FX Daily Strategy: Asia, Jun 23rd

U.S.-Iran, On and off

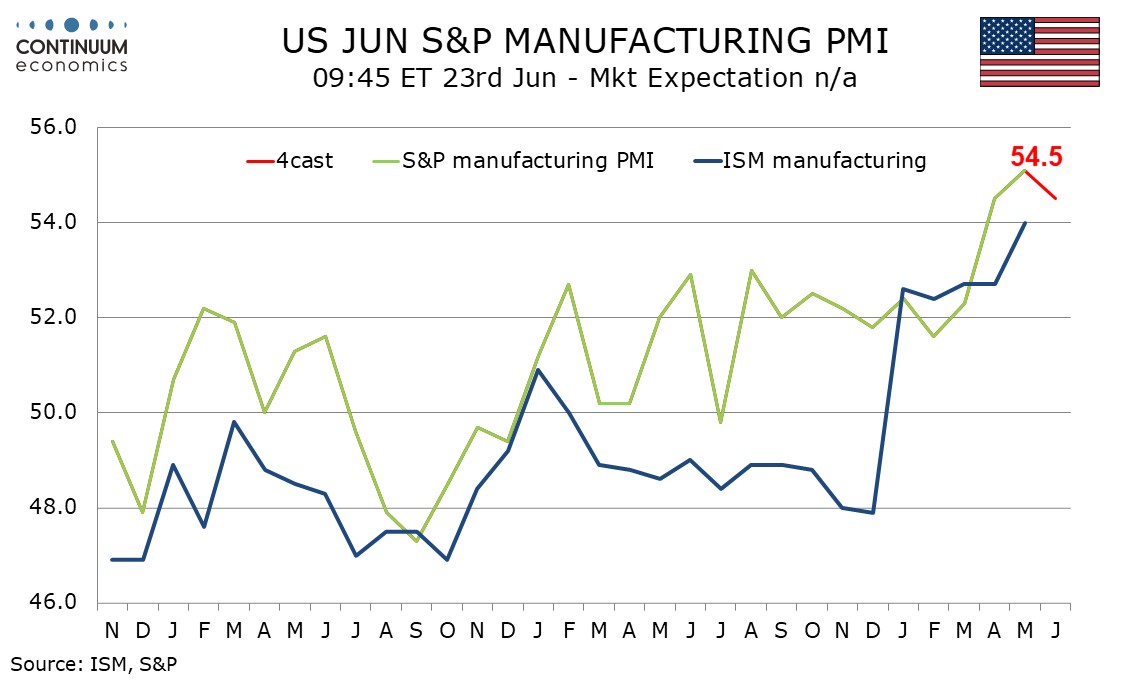

U.S. June S&P PMIs not quite as strong

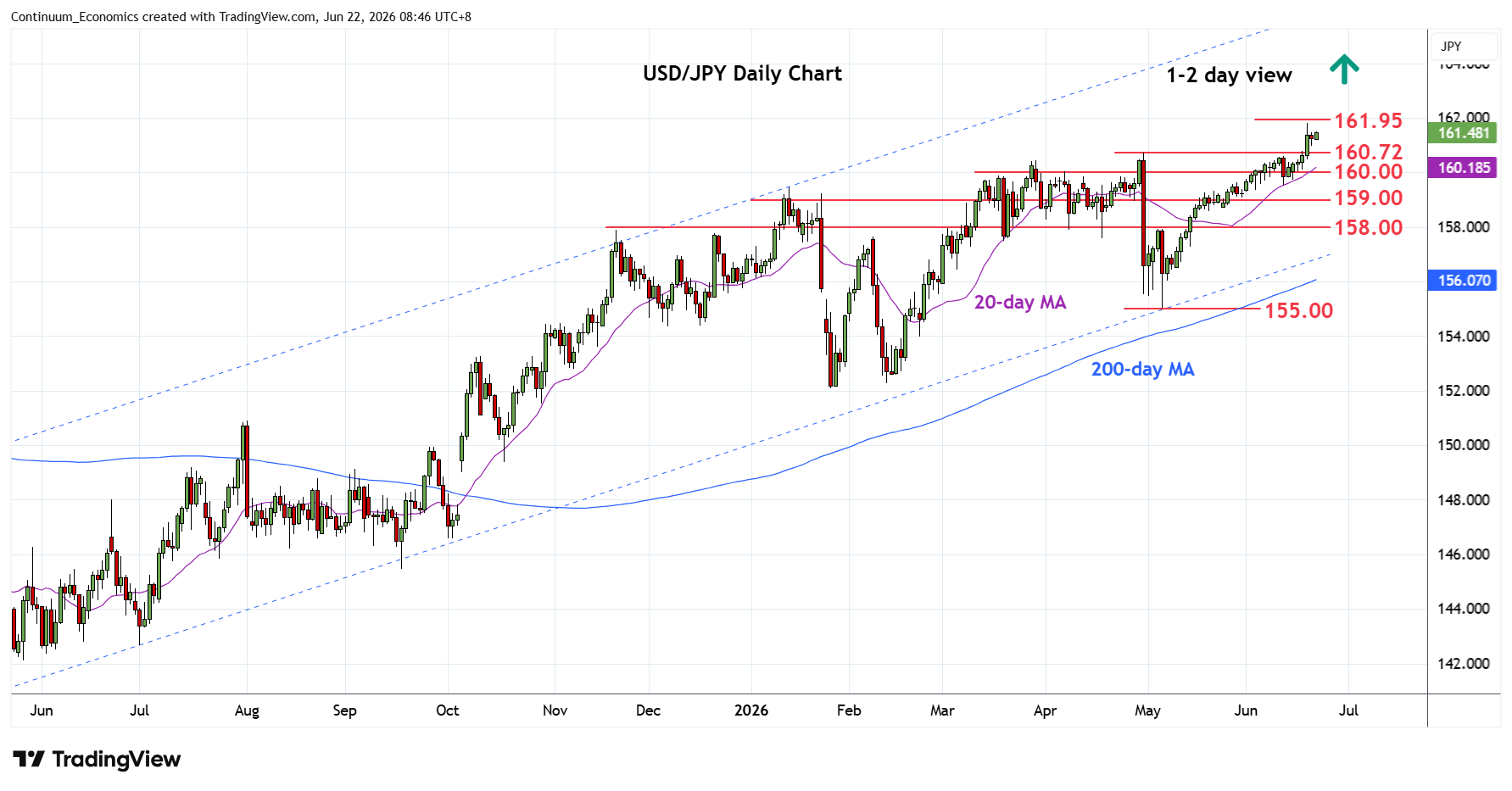

USD/JPY in Intervention Zone

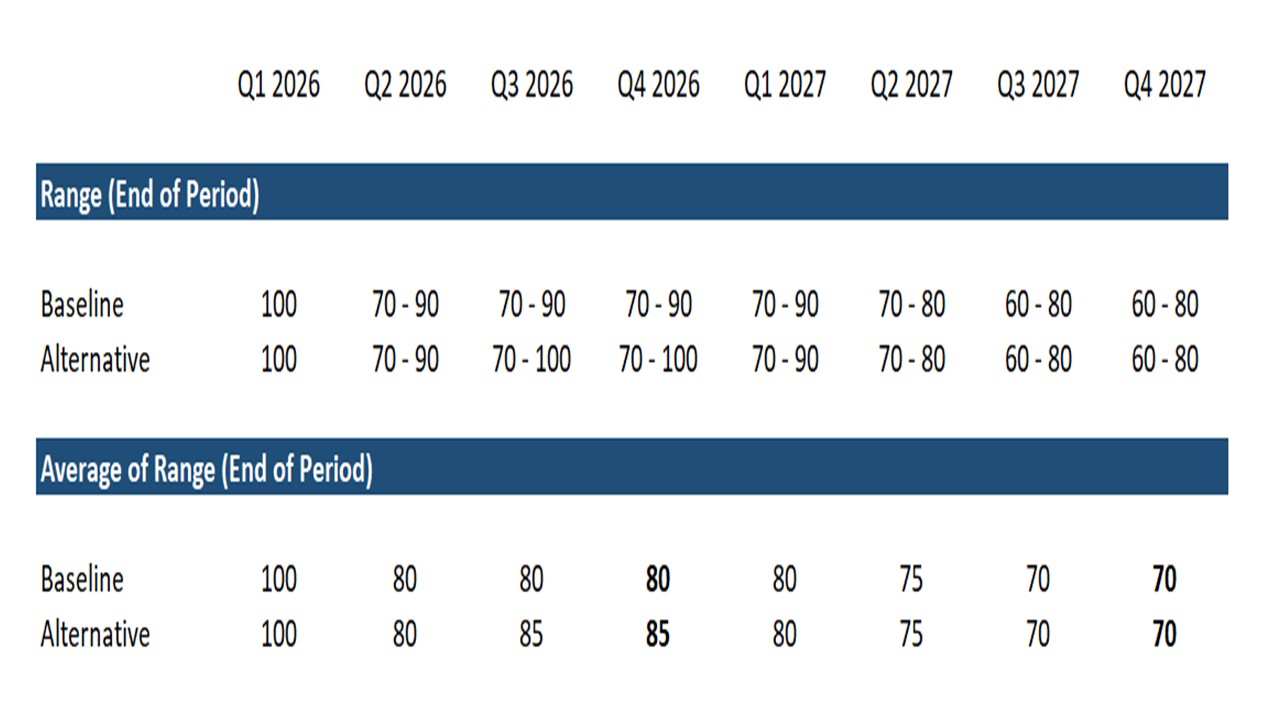

Figure: WTI Oil Price Projections (USD)

Our baseline (80%) is that the Strait of Hormuz will reopen in H2 2026 and remains open through 2027. However, logistics dislocation plus a switch from commercial inventory rundown to rebuilding will likely slow the decline in oil prices back towards normal levels.

Nuclear negotiations between the U.S. and Iran will be tricky and could drag on. However, the agreement has a minimum commitment that the IAEA will supervise the dilution of 440kg of highly enriched Uranium. Neither side will want a prolonged breakdown of the interim agreement, which would close the Strait of Hormuz again and cause economic pain.

