to end-2027 rather than the small hikes markets are now pricing for late 2026. A similar profile has been offered by the Riksbank since last autumn (Figure) and it may decide to bring forward its first hike hint a touch when it presents it updated Monetary policy report alongside its next verdict. Indeed, in March, it tweaked its forward guidance by suggesting that, even amid Middle East conflict making the outlook very uncertain, it was in a good initial position to adjust monetary policy if required to safeguard the inflation target and no longer pointed to no change for some time to come. Somewhat better data in the last on both the GDP and CPI fronts may even harden this guidance, but underlying inflation is still well below Riksbank thinking while its own survey data and the labour market provide a timely reminder of on-going economic fragility.

Indeed, the just-released Riksbank business survey underscores both downside risks to growth and inflation. It notes that due to the Middle East conflict uncertainty has increased again, which the companies involved say risks delaying the already prolonged recovery. At the same it notes that while companies do intend to increase their selling prices in the coming year, they emphasise that it is very uncertain to what extent higher costs will actually be reflected in the prices so that at the current juncture they are talking about small price increases. As for actual price trends, the latest CPI figures surprised on the upside (for once). Even so, perspective is needed as CPIF excluding energy (CPIFXE) – an official indicator of underlying inflation – is still only 0.5% y/y, ie almost half the Riksbank's forecast from its most recent March projections

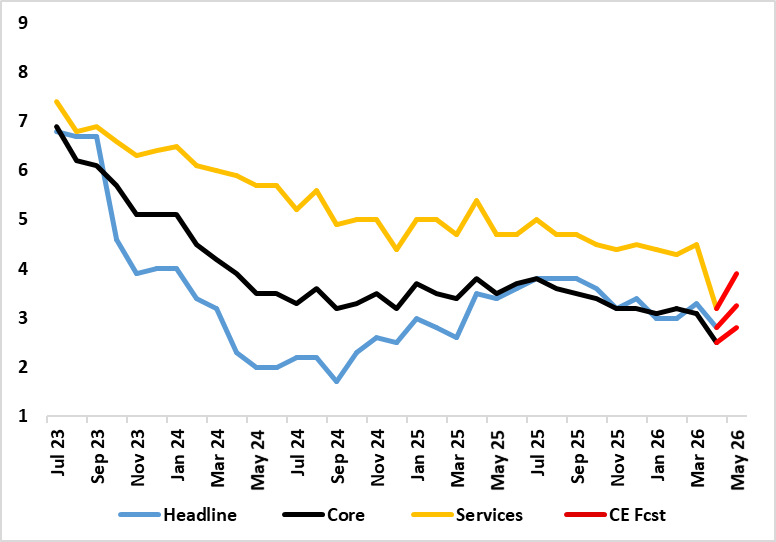

Figure: Headline And Core To Bounce Back?

What have been energy induced price rises are now very evident, even more so in some aspects of the latest PPI data. Regardless, actual CPI have offered a more benign picture both in terms fo headline and underlying trends. Indeed, having seen headline CPI jump to 3.3% in March and where services rose to 4.5%, the headline was down to a lower-than-expected 2.8% (BoE saw 3.0%) despite a 15% m/m rise in fuel related energy, this offset by services dropping almost a full ppt, taking the core down to 2.5%, a four-year low. This will not last as even with Government-paid support measures, CPI inflation will rise afresh from this month – we see it back up to 3.2%-3.3% with calendar effects taking services up toward 4% and the core 0.3 ppt higher to 2.8%, all similar to BoE thinking. But the headline may then be at (or near) a peak, especially given the already visible drop in diesel prices.