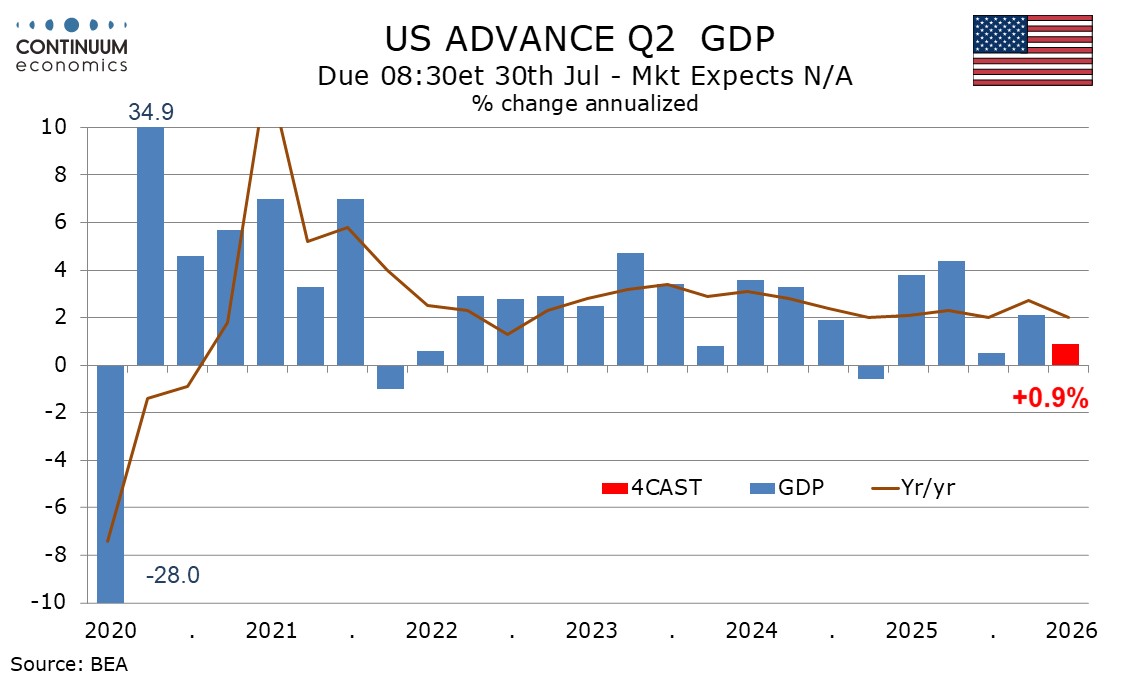

A Strong U.S. Q2 Report Now Looks Unlikely

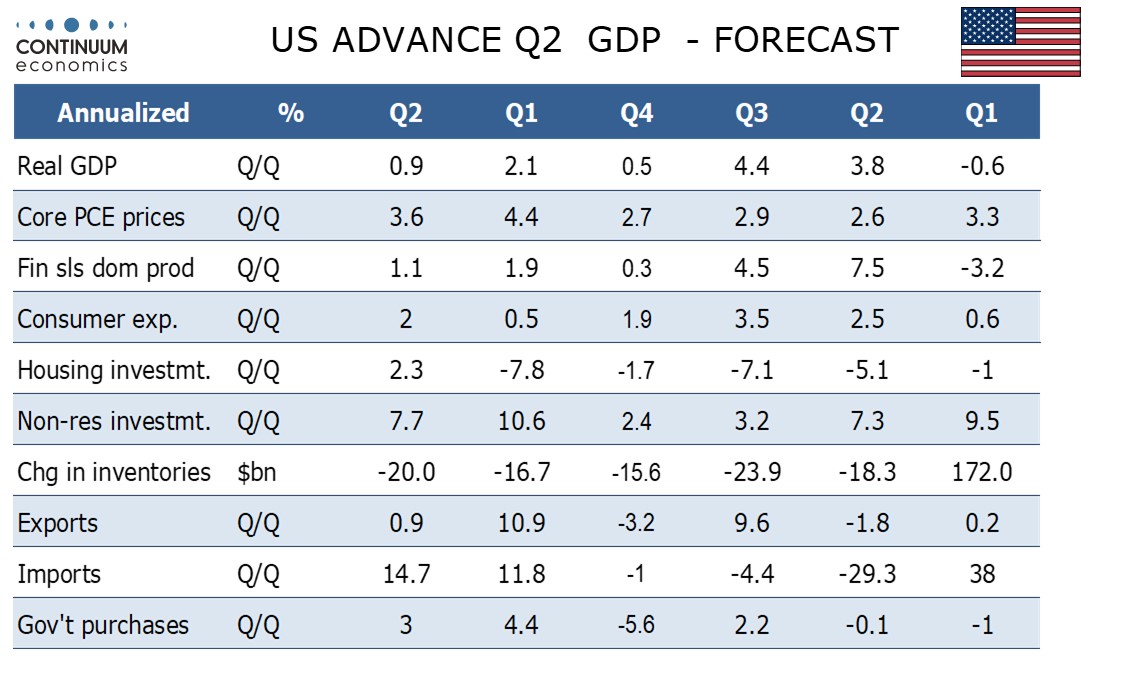

After a sharp deterioration in May’s trade deficit, previously positive forecasts for Q2 GDP need to be trimmed significantly, though there is still uncertainty over June data. We now expect a Q2 GDP increase of only 0.9%, down from a previous estimate of 2.3%. After an upward revision to