FX Daily Strategy: Asia, Jun 25th

Australian Employment Market Unlikely to Persuade RBA

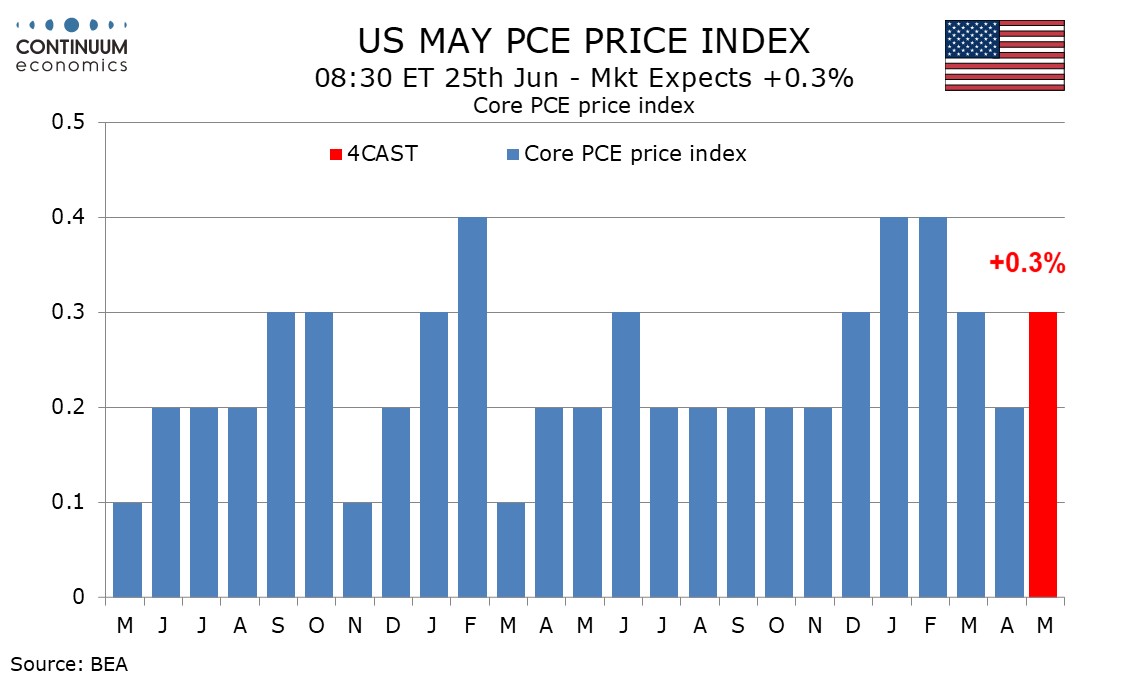

U.S. May Core PCE Prices to outperform CPI

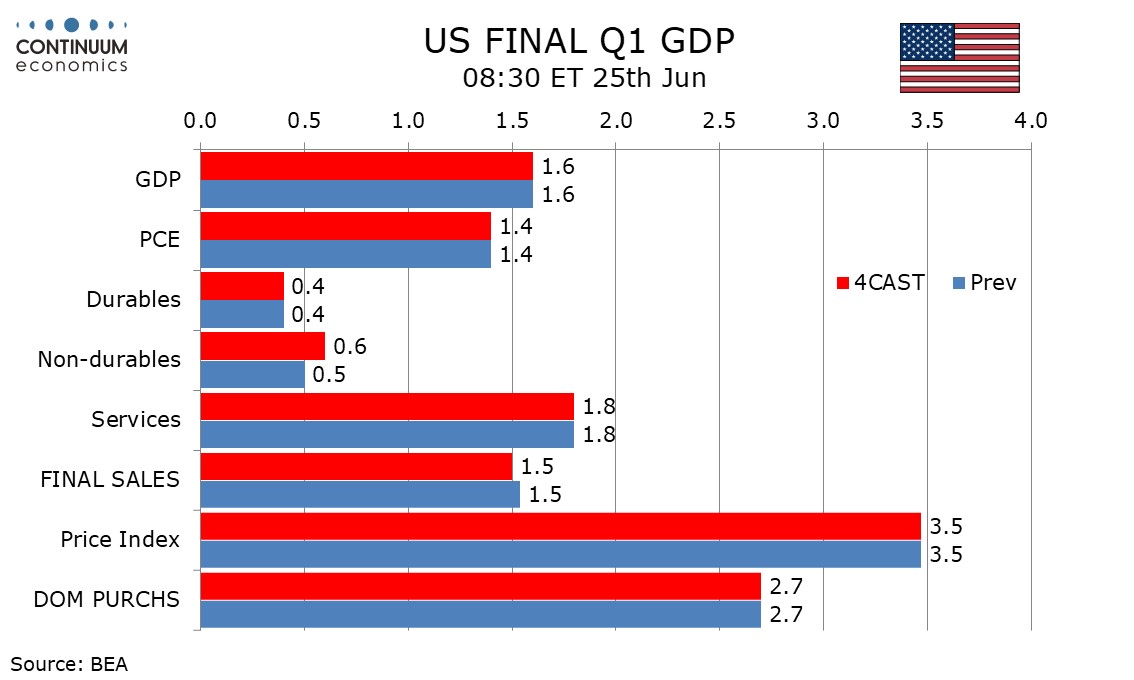

No significant revision for U.S. Final Q1 GDP

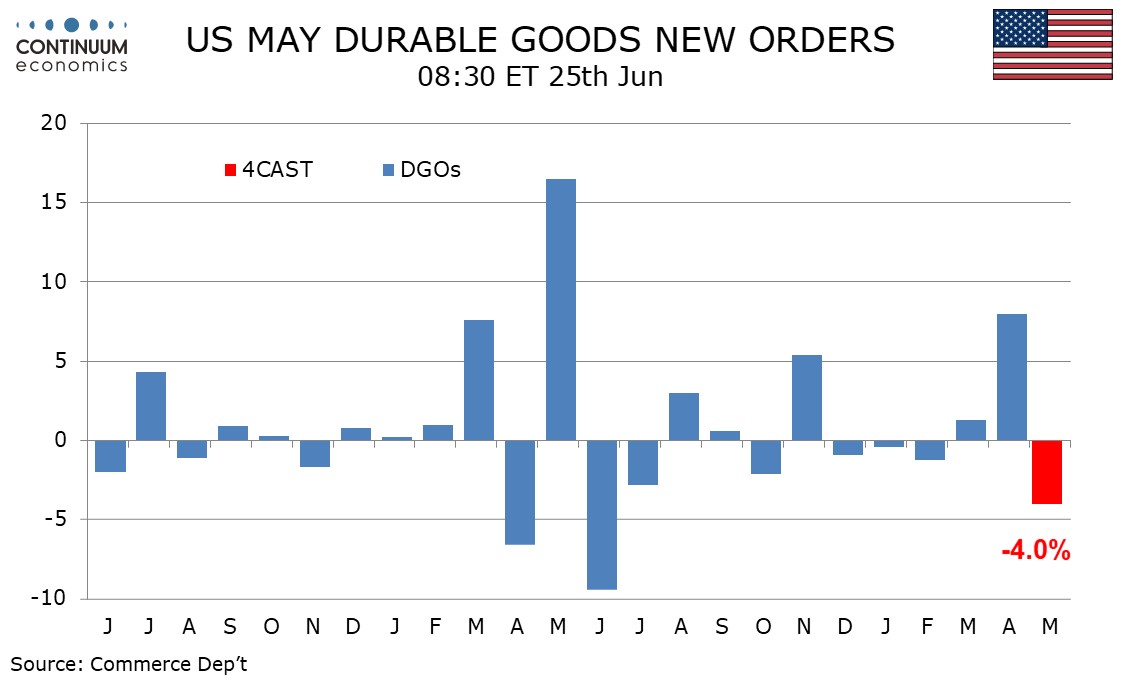

And other U.S. Data

The Australian labor data will unlikely to persuade RBA to hike in the coming meeting. Widely expected the May report to be a rebound from April, the past year has shown Australian labor market being healthily choppy, instead of steaming hot. The lack of strong indicator in the past year should translate to a relatively slower wage growth and keep the RBA comfortable in their current rate path.

On the chart, the pair is sharply lower following break of support at .7000/.6980 low with losses reaching .6907. Consolidation here see prices unwinding oversold intraday studies but a later break lower cannot be ruled out. Nearby see bullish channel support from April 2025 low coming into play at the .6900 congestion. Would take break here to see deeper pullback to retest the .6833 May low. Meanwhile, resistance is lower to .6950 and this extend to .6980/.7000 congestion area which is expected to limit immediate corrective bounce.

