FX Daily Strategy: Asia, May 28th

Pullback in oil sticking, even if on fragile ground

Focus has been on some of the 'oil terms of trade crosses' and profit-taking

Market remains a prisoner to the Iran headlines n/t

We remain in the territory of initial drafts, of provisionals, of MoUs – and of course before going through the Trump-randomiser. But the market continues to have little choice but to price according and assume that the ‘logical’ solution of an initial, but fragile, truce will kick in at some point, for a month to then work precariously towards a final agreement. If we do get there, that will remain a month fraught with risks and bad faith breakdown potentials, particularly with Trump stuck between the desire for an exit and the push back from conservatives on concessions. And most of all the optics on how it compares to the Obama deal - the triggering, legacy-breaking driver that prompted the whole current scenario back in the first term.

As things stand at least, so long as that Strait opening is on the table, we are back at May lows and sitting just off the April base ($95-90 on the Brent front month for example). We have already seen that as the latest pullback is showing stickiness (trend down for most of the last two weeks through the noise) the FX market is having to see some give, especially on popular “oil terms-of-trades cross” trades that had been the staple. And not just popular but rather stretched on a short-term spec basis.

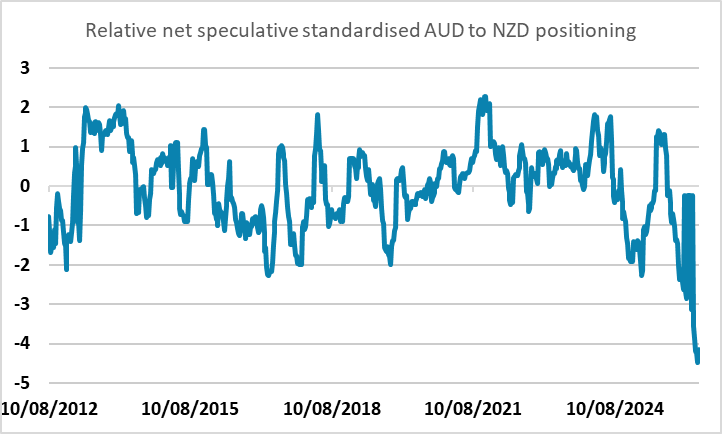

AUD/NZD is one of them of course and while the RBNZ was the initial trigger with the split vote, it is arguably more that overstretched positional setup along with the vulnerability of the NZD leg to some unwinding of the negative oil pricing that was more to the fore. Having taken out 1.2135/15, 1.2050/00 is the deeper corrective support.

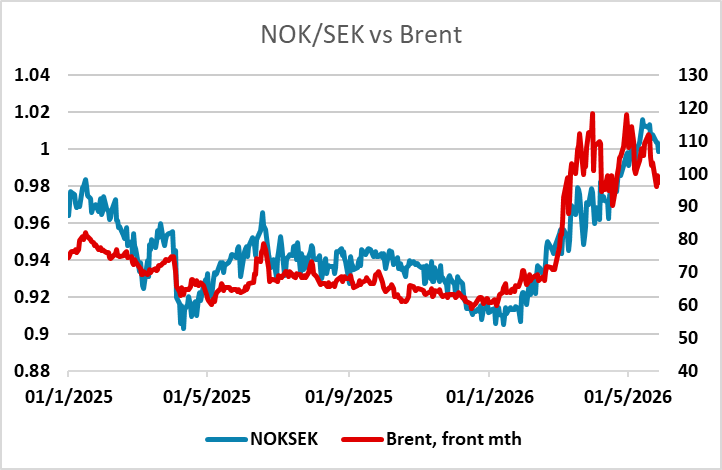

Likewise, NOK/SEK has been a popular and easy Iran trade with a good runup from the cheap cross levels and so similarly seeing some long reductions and profit-taking kick in now that its gap to oil’s retreat is sticking. Sweden sees its latest Economic Tendency Survey Thursday and while it is not expected to be positive, the focus is more on forward looking pointers from global developments.

So long as this holds, the bias towards lightening, as well as short-term squeeze risks, remains. 0.986/00, 38.2% and 29 Apr low could end up attracting on the profit-taking move if we avoid any decisive negative Iran news.