A restart of major military hostilities between Iran and the U.S. is thus unlikely. In this scenario, our baseline is for a gradual reduction in oil prices. Iran may have the ability to impose a fee of ships later in the year, but shipowners would likely pay this and it would add marginally to the cost of oil. However, a number of countries have stopped production and restarts could take months rather than days.

We expect a correction lower in June’s S and P manufacturing PMI to a still firm 54.5 from 55.3, but a modest improvement in the S and P services PMI to a still subdued 51.0, from 50.7 in May. May’s S and P manufacturing PMI was the strongest since May 2022, and backed by an improved ISM manufacturing index. However we feel a further acceleration will be difficult to achieve. May manufacturing output paused after a strong April rise, and June’s Empire State manufacturing survey lost momentum. June’s Philly Fed manufacturing index picked up from a negative May, but remains off recent highs.

USD/JPY continues its grind higher and has a steady foot above the 160 figure. We are very likely close to intervention zone but the pace of rally may not be rapid enough in the Japanese officials' eyes. If we are seeing another rally of more than a percent, it could very much trigger a response from the BoJ.

On the chart, the pair settled back from fresh year high at 161.80 as prices consolidate above the 161.00 level. Bullish gains from the 155.00 May low keep pressure on the upside with support at the 160.72 high of 30 April and the 160.00 figure expected to underpin. Would take break to fade the upside pressure and open up room for deeper pullback to 159.53/159.00 area. Meanwhile, focus remains on the 161.80/95 highs and break here will extend gains to fresh multi-year high towards 163.00/164.00 congestion area from December 1986.