FX Weekly Strategy: Asia, Jul 13-17

Quiet summer markets, if some with idiosyncratic drivers

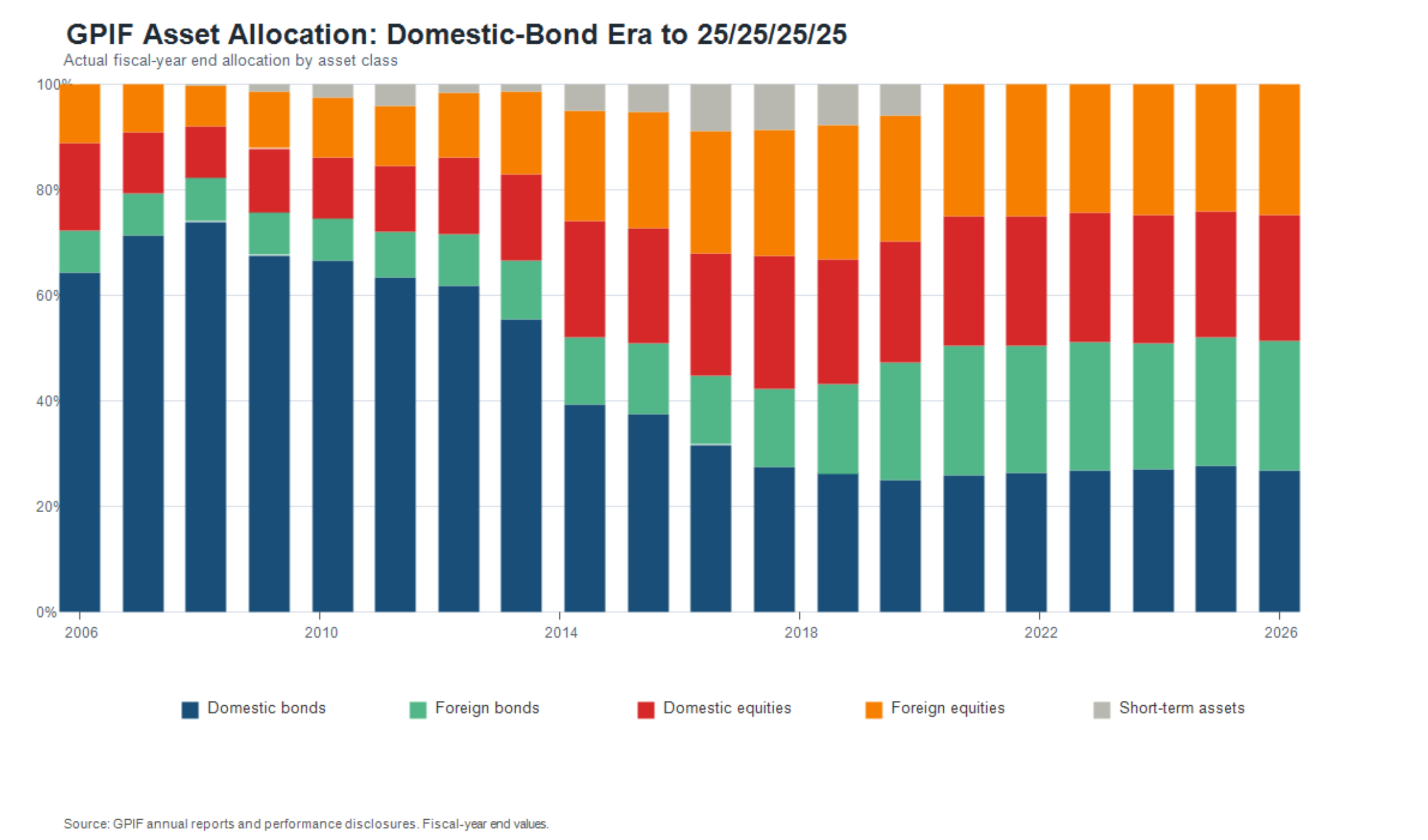

GPIF story is one to watch on USD/JPY. Market may be being underestimated it, for all its procedural issues

US CPI and Warsh testimony provides the calendar highlights

While it might be an exaggeration to say the FX market has entirely entered the summer doldrums, it does seem to need a lot of prodding right now to get moving in any meaningful way - tending to focus more when it does on the idiosyncratic factors where reaction is more forced.

