FX Daily Strategy: N America, May 19th

Erratic Iran headlines continues, glass half full and empty reads

Stretched positioning still dominates, keeping dollar propped

Oil still sets the tone, but along with other areas of risk build up

UK labour market soft, favouring BoE caution; Burnham reassures

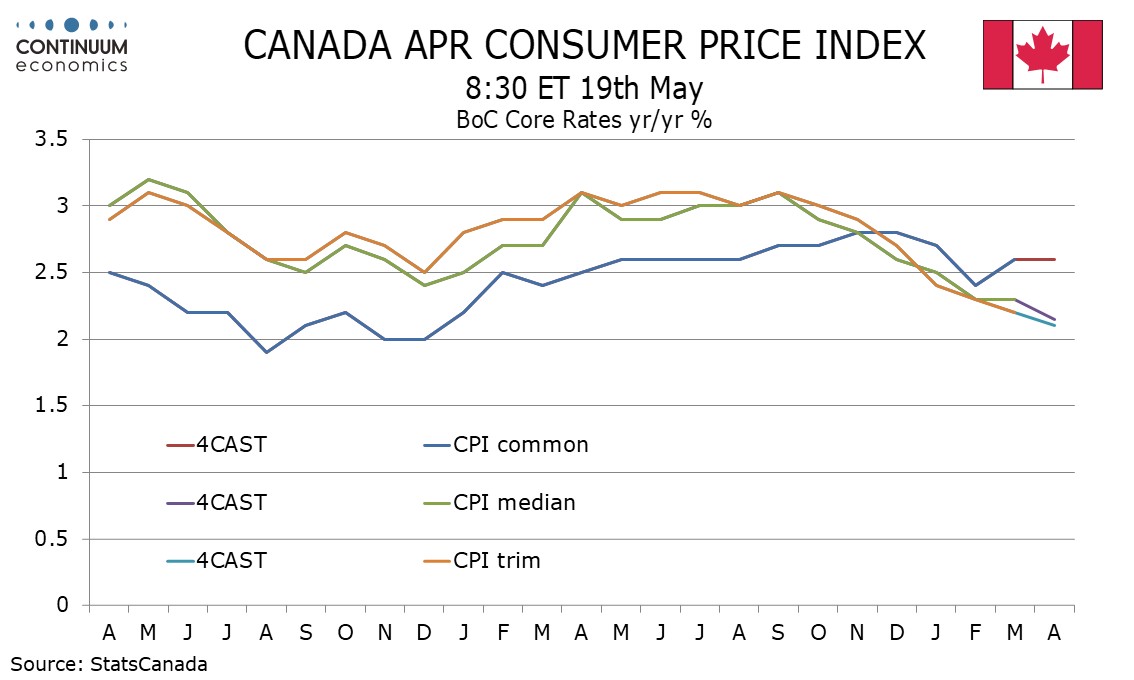

Canada CPI likewise seen implying little immediate pressure to hike

Headlines on Iran continue to prove erratic, glass half full and empty reads on the latest 'delayed strikes' and hopes of a deal comments. Oil and yields have backed off the highs for now but with comments so erratic and unreliable day to day, hour by hour, nobody is going to be drawing any comfort for long unless real evidence of a deal is forthcoming.

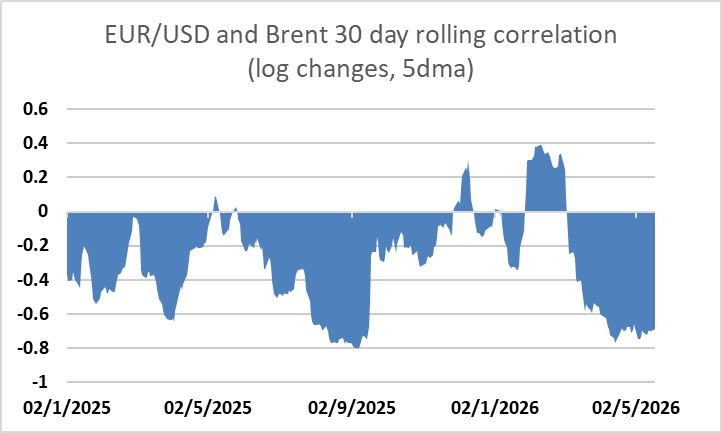

The “clock ticking”, not only as far as an impatient Trump is concerned but also in terms of the probability of lasting footprint on the macro and market outlook for this year. It is hard to look past that Iran story nearby for direction, as evident for example in the rolling EUR/USD oil correlations and similar metrics.