Q1 our view for 2026 as a whole is not significantly changed, though the second half of the year may now look similar to the first rather than slowing from a stronger Q2.

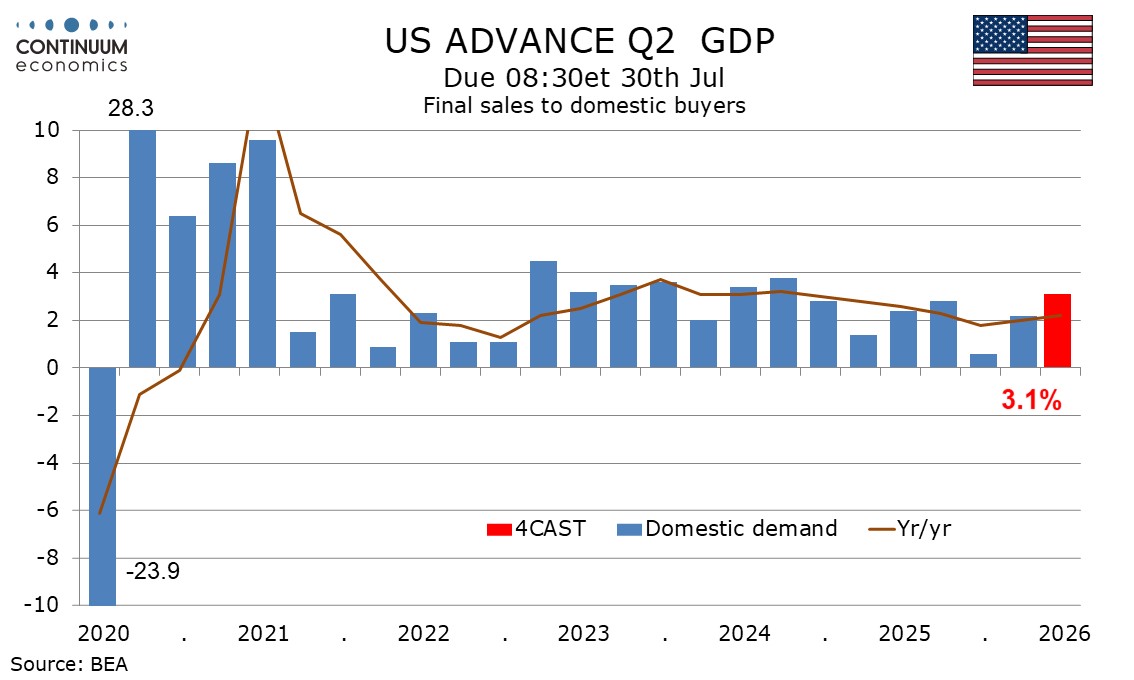

Domestic demand is still likely to look strong in Q2, with a rise of 3.1% in final sales to domestic buyers (GDP less inventories and net exports), which would be the strongest increase since Q3 2025.

