FX Weekly Strategy: Asia, Jul 6-10

FOMC, ECB Minutes, RBNZ decision the highlights

Dollar ardour cools but spreads still in favour

NZD attempting to bounce if RBNZ plays ball

USD/JPY has done some n/t chart damage

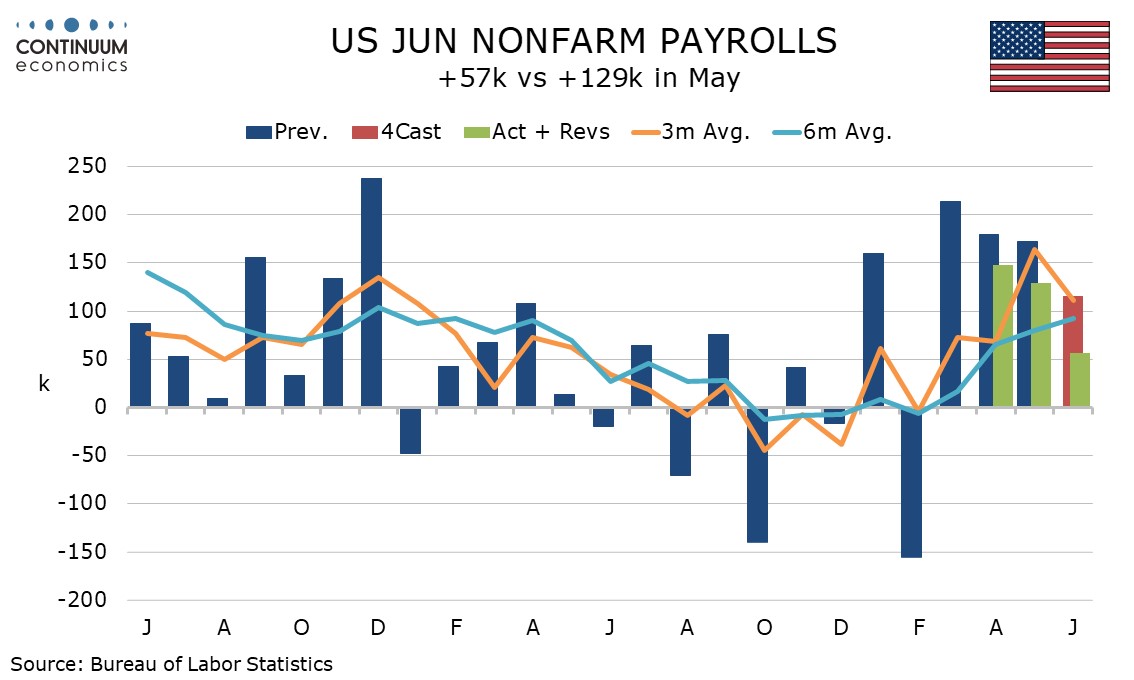

Last week, payrolls did indeed prove to be the defining feature. It is reasonable to say it did quite a good job of diffusing some of the more immediate Fed pressures at least when it is set within the context of the current fence-sitting debate. That said, we wouldn’t want to be overreading into the last few prints either and there was still enough for everyone as the unemployment rate dropped, albeit labour force driven (which might itself also even be a World Cup distortion).

The upshot remains that the proof of the current pudding regarding AI impact, neutral real rates and degree of output gap will be the inflation prints going forward and that is still an open question even if energy’s reset to pre-Iran prices will make itself felt.

The other main point to take away is that the retreat in tightening pricing odds has been a parallel experience and not just US-centric (quite the opposite in fact), even if it has cooled the market’s recently heated dollar ardour.

