FX Daily Strategy: APAC, Jun 18th

FOMC projections and press conference to set the broad tone

Otherwise focus turns to the UK, with data, BoE and by-election. Sterling mood has improved

SNB seen unchanged and CHF comments to be ignored unless escalated

It goes without saying that the full read of the much-awaited FOMC results and new chair Warsh’s first press conference are going to be dominating the tone into Thursday - and potentially some time onwards, depending on how guarded or not this first showing proves to be.

Outside of that dominant driver, Thursday sees focus partially shift back to the UK, with the Labour market data, BoE decision, and later the count for the political important by-election.

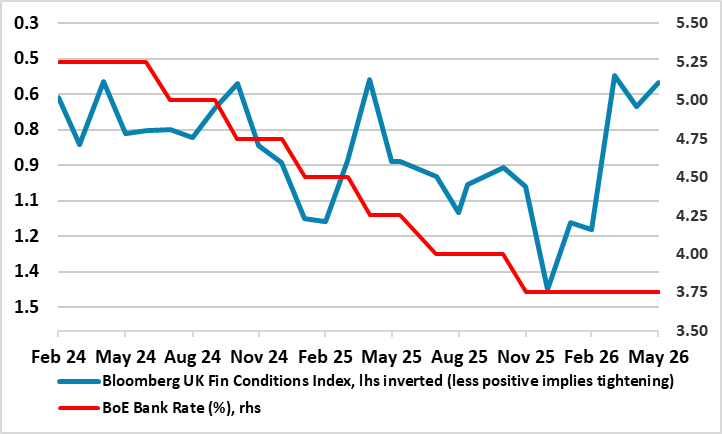

On the former, HMRC data may continue to show slowing in employment while pay data may show fresh slowing from its recent retreat. Data is then unlikely to offer any challenge to the view, supported by recent CPI, that the BoE is not just on hold this meeting as universally expected, but likely reiterating that it sees risk-reward favouring an ongoing pause.

Although there may be some split on the board, the meeting should support the market’s shift towards assuming on-hold through the summer and receding risks of a hike later in the year (our view is on hold throughout).

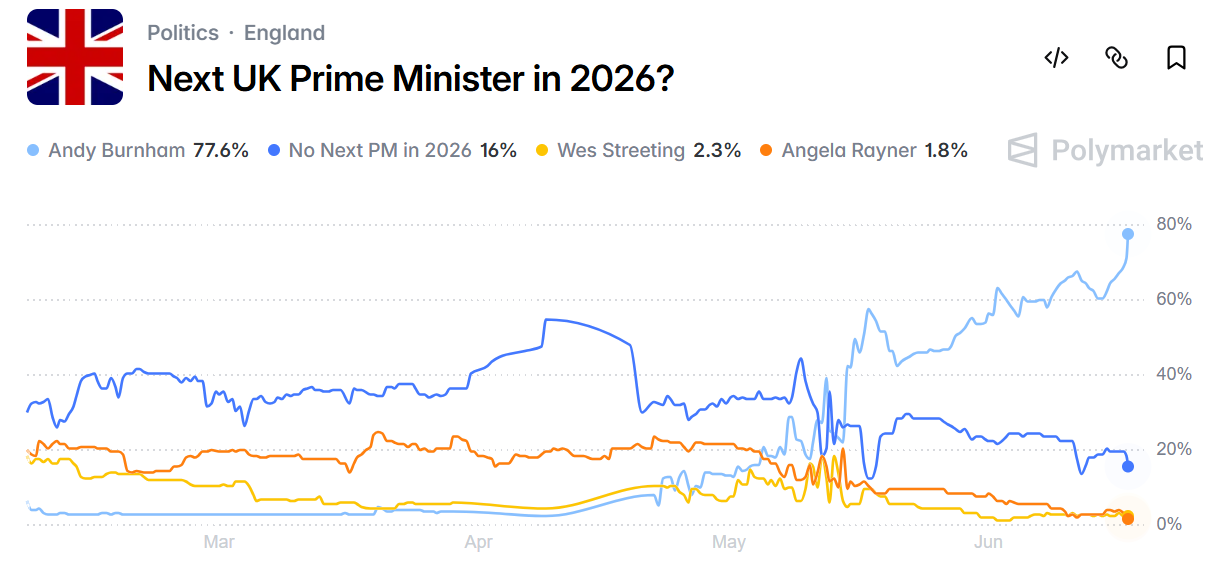

Regarding the byelection, most polls suggest a clear but modest lead for Burnham into the vote. Interestingly, his own popularity has dropped notably since mounting the leadership challenge though remains well ahead of his rivals including Starmer.

For markets, his victory in the seat and then likely victory in the eventual leadership contest is very much priced in. Sterling price action into the vote has also been pretty constructive and while EUR/GBP has been respecting its YTD range again and so mildly lifting off the recent base test, it seems unlikely that events will offer a strong negative sterling trigger.

Indeed, so long as geopolitical improvements remain in place and risk tone generally improved, sterling typically stands to gain from the reduced macro pressure and pro-cyclical bias.

The SNB is a lesser focus with a clear unchanged outlook and little change expected in its forecasts.

There will be some likely reference to watching CHF strength and being able to willing to respond. But these comments are well aired now and are likely to be ignored without any material escalation in tone.

EUR/CHF range recovery has been capped by 0.9250 and has tended to roll back since the referendum passed off without event. 0.9150-00 is the recent limited range downside.

Interestingly, neither CHF upside nor JPY downside has shown a huge amount of inclination to shift from their respective contrasting Iran positioning as yet, and FX markets have been cautious in general in this. That may change in coming weeks if confidence in the de-risking and terms of trade impact reversal grows.