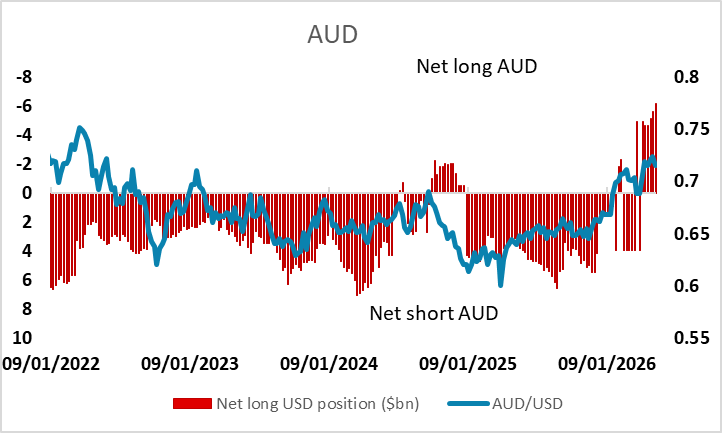

That story still sits within one of broader risk positioning however with different strands to it. The most speculatively leverage trades (clustering around AI build up, Nvidia earnings a nearby focus), the most heavily populated thematic trades (for example recently AUD, and terms of trade gainers such as BRL) and the wider dollar backdrop (the recent extent, for example, of USD/Asia regionals pressure) are all part of that broader mix that could yet ignite.

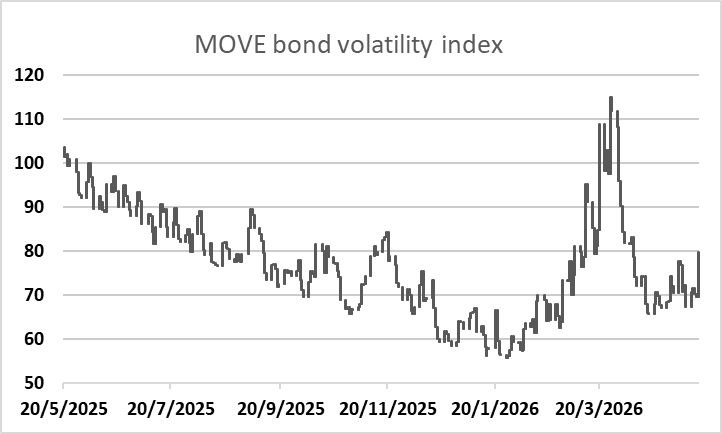

Bond market trade also remains a backdrop issue as major bonds all sit around some critical upside levels and we would continue to monitor any outbreak of volatility for any spillover to the broader market risk and volatility tone. Oil remains a pivotal driver here too of course, as it works through inflation, growth and fiscal channels.

With positioning as it is, any corrective gains in risk currencies against the dollar continue to attract profit-taking, tending to keep price action heavy for now, barring a more significant lasting shift in news flow.

AUD/USD has 0.72- as bounce resistance and prone to re-test 0.71 support unless a deal is struck.

EUR/USD is likewise consolidating the speedy move back to 1.16, but prone in due course to extend to 1.550 unless the backdrop shifts more significantly.

In the UK, we had a reminder that, as previously suggested, the 'Burnham is market negative' narrative risked being a bit overly cliché and one-dimensional, with the reports that he won't seek to overhaul the borrowing rules forcing shaper profit-taking from GBP event shorts. EUR/GBP has essentially been 0.86ish to 0.8750ish all year (minor stretch to 0.88 in March) and continues to respect that for now.

In terms of data, the soft employment data reinforced the need for BoE caution. Underlying earnings are now far off levels consistent with the inflation target at present, vacancies weak, and latest noisy payrolls data was the weakest since the pandemic albeit prone to large revisions. Gilt yields have backed off on the combination of the above, albeit with the broader unstable bond market tone still dictated by the geopolitical developments.

USD/JPY remains a stubbornly challenging market to short at present, given its tendency of late to either be dominated by the rising dollar trend in risk-off days, or lifted by carry on risk-on periods. Until Japan bonds stabilise (in theory Japan yields are not that unattractive hedged these days, were it not for the market continuing to sell off), it’s still struggling to regain its previous risk-off leadership status. For all that, the yen is clearly trading at a current discount and as underscored by the finance minister at G7, the MoF is still there as a force ready to show itself with market checking, guerrilla intervention and heavier intervention as it sees fit into 160. Japan sees Q1 GDP data came in stronger than expected which is a positive but the data precedes the Iran impact and BoJ focus is more on market dynamics than recent data.

Elsewhere, Canada sees its key release of the week with April CPI. We expect acceleration to 2.9% yr/yr from 2.4% in March, the bounce in part due to the April 2025 abolition of the carbon tax. But we also expect the BoC’s core rates on balance to continue declining. As such, data shouldn’t detract from the view the BoC remains patient, while waiting to see if oil remains higher than its central scenario for oil to drop back in coming quarters.