FX Daily Strategy: N America, Jun 19th

Market Focus Stays in Middle East

Japan national CPI Remains Compressed

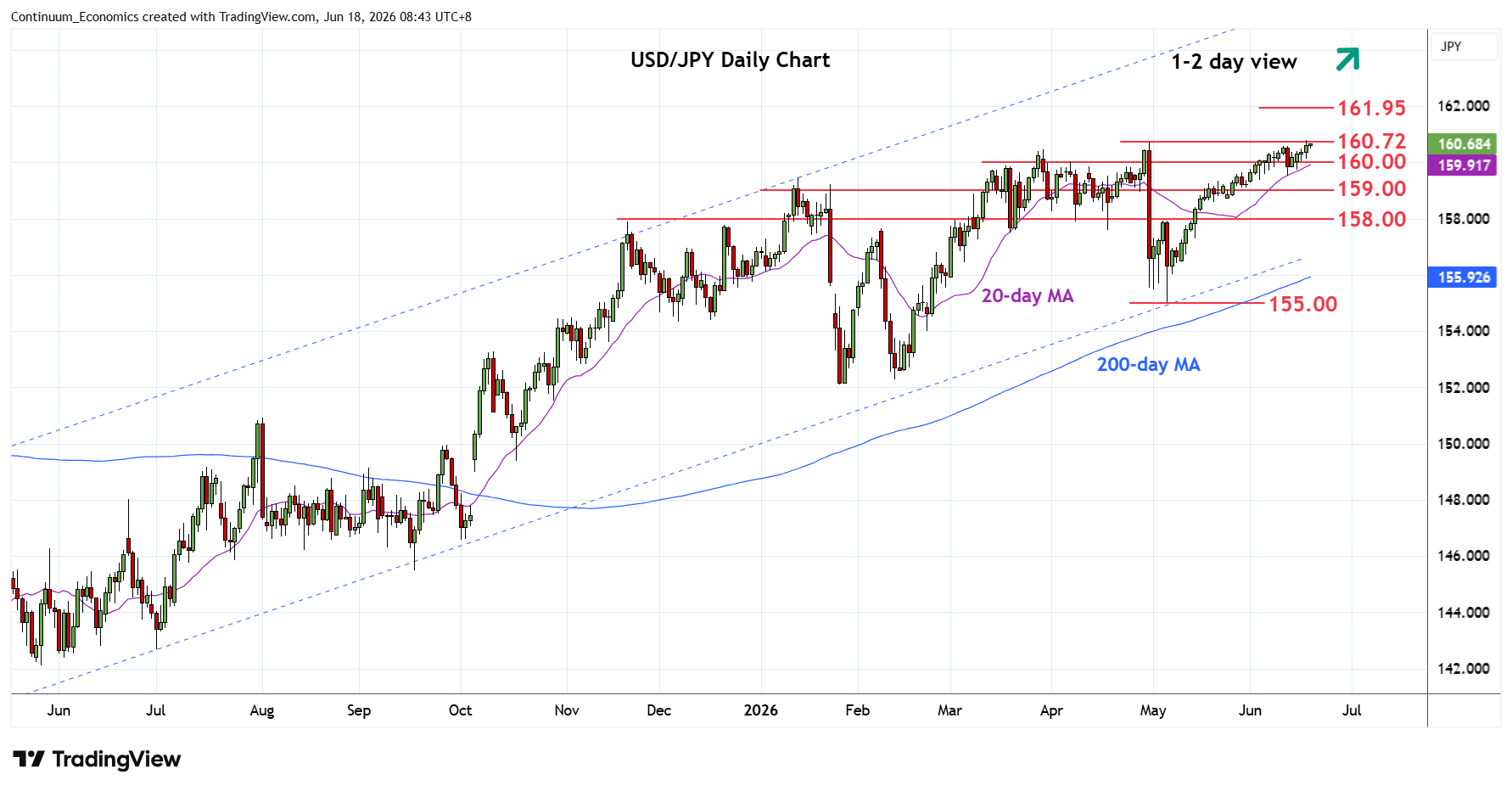

USD/JPY Consolidating, Tilted Higher

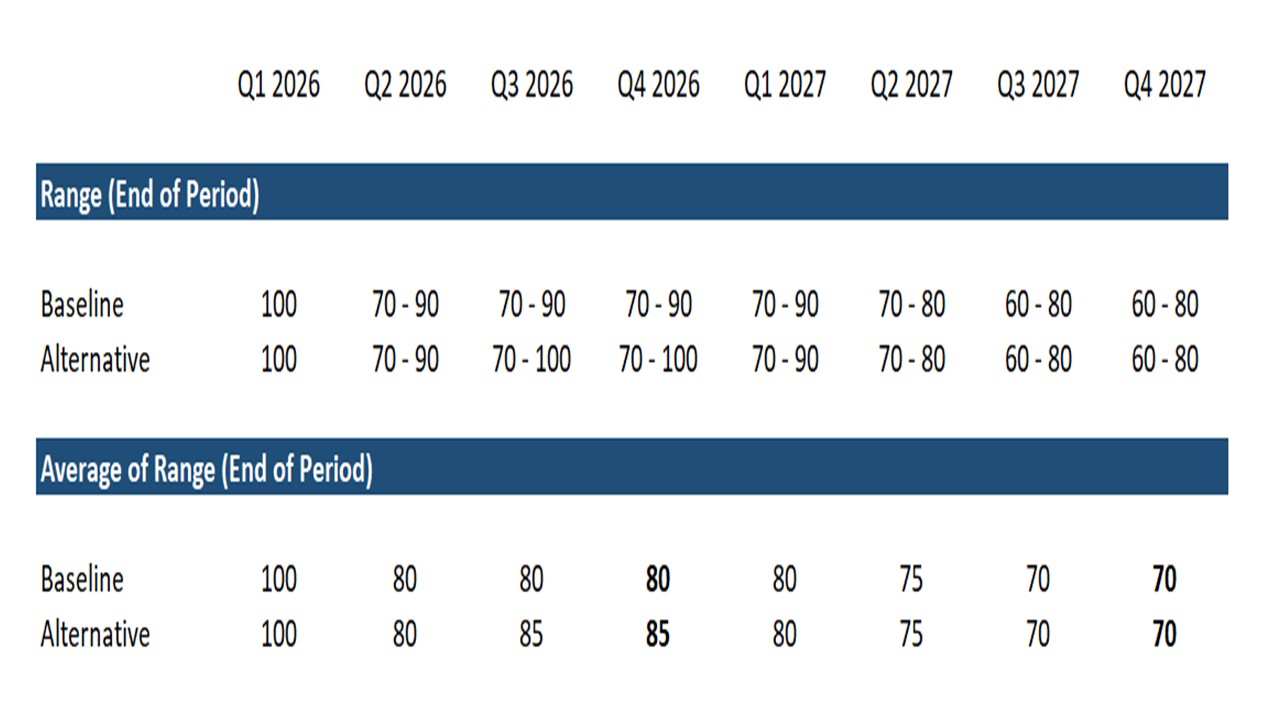

Figure: WTI Oil Price Projections (USD)

Our baseline (80%) is that the Strait of Hormuz will reopen in H2 2026 and remains open through 2027. However, logistics dislocation plus a switch from commercial inventory rundown to rebuilding will likely slow the decline in oil prices back towards normal levels (Figure 1). Our new alternative scenario (20%) is that Israel attacks Hezbollah to disrupt the deal and then Iran temporarily threatens to close the Strait, which could then add a risk premium to oil prices over the next 18 months. An actual temporary closure would produce a bigger risk premium.

Economic pressure has helped drive the June 14 interim agreement between Iran and the U.S., and while frictions remain (evident in today's delayed peace talks) uneasy progress is still expected. Oil markets continue to take comfort from start of shipments even with the halting moves on the next steps.

Iran’s loss of revenue from the U.S. blockade, plus the risk of damage to wells from shutdowns, helped drive the regime towards an agreement. The Trump administration, desperate to reverse politically toxic high gasoline and diesel prices, was willing to compromise to reach an agreement. Nevertheless, Iran feels that the agreement is linked to Lebanon peace as well, which Israel has not agreed to. We see two scenarios: the Strait of Hormuz remains open for the remainder of 2026 and 2027, or Iran threatens or actually imposes a temporary closure in response to new Israeli attacks on Lebanon.

In Japan, the extension of energy stimulus have partially cushioned the high energy cost and kept headline CPI in check as evident in the latest prints overnight, sticking at 1.5% y/y with ex fresh food & energy also below at 1.8% y/y. We all know it is driven lower by stimulus and base effect, but the slow consumption cannot be neglected. BoJ’s Himino struck a relatively hawkish note emphasising the need not to delay hiking amid risks of inflation overshoot from supply and demand side factors, reinforced by minutes to the April meeting highlighting one argument that hikes should come more quickly. FinMin Katayama reiterated threats on yen and that have ‘confirmed at G7 we can take decisive action’. Intervention on any fast test of the major low is looking pretty high risk with BoJ and G7 out the way and critical levels in frame.

On the chart, USD/JPY is still pressuring the upside as prices extend bullish gains from the 155.00 May low to retest 160.72 April YTD high. Break here will extend the broader gains from 2024 year low and see room to 161.00 level though focus will turn towards the 161.95, July 2024 multi-year high. Meanwhile, support is raised to the 160.00 figure and this extend to the 159.53 low of last week. Would take break here to open up room for deeper pullback to retrace strong gains from the 155.00 May low. Lower will see room to support at the 159.00/158.60 congestion and 18 May low.