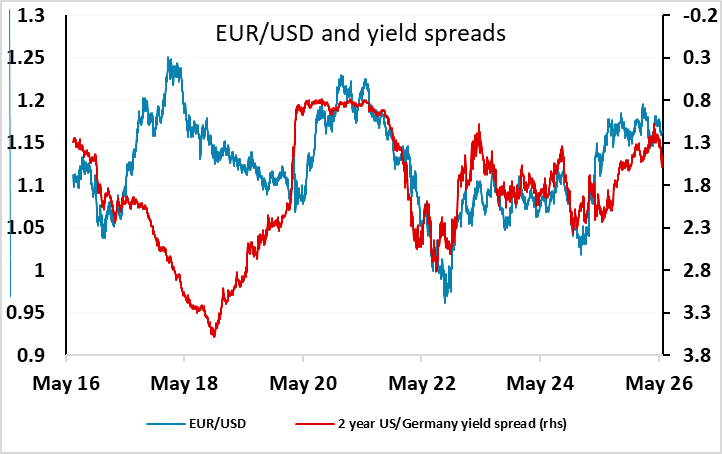

With positioning being more definite on the crosses, dollar positioning is a bit more neutral arguably (think mid 1.14-1.18 ish on EUR/USD for example). Recent news has stemmed the dollar squeeze though, especially as US yields have backed off from the steep runup to uncomfortable levels. Recent short end spread narrowing has been stalled, although levels still don’t leave the euro looking cheap. The bigger background question for the market is whether it remains more focused on spreads than it is on drivers (comparative growth).

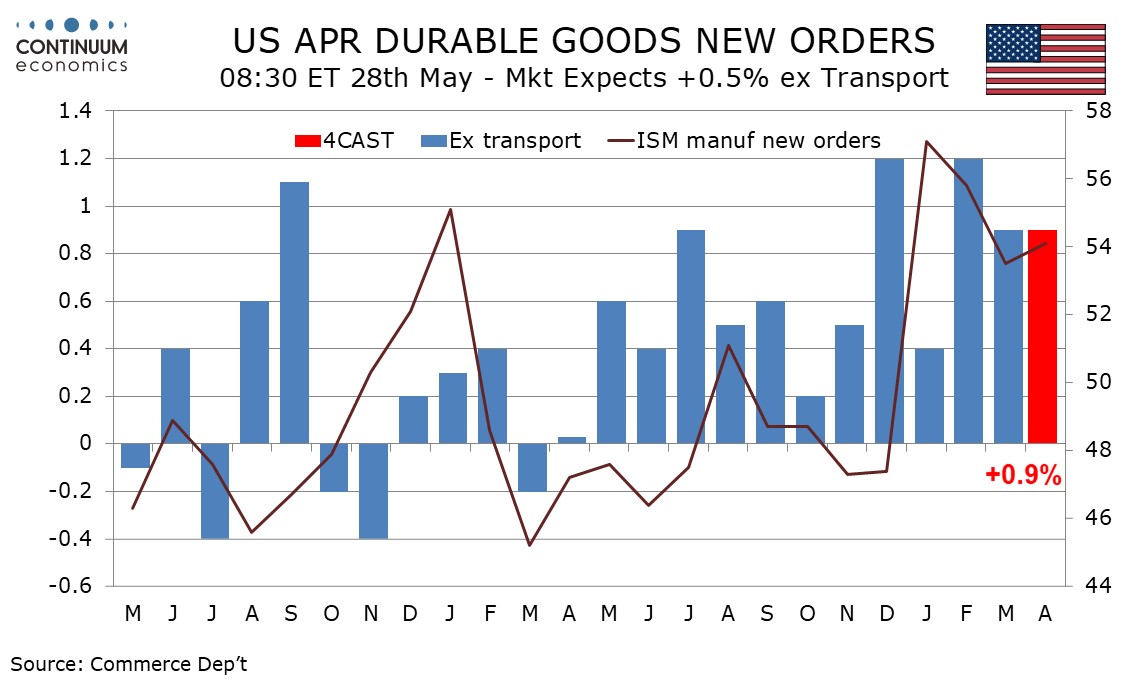

It’s a busier calendar in the US Thursday which should still see that relative US resilience on show, especially on the non-residential capex side. We expect a 0.3% rise in April’s core PCE price index, with overall PCE prices up by 0.5%, personal income up by 0.3% and spending up by 0.5%. We expect Q1 GDP to see a marginal upward revision to 2.1% from 2.0%, and April durable goods orders to rise by a strong 4.5%, with a 0.9% increase ex transport. Weekly initial claims ate also due. April new home sales follow, where were expect a 2.5% decline to 665k.

Tokyo CPI data is out in Japan but after recent BoJ comments the market has already been well primed for a likely June hike. Further recent compression in volatility together with some potential month-end hedging rebalancing support is helping keep USD/JPY propped into the 159 handle topside limit just off the MoF cap. At present it still looks like it is going to require another burst of heavier intervention if the pair is to be pushed back from the159-160 zone back to the 156~ long term uptrend.