Kiwi was our pick for last week, and the RBNZ hike did indeed see AUD/NZD roll over and NZD/USD squeezed back into its prior range. 50% back on the last leg there would be roughly 0.58, and 61% another half figure if the squaring isn’t quite done yet. The cross though has made the obvious nearby range support / break level at 1.2~ before holding, and that might speed limit now. The wider range floor on the cross is more like 1.1925/30.

NOK was another small outlier to the drift on Friday where the latest CPI print (if it can be trusted given the stats office problems) was enough of an outsized downside miss to give a bit of extra credence to our economist house view that policy is rather tight there and Norges’ bank overly hawkish on the inflation risk and policy profile.

As ever though, developments on Iran and oil do remain pretty fundamental both here and more broadly. The latest outbreak may have quietened into the end of the week, but the fundamental issues regarding the arm-wrestle over Strait control as a geopolitical tool are not going to go away, nor are the open-ended headline risks.

Some idiosyncratic factors are more important and lasting than others though, and the ‘GPIF story’ is certainly one. It is embroiled in complications and details that need some expounding but the net result could eventually have reach.

We will discuss this in more detail in a forthcoming report. For now, it is worth noting that even though the whale was let lose by Abenomics over 2014-2020 - ironically partly to weaken the yen and generally reflate, to become one of the worlds biggest and most successful hedge funds and carry traders, so the meme goes - there is still potential for a determined government to window guide the GPIF towards significant allowable adjustments.

Procedurally, there are real issues to bringing it back to the days of a government slush fund. But already allowed flexibility within the mandate and 5-year plan could create notable ripples if it can be pinned to a rationale and investment justification (VAR and historically extreme FX divergence risk say).

All that but to say, it’s dangerous to underestimate the Japanese government’s determination to drive capital flow shifts when it wants to. Recent comments imply a realisation that intervention only will lack firepower unless MoF can prompt a wider structural expectations and flows shift and encourage others to adjust and piggy back with it.

Tuning out from big picture to immediate, the market itself is proving a slower burn. If the potential starts to get traction, then the pair could look back to 160 next however. More technically, a break back below 161.50 will open up the 160.72 monthly high of 30 April. A further close beneath here will add weight to sentiment and confirm continuation of July losses, initially to congestion around 160.00.