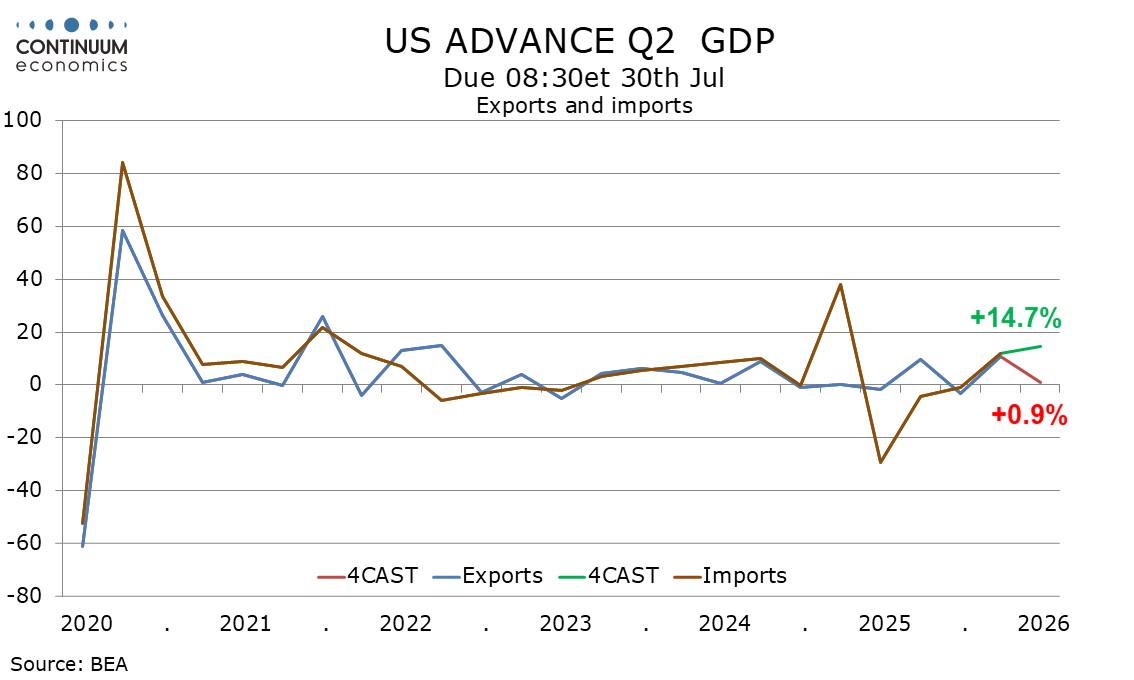

We expect net exports to take off 2.0% from Q2 GDP, assuming a June deficit wider than April’s but narrower than May’s, with exports up a marginal 0.9% but imports surging by 14.7%. The Supreme Court ruling against many of Trump’s tariffs may be lifting imports.

We expect a marginal 0.2% negative contribution from inventories, with a slightly steeper pace of deterioration than in Q1, in part because of supply disruptions related to the Middle East conflict. We expect a 1.1% increase in final sales (GDP less inventories).