We expect May’s core PCE price index to rise by 0.3%, though probably on the low side of 0.3% before rounding, with overall PCE prices up by 0.4%. We expect a 0.6% increase in personal spending to outperform a 0.3% rise in personal income, extending a recent sharp decline in savings. A 0.3% rise in core PCE prices would be stronger than a 0.2% rise in core CPI, which was 0.21% before rounding, Strength in May’s PPI suggests core PCE prices could exceed the core CPI, though the gain is likely to be only marginally above 0.25%.

We expect a final estimate of Q1 GDP at 1.6%, unrevised from the preliminary, though in USD terms we do expect a marginal upward revision. March retail sales were revised marginally higher but we do not expect that to lift consumer spending from the preliminary 1.4%. Construction revisions imply a downward revision to housing but upward revisions to non-residential structures and public construction.

We expect May durable goods orders to fall by 4.0% overall after a rise of 8.0% in April, the moves led by volatility in aircraft. Ex transport we expect an increase of 0.8%, slightly slower than three straight gains in excess of 1.0%, but maintaining a positive trend. Boeing data suggests a significant decline in civil aircraft orders after a strong April. We expect only a marginal increase in auto orders. A strong month from defense, which has a large overlap with transport, is likely. We expect orders ex defense to fall by 5.4% after rise of 8.1% in April.