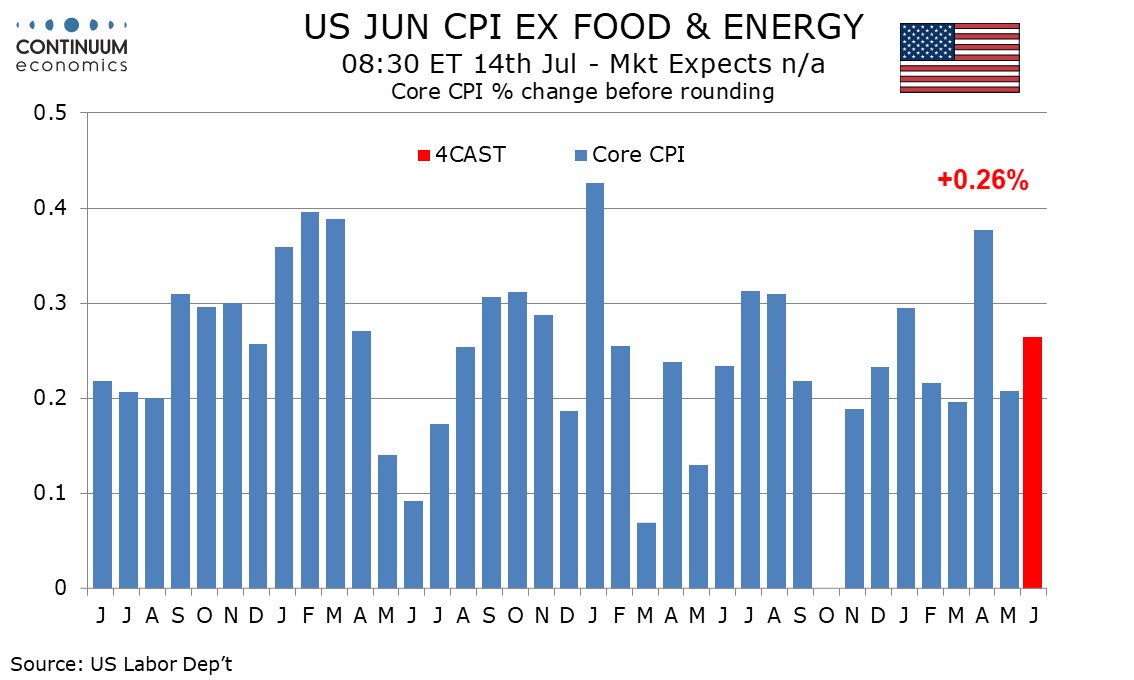

In terms of the week ahead, the biggest focal points otherwise come from US CPI, whose importance was again underscored in the last FOMC Minutes, and testimony from Warsh shortly after. Our 0.3% and 2.9%y/y call is in line with market and enough to keep the rate ‘too high’ but without materially changing the Fed’s open-minded two-scenario view on where it goes from here. We probably need to be seeing a few more months of data yet before any stronger biases emerge on the assessment. Warsh meanwhile is more of a wildcard.

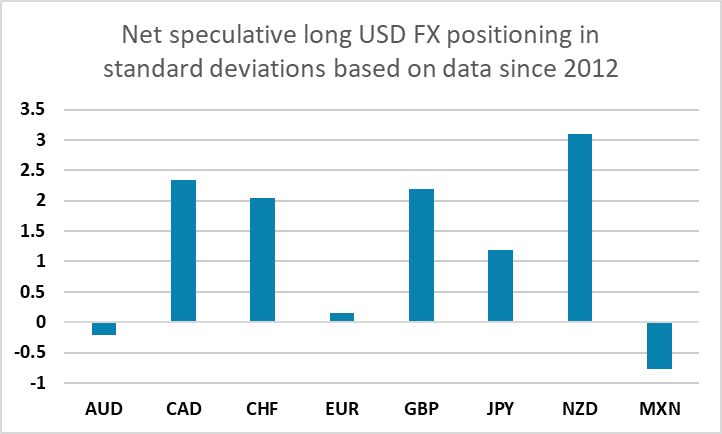

Generally, the dollar at present does face some baggage wit the spec market generally long on most pairs other than the euro and EUR/USD itself proving quite stymied by proportionate moves being seen in ECB expectations (the market has pushed back out its ECB view to a full 25bp by Sep). If the dollar index’s slightly near-term heavy lean is to play out, it might need both Iran issues not to spike and for it to come from USD/JPY and out to other pairs. Otherwise, EUR/USD in particular remains a highly compressed market at 1.14 +/- 50 or some pips. Technically, a close above the 1.1473 weekly high of 2 July is needed to improve sentiment and extend late-June gains towards congestion around 1.1500

Data and events for the week ahead

USA

The US releases June budget data on Monday and June’s NFIB small business survey on Tuesday. The most significant release of the week wis likely to be June’s CPI on Tuesday, which we expect to be unchanged overall, but with a slightly firmer 0.3% rise ex food and energy, 0.26% before rounding. The CPI could however be overshadowed by testimony from Fed Chair Kevin Warsh to the House Financial Services Committee due 90 minutes later, even if he continues to decline forward guidance. June PPI is due on Wednesday, which we also expect to be unchanged overall, but with 0.4% increases in the core rates, both ex food and energy and ex food, energy and trade. July’s Empire State manufacturing report is also due on Wednesday, with the Philly Fed’s following on Thursday.

