FX Daily Strategy: N America, May 6th

Slightly stronger USD favoured on ADP data

Middle East risks suggest equities and riskier currencies vulnerable, but hopes of US/Iran deal maintain positive sentiment for now

JPY weakness against European currencies looks increasingly hard to justify

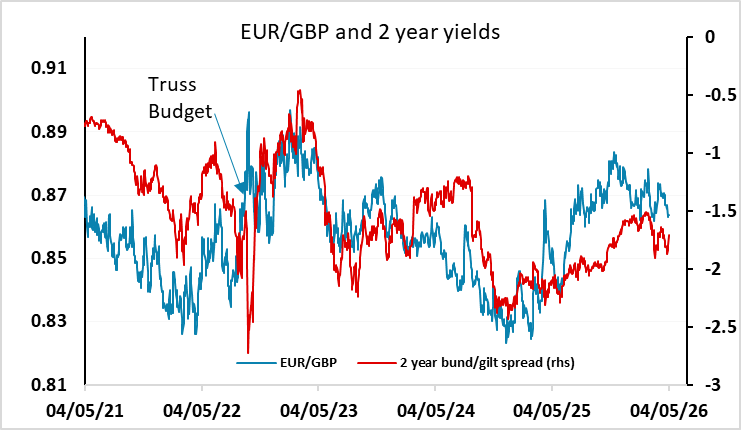

GBP strength against the EUR is likely reaching its peak

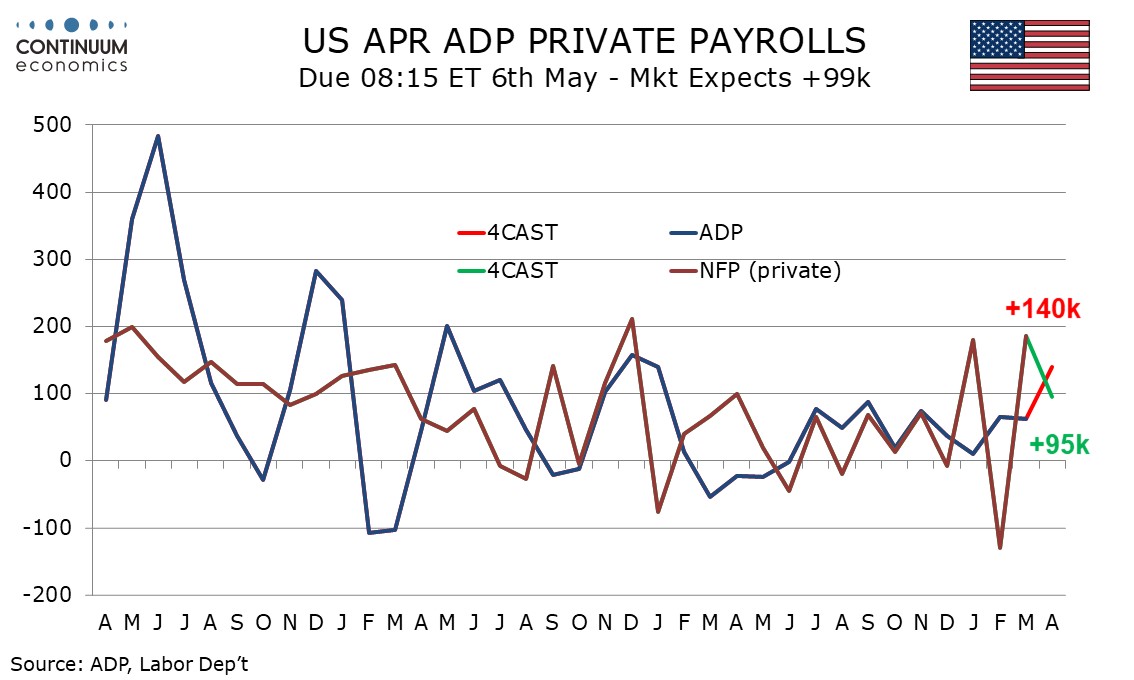

Wednesday sees the US ADP employment data. We expect a 140k increase in April’s ADP estimate for private sector employment, which would be the strongest since a matching gain in January 2025. It would not be quite as strong as a 4-week average of 39.25k in the weekly ADP employment report for the weeks to April 11 implies. We assume some loss of momentum in the week to April 18, the week of the monthly survey, but our forecast is nevertheless stronger than the 116k market consensus. Sensitivity to the ADP data is likely to be modest but our forecast, and even the consensus, suggest a mild upside bias for the USD. Our forecast for the official data is also somewhat stronger than consensus, so we continue to expect some positive USD impact from the data this week.

However, data will probably not be the main driver of volatility through the day, with the focus still on developments in the Middle East. Tuesday saw a generally strong equity market performance with the skirmishes between the US and Iran seen as minor. However, the clock is ticking, and if there is no progress towards a reopening of the Straits of Hormuz the current risk positive market tone is unlikely to last. Nevertheless, overnight talk of the US and Iran moving closer to a deal has maintained the risk positive market tone, and the USD has been a little softer as a result.

The JPY was the market’s whipping boy yesterday, with the impact of last week’s BoJ intervention fading. While the JPY managed a sharp appreciation last Thursday, the underlying market tone doesn’t seem to have changed. While it makes some sense that the USD would benefit if we see some risk negative news, the weakness of the JPY against the European currencies and the AUD looks hard to justify, even if we see risk positive sentiment continuing. However, longer term JPY negative momentum has started to decline, and we would anticipate a JPY break higher in the fullness of time. But this may well require a much bigger turn lower in equities. The reports of more BoJ intervention overnight have reversed yesterday's JPY decline, with both USD/JPY and EUR/JPY making a new post-February low, but The JPY has fallen back in Europe after the intervention, and is now close to yesteday's opening levels.

EUR/GBP continues to test the year’s lows despite there being little good news emerging from the UK, reflecting the general market preference for higher yielders. However, yield spreads are starting to move a little in the EUR’s favour, with ECB tightening looking more certain that tightening in the UK, and the UK also facing political uncertainty with the upcoming local elections and potential challenge to PM Starmer’s leadership. We would see EUR/GBP levels near 0.86 as likely to provide a good long term buying opportunity.