FX Daily Strategy: Asia, Jul 2

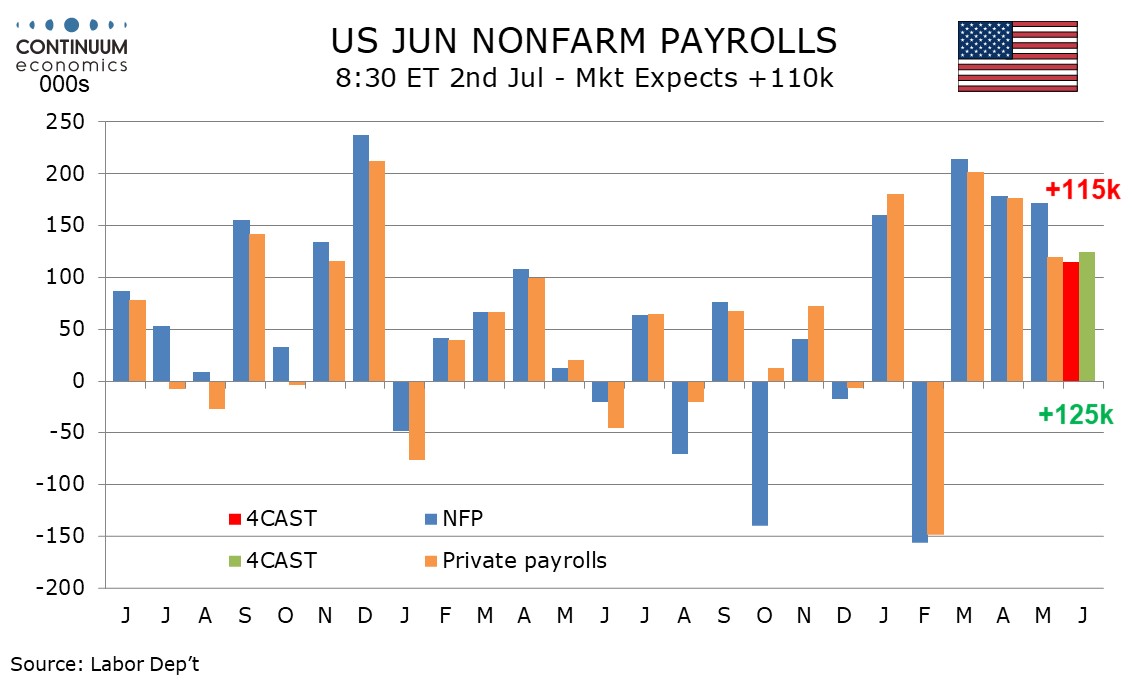

Payrolls in focus. Probably needs a 100k+/- surprise to prompt excitement

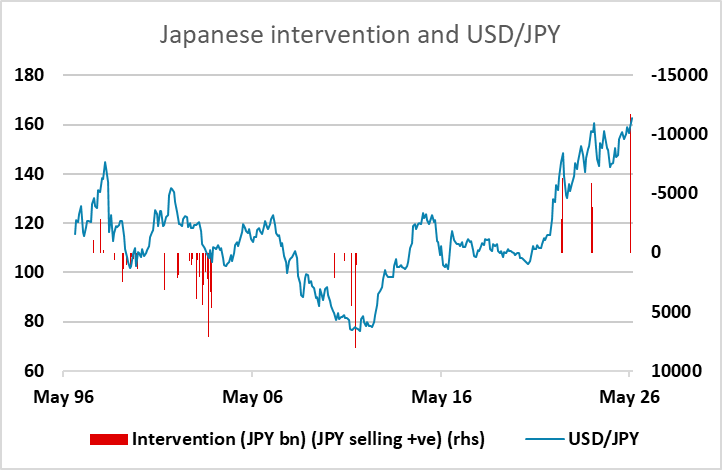

Friday's US holiday may leave mkt wary of Japan intervention, prompt some early covering