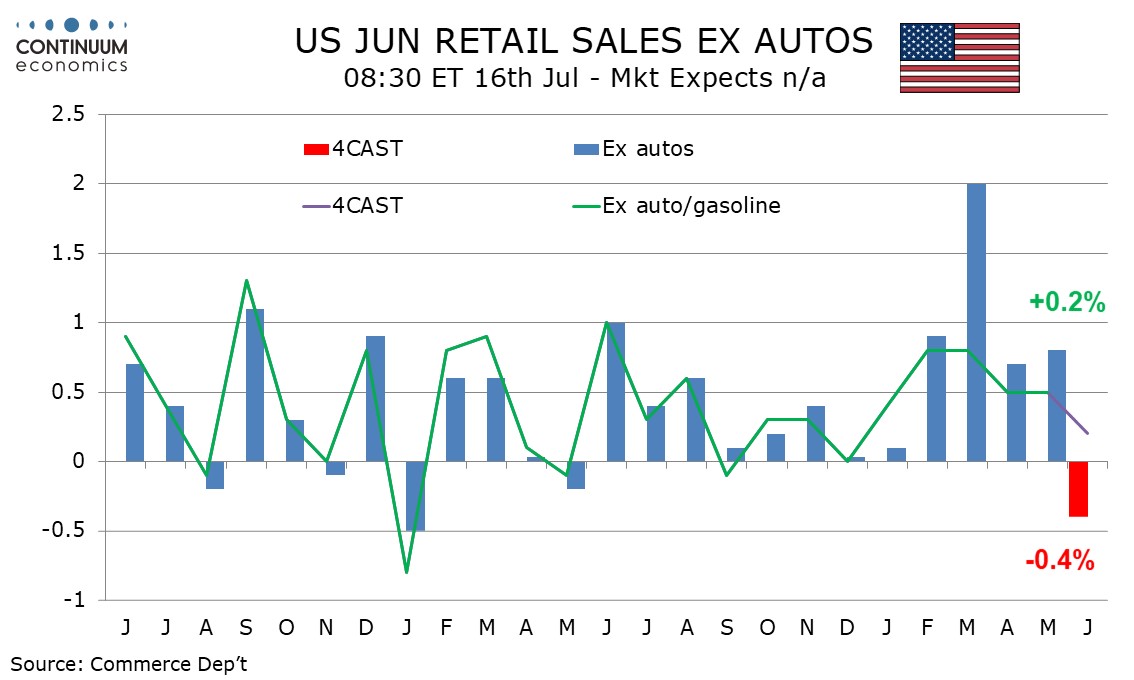

Also due on Thursday are weekly initial claims and June retail sales. The latter will be watched to see if recent consumer resilience persists. We expect a 0.2% decline overall and a 0.4% decline ex autos, but a 0.2% increase ex autos and gasoline. May business inventories, where existing data suggests a rise of 0.6%, July’s NAHB homebuilders’ index, and June pending home sales follow. On Friday we expect June housing starts to rise by 13.0% to 1.33m after a 15.4% May decline, while permits fall by 2.1% to 1.38m after a 0.9% May decline. June industrial production follows, which we expect to be unchanged overall with a 0.1% rise in manufacturing. Friday also sees the preliminary July Michigan CSI, which may see support from lower gasoline prices.