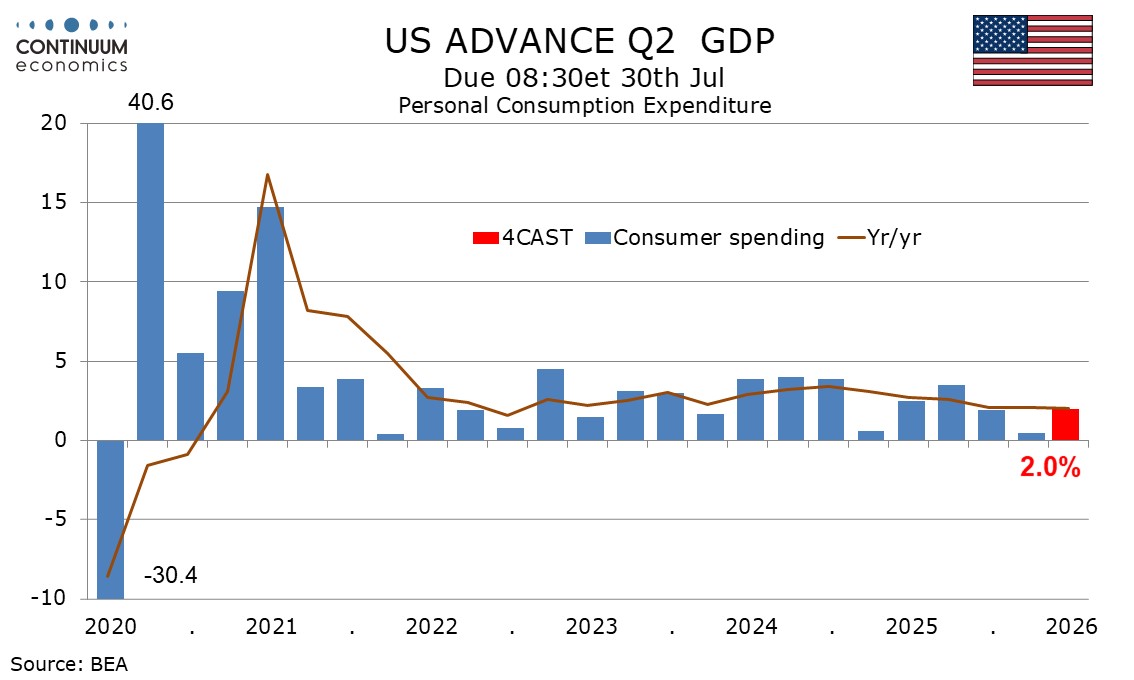

Consumer spending looks resilient to weakness in real disposable income and we expect a 2.0% increase in the former despite a likely 2.3% decline in the latter as PCE prices increase by 5.3%. We expect a 3.6% increase in core PCE prices, still too high but down from 4.6% in Q1.

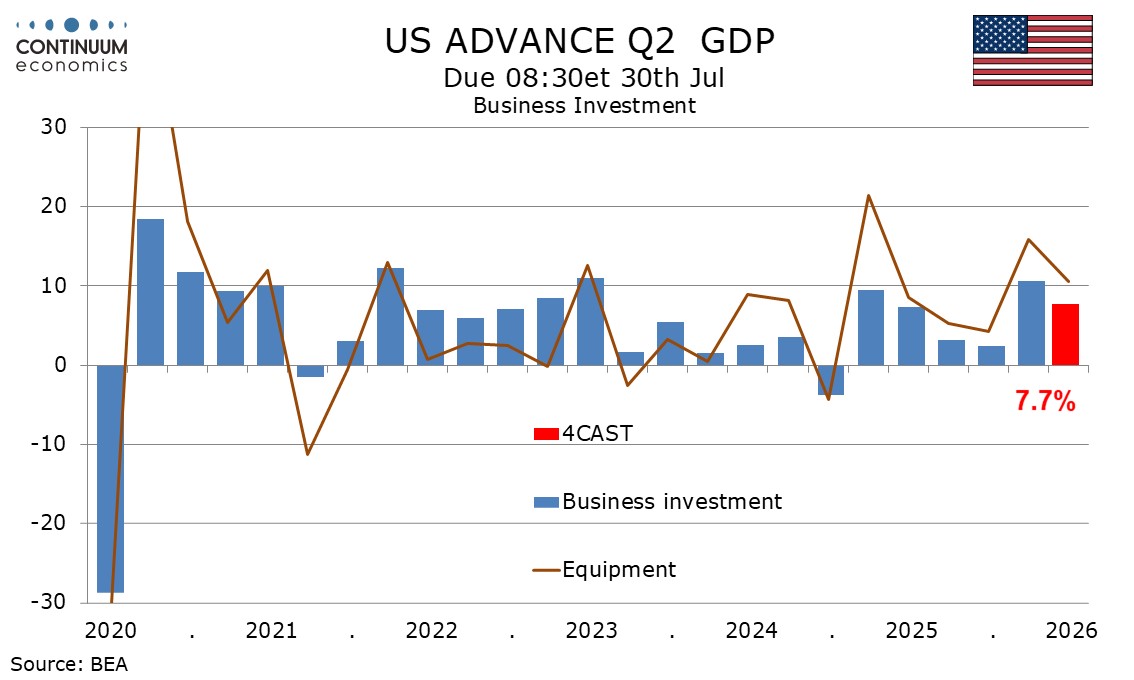

Business investment is likely to remain firm in Q2, led by AI, though our 7.7% forecast is down from 10.6% in Q1, which followed moderate gains of 2.4% in Q3 and 3.2% in Q3 of 2025. We expect the first increase in housing investment since Q1 2024, albeit a modest one of 2.3%.

We expect a 3.0% increase in government with defense likely to be positive and the Q1 reversal of Q4’s shutdown impact probably not fully done. State and local government continues to see moderate growth. A 3.0% increase in overall government would follow a 4.6% increase in Q1 and complete the reversal of Q3’s 5.6% decline, though not quite at the Federal level.

Downgrading of our Q2 view more than fully offsets a recent upward revision to Q1 GDP to 2.1% from 1.6%, that was more than fully due to an upward revision to net exports. Consumer spending was revised significantly lower in Q1, to 0.5% from 1.4%, which may mean slightly less downside scope in the second half of the year. Inventory weakness in Q2 also reduces downside risks for the second half. Still, despite the changing quarterly picture, a fairly subdued 2026 is likely, particularly outside surging business investment.