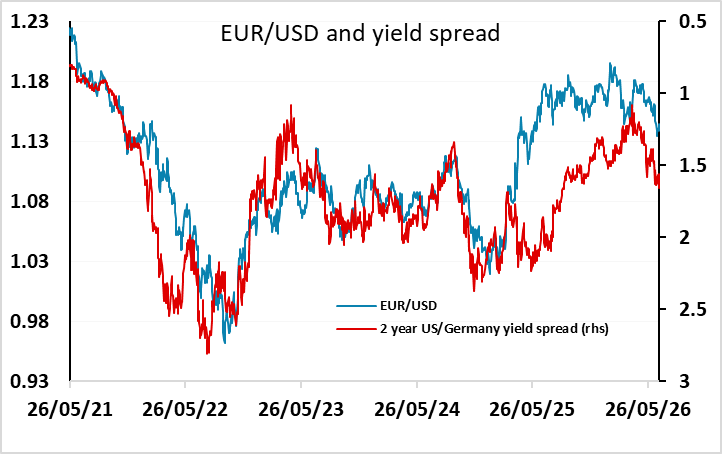

The money market doesn’t have another ECB tightening fully priced in until December now either and that as more the peak. Recent data, oil, and tip-toeing by ECB comments less hawkish (Lagarde calling growth and inflation more balanced now) - these all actually tend to hint more at an extended pause that could segue discretely into a current top.

All but to say, the upshot is that 2yr spread and (to a lesser extent) 10yr are still actually pointing EUR/USD more south rather than towards meaningful recovery.

While you might have to allow a certain amount of market and technical momentum, that argues that any extension of the EUR/USD bounce beyond the current lift to 1.1450 if seen should be maxing out at 1.15, and then looking to roll lower again, if maybe needing a new trigger to be doing so at any speed again.

It’s a comparatively quiet week ahead, but it is headlined by FOMC (and to a lesser extent ECB) Minutes, and the latest RBNZ decision.

ECB Minutes are going to look dated and superseded by recent inputs (CPI data, oil and comments). Fed commentary though will be given more weight, especially given this may increasingly become the main source of any colour if forward guidance is otherwise discontinued. These Minutes are also slightly dated true, but any more substantive debate about tightening risks and inflation risks might be enough to slow the market’s more dovish pivot for now.

RBNZ is the other big event of note and it does come at a time when NZD is showing signs of “wanting” to bounce, if you can put it like that. NZD/USD has respected and bounced off 0.56 and actually regained 0.57. If that is cemented then it can establish back into the prior 2026 range and encourage some short covering. Similarly, AUD/NZD has also been rolling back from the high retest. Spec wise, it was also one of the few pairs as of last week where the market was still quite strongly short versus the dollar so it has that asymmetric positioning backdrop.

In terms of the call, the market is currently priced at around 80% chance of a hike, and then at about 90% chance of reaching 50bp in September. There are some prominent calls for unchanged though as Iran impact has unwound. If the RBNZ does enough to validate the current curve then NZD could well be the week’s main performer. At a more abstract/conditional level, we would continue to watch El Nino (just declared in NZ too) as a risk factor later in the year but for now the market focus is on more immediate, tangible factors (especially while current weather is actually quite wet).

Finally, the other key trend to take into the week ahead is what could be some significant recent price action in USD/JPY and the yen more broadly on the crosses. Chart wise it has done a bit of damage thanks to the burst of yen short-covering. There have been mutterings about potential MoF tactics, but this is largely a self-policed and self-spooked move from over-extended positioning. It has the added feature that burst of yen short covering, deliberately or otherwise, can become a popular speculative activity too. With the break of what has been quite an extended short-term uptrend, the pair can stretch down to 160 next and then maybe lower.

Data and events for the week ahead

USA

The highlight on the US calendar will be FOMC minutes from June 17 on Wednesday. Dots showed a fairly even spilt between those looking for tightening this year and those looking to keep policy steady. While we feel the voting line up is tilted towards the latter camp any suggestions that tightening should be considered in the near term will attract attention. Fed’s Williams and Logan speak on Thursday.