CANADA

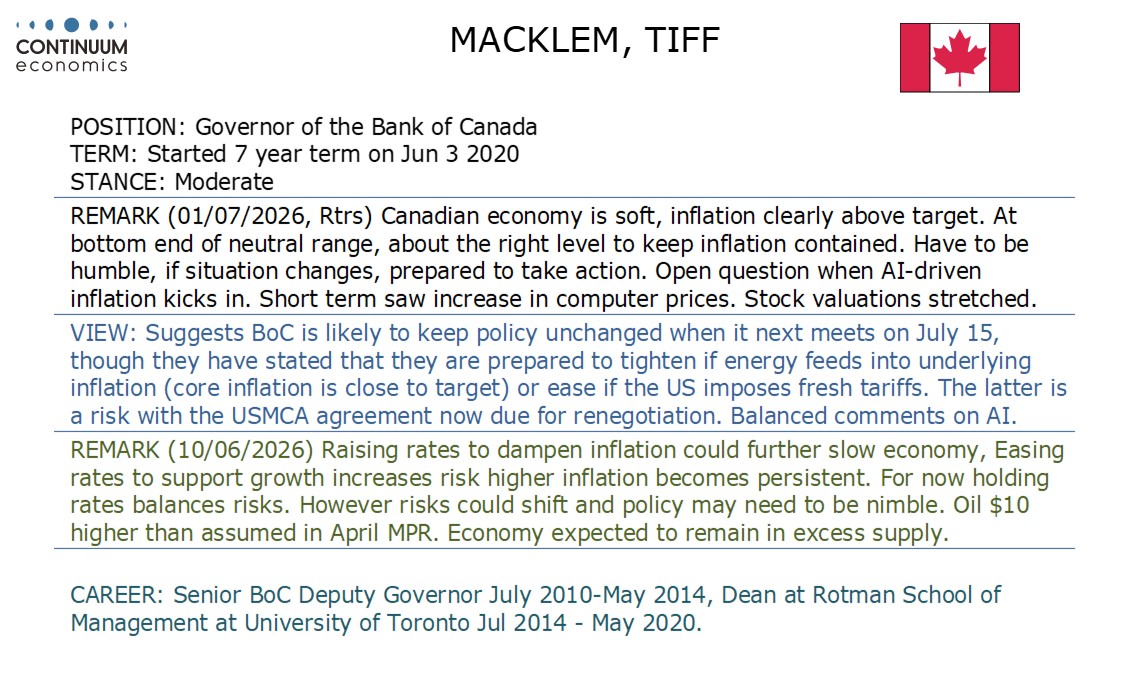

The Bank of Canada meets on Wednesday, and looks set to leave rates unchanged at 2.25%. They have stated that they are willing to tighten if higher energy costs feed into underlying inflation or ease if the US imposes fresh tariffs. The former risk has faded somewhat, which may see greater emphasis put on the latter. Canadian data includes May manufacturing and wholesale sales on Wednesday, for which respective preliminary estimates were for a 1.1% increase and a 0.7% decline (ex-petroleum for the latter). Also due are June existing home sales on Wednesday and June housing starts on Thursday.

UK

May’s GDP data may show conflicting signals, with a 0.1% m/m still consistent with Q2 growing by 0.2%, absent revisions of course. The usual accompanying data, including vis Trade, services and construction may also paint a differ picture. Otherwise, BoE Governor Bailey speaks (Mon).

Eurozone

Data wise, final HICP numbers, trade and industrial production all arrive Thursday. Thursday sees an ECB gathering, with at least three speeches.

Rest of Western Europe

There are a few key events in Sweden, not least what were near-unchanged headline June CPI flash numbers, such an outcome chiming with the Riksbank latest projection.

JP

Quiet calendar for Japan next week. Bunch of tier two data only. The blunt of energy is unlikely to be reflected in industrial production just yet.

AU

The Summer quietness creeping in. Consumer confidence on Tuesday and inflation expectation on Thursday are the only releases for Australia.

NZ

Business PSI on Monday, business confidence on Tuesday concludes the calendar for Kiwi.