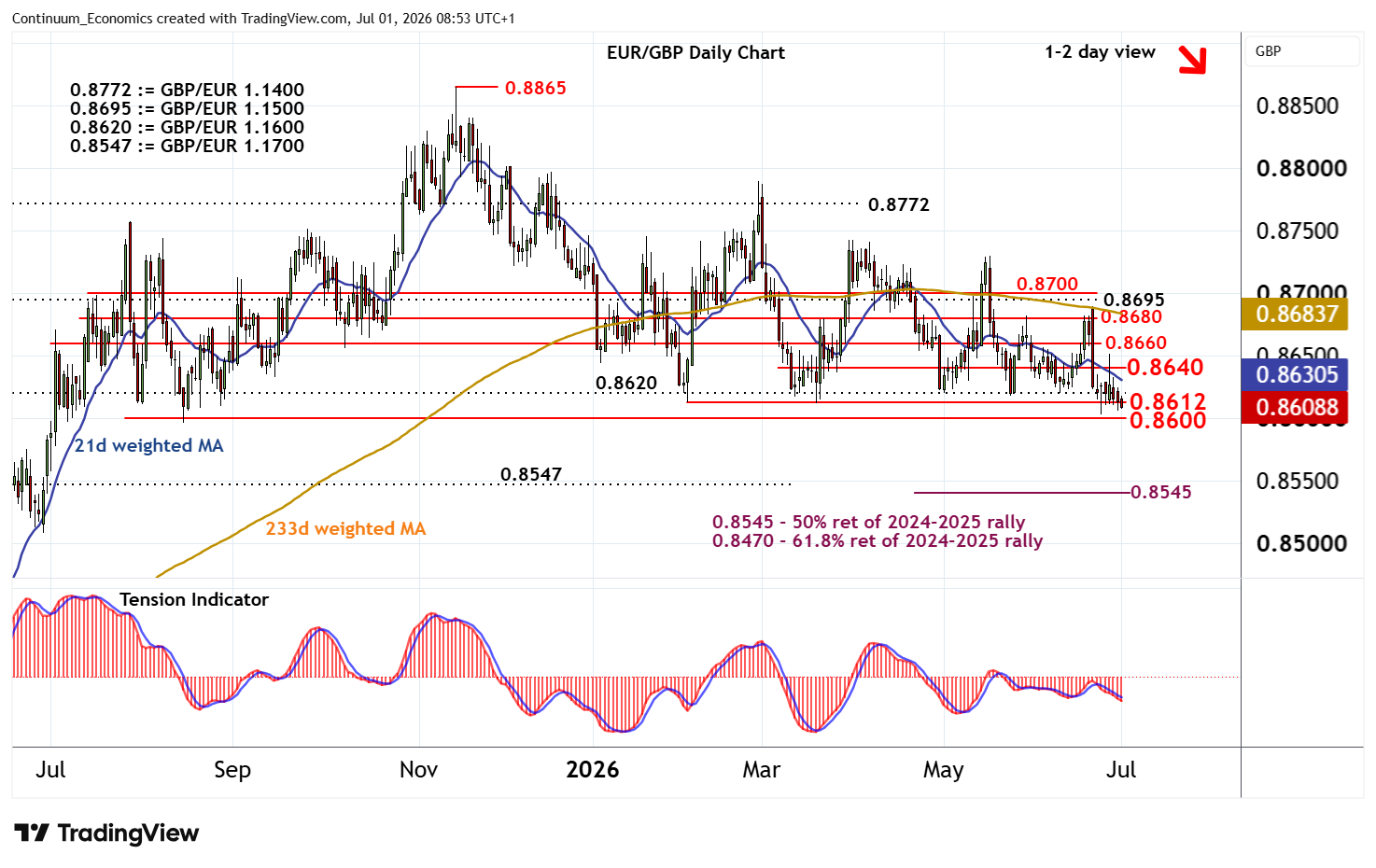

EUR/GBP still sitting on key support, risk of break remains

With the US out on 4th July holiday early, tomorrow is a virtual Friday as far as markets are concerned and with the key payrolls report ahead of time.

There are a cluster of options as a result, focused mainly on 1.14 and 1.1450 on EUR/USD. The next biggest focal point is on 1.13, while USD/JPY has a chunk well below at 159.

In that respect, it is worth acknowledging the MoF’s penchant for targeting holidays, particularly its own but also US holidays, for intervention to try and take advance of low liquidity. Thinly covered desks on 4th July marks it out as an obvious day for the market to be on high alert and so there might even be a degree of self-enforcement prior (i.e. some short yen covering just in case).

Certainly, on the latest leg to new 40 year highs, USD/JPY has become a bit more technically overbought and recent data has shown spec yen shorts moderately high. Friday might, ironically, lack the element of surprise as a result but it is pragmatic, coming after the week’s main events out of the way. In any event the game of cat and mouse continues and so it would not be surprising for some to be trimming longs pre-emptively on Thursday, especially if the pair does lift out of payrolls.

As for payrolls, we look for the headline to rise by 115k overall and by 125k in the private sector, the former a slowing from 172k in May but the latter marginally stronger than May’s 120k increase. We also see the unemployment rate remaining at 4.3% for a fourth straight month and an in line with trend 0.3% rise in average hourly earnings. Details will also be scrutinised given the possibility that the report is somewhat flattered by temporary World Cup hires.

Such a result would be fairly ‘middle of the road’ – not super strong and a green light to tightening but at the same time still pretty solid and keeping the focus on the output gap and inflation trajectory going forward. It doesn’t have to be a stellar report in order to keep the market focused on a relative US resilience narrative for now, especially amid flagging market expectations over European rates policy. Recent data and comments have reinforced confidence in a lack of summer action from the ECB and the BoE and flagging expectations further out in the year.

That said, it probably does need a figure more like 200k+ or near zero to really be making its mark on Thursday.

Outside of the dollar focus, there remains some interest in sterling. We’ve noted a number of times that the combination of decade plus extremes in short GBP spec positioning, together with EUR/GBP sitting on critical cross range support, and potential ‘buy the fact’ on political sensitivity ebbing all mean that there is some risk of a GBP squeeze that triggers some technical break follow through. This remains something to watch, notwithstanding the fact that UK data continues to be soft and the impulse for BoE tightening low near-term. A close below 0.86 could extend November losses towards the 0.8545 Fibonacci retracement and 0.8547, (GBP/EUR 1.1700).