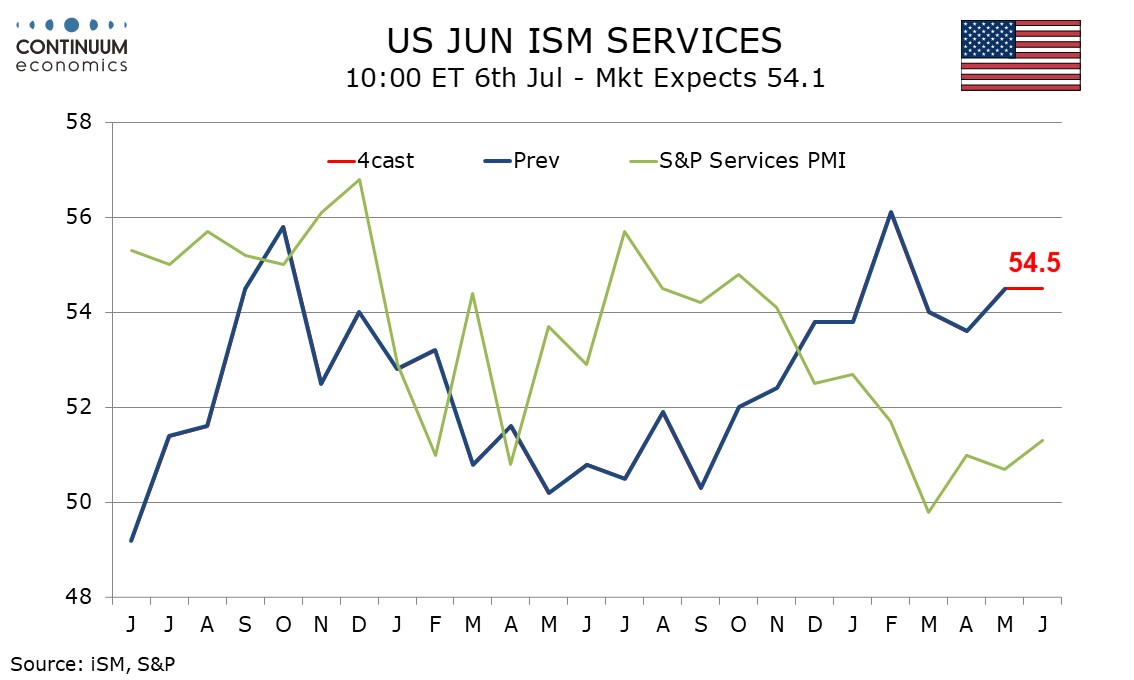

On Monday we expect June’s ISM services index to hold steady at 54.5. On Tuesday we expect May’s trade deficit to increase to $78.7bn from $55.9bn in line with signals from the advance goods report. May wholesale sales are due on Wednesday. Thursday sees weekly initial claims and June existing home sales, which we expect to rise by 1.9% to 4.25m. Friday sees no significant US data.

CANADA

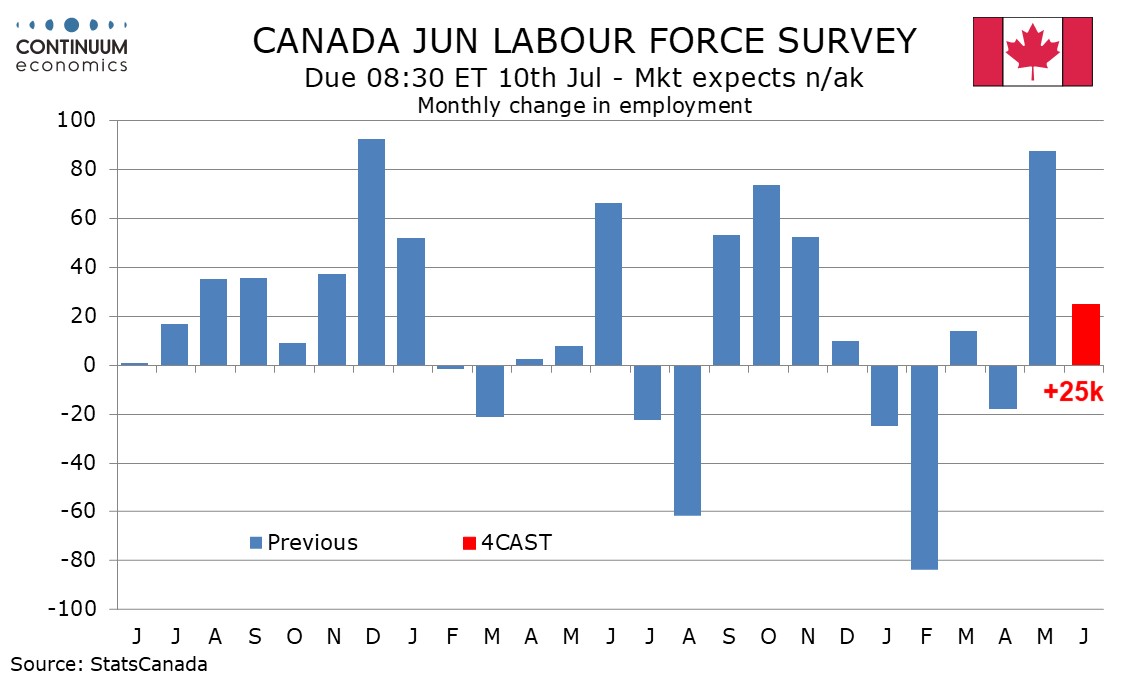

Canada’s most significant release comes on Friday with June’s employment report. We expect an increase of 25k to extend on a strong May increase with unemployment falling to 6.5% from 6.6%. May building permits are also due on Friday. Monday sees June’s S and P services PMI. Tuesday sees May’s trade balance and June’s Ivey manufacturing PMI.

UK

Coming before what may still be soft construction PMI data (Mon), there are more housing survey numbers. These RICS data are likely to remain soft but without signalling any marked correction. Such a worry will remain in the BoE Financial Policy report though. Back in December, the FSR warned that risks to financial stability have increased during 2025 and those risks surely must have increased further given recent market moves, not least energy and AI swings.

In the FPC’s judgement seven months ago, many risky asset valuations remain materially stretched, particularly for technology companies focused on Artificial Intelligence. Equity valuations in the US are close to the most stretched they have been since the dot-com bubble, and in the UK since the global financial crisis. This, the FPC thinks, heightens the risk of a sharp correction.

Eurozone

German industrial production numbers data (Tue) are preceded by order numbers (Mon), the former likely to see a second successive rise and this coming in the first month of the conflict. Otherwise, construction PMI data (Mon) may remain very weak. More ECB insight arrives Thursday, with the minutes to the June 11 rate hike decision. That 25 bp official rate hike unveiled was so well-flagged it is hard to suggest that it was consistent with a decision process on a meeting-by-meeting basis. Similarly, the dominance of inflation upside risks, alongside another dose of optimistic real economy projections, is hardly proper data-dependency. All of which shows where the ECB focus lies (a sharp contrast perhaps to the BoE). But while the projections show HICP inflation back in line with target by Q4 next year, this already looks out of date given June HICP numbers. While a further hike cannot be ruled out given the ECB’s biased reaction function, we think that this 25 bp hike is more than enough and that this misplaced move will be more than reversed into 2027. The week is wrapped up by further ECB speeches on Friday.

Rest of Western Europe

There are a few key events in Sweden, not least what is expected to be near-unchanged headline June CPI flash numbers (Jun). Such an outcome would be consistent with the Riksbank latest projection. Norway on Friday also releases the latest CPI figures, which may also chime with Board thinking.

JP

Kickstarting the week are Labor Cash Earnings and Household Spending. While both are important, more weight would be on wage growth as it is the main drive for household spending. The latter will need to see a rebound to improve private consumption growth which been lagging for the past two months. Elsewhere, it is just tier two data throughout the week.

AU

Quite an empty calendar for Australia next week. Only private inflation survey on Monday, along with ANZ job ads.

NZ

All-important RBNZ interest rate decision on Wednesday. Widely expected to be a no change with hawkish tilt. Some even expect forward guidance of a July hike. Business PMI is